- with readers working within the Business & Consumer Services industries

- within Strategy, Family and Matrimonial and Insolvency/Bankruptcy/Re-Structuring topic(s)

PREFACE

The crypto assets sector has been on the watch list of both investors and lawmakers in recent years due to the increased adoption across the world. India has an estimated 25 to 30 million crypto investors, and the numbers are likely to significantly increase in the coming years. The sector has a flourishing ecosystem replete with exchanges, wallets, miners, and investors. The sector has massive potential in terms of contribution to the economy and generating employment. According to a report published by CrossTower and US-India Strategic Partnership Forum, embracing and fostering crypto assets in India would grow the country's GDP at a healthy 43.1% CAGR from $5.1 billion in 2021 to $261.8 billion over an 11-year period, resulting in a $1.1 trillion contribution to the GDP. The bulk of this $1.1 trillion in economic growth for India over these 11 years would be derived from ancillary crypto asset-related businesses that are yet to be materialised.1

However, despite the large number of players involved in the crypto-asset market, it remains largely unregulated and currently operates in a grey zone, abstruse in its many dimensions. The lacuna stems from the inability of the existing legal framework to deal with policy issues and concerns surrounding crypto assets.

Governments across the world have identified major concerns in the crypto assets sector that revolves around financial stability, investor and consumer protection, money laundering etc. Owing to these risks, the bulk of entities operating in the crypto-asset market in India and across the world currently lack standard operational, governance and risk practices. This has led to market turbulence and uncertainty in operations for the industry players and is gradually eroding consumer trust and confidence in the sector.

Therefore, it is imperative for governments worldwide to develop standard operating procedures for crypto assets. This would help countries globally, across the G20 group and beyond, to have a technology-driven regulatory framework which will promote cooperation across borders and address the major policy concerns. India's ongoing G20 Presidency has been making a strong case for global regulation of crypto assets.

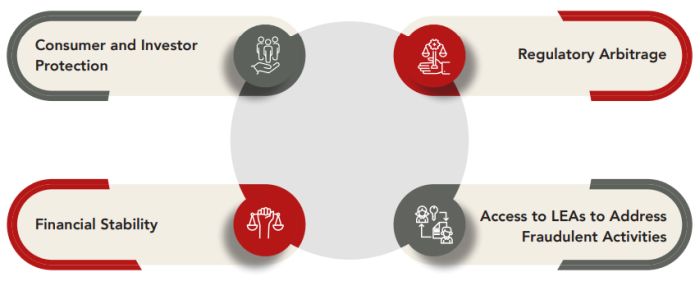

With the objective to create a favourable policy ecosystem for the crypto assets, Chase India & INDUSLAW have drafted the report aimed at developing standard operating procedures (SOPs) for the sector. The report has described in detail the four major areas – i) Consumer and Investor Protection, ii) Access for LEAs to Address Fraudulent Activities, iii) Regulatory Arbitrage, and iv) Financial Stability which have been the key cause of concern for the governments and regulators worldwide. As a way forward approach, the report has touched upon the key aspects of these major concern areas and drawn references from the international best practices to identify the SOPs to regulate the sector.

INTRODUCTION AND OVERVIEW

In their short history, Virtual Digital Assets ("VDAs") have proven their utility in public service, wealth distribution, and economic access worldwide through their utilization of digital ledger technology ("DLT") or blockchain technology. DLT allows for trust, security, transparency, and the traceability of data, which is especially beneficial to the financial context as it contributes to the reduction of information asymmetry and improves accountability in the provision of financial services. However, the 'crypto sphere' can be a potential safe haven for financial transactions by terrorist regimes and white-collar criminals. In addition, large-scale adoption of VDAs without regulatory oversight and control can adversely impact customers or investors who invest in such VDA projects and can have further macroeconomic impacts. On the other hand, globally, inordinate weightage has been placed on these concerns inviting disproportionate restrictions on VDAs by most governments. In doing so, an important economic opportunity is being missed by countries.

In India, regulations relating to VDAs have not been finalized yet, and one can expect some guidance for domestic regulation in India on VDAs emerging from the discussions currently underway within the G20. However, the general regulatory approach towards transactions relating to VDAs has been predominantly cautionary, perhaps for the right reasons. Recently, high taxes on VDA gains in India have been introduced as a means to deter investors/customers from making an investment in VDAs.2 This may be done to ensure that the retail investor is discouraged from investing and transacting in crypto, and only large institutional investors with appropriate risk appetite and financial capability may engage in such investments. In addition, the government has taken note of the problems existing in the sector in relation to money laundering and has brought VDAs under the purview of the extant anti-money laundering framework in India by including VDA Service Providers in the Prevention of Money Laundering Act (PMLA).

Moreover, there are several challenges recognized globally in relation to VDAs. It is necessary to consider such challenges in order to formulate an effective framework for SOPs.

Problem of Anonymity

It is pertinent to note here that crypto was built on blockchain ledger technology. The blockchain was lauded for ensuring the authentication of transactions by all users on the blockchain. One of the advantages of the blockchain was not to create a transactional plane where the payer and payee can be faceless and untraceable but to increase consumer ownership of transactions.

This challenge is not the first time that governments have had to deal with a transactional plane that cannot be traced back to the payor or payee. Cash transactions still constitute the bulk of grey market exchange. This does not mean that cash as a medium of exchange and store of value can be banned or derecognized. Credit and debit through bank transfers also occasionally happens over the wire without a need for identity verification or using proxy verification details. In other words, the identity of the source of funds and the fund's receiver is not critical for a bank transfer to occur as they happen over the internet. In both the above cases, and in the present case of crypto, regulatory mandates for KYC and a formal customer relationship mechanism between holders/consumers of VDAs and Virtual Asset Service Providers (VASPs) are required.

Transformation of VDAs

Conversion of fiat currency held in traditional bank accounts undergo a complicated 'cleansing' process whereby this money is converted into a virtual digital asset. In this manner, the primary money trail that underlies the asset is obfuscated.3 However, in its current usage, crypto is used as a store value. Thus, the value held in crypto in this manner has to be realizable at some point and be integrated into the fiduciary cash flow of an economy to become usable by the beneficiary. Once again, regulatory efforts should be geared towards recognizing VDA exchanges as regulated entities. It would also behove governments use available softwares which can untangle or 'un-mix' and 'un-layer' crypto which has been converted from fiat to a VDA. This is indeed an opportunity for governments to integrate programs and specialized e-governance frameworks into law enforcement. With the adoption of machine learning based on Bigdata, the regulator will develop an initial database and upgrade or update its existing database to investigate criminals laundering money. As is suggested by international organisations like the FATF, ample budget and personnel need to be set aside for the development of such a database and investigative software.

Central Regulation of a Decentralized Asset Class

VDAs are also the vanguards of decentralized finance. The distributed nature of blockchain ledgers has been put to both virtuous and vicious use. On one hand, blockchain is goal-oriented in that it affords authentic exchange of value over secured networks which are verifiable by anyone who is a part of the transaction. On the other hand, it shuts out centralized law enforcement agencies from knowing the sources of funding. This problem is further exacerbated by the global infrastructure that supports such transactions, with links, in the form of an exchange or a mixer or a custodian, present at every node of the exchange infrastructure.

Global reach, anonymity and speedy transactions between the payer and the payee directly have made VDAs conduits for money laundering, terror financing and other illegal activities. To combat such activities, SOPs (in line with requirements under the PMLA) could help LEAs in quick and timely intervention. We suggest a model of regulatory agility and enforcement tools that can enable governments to confidently allow VDAs and benefit from their success.

Policymakers and stakeholders across the world have been closely monitoring the developments in India amid the ongoing G20 Presidency, which is expected to build a global consensus to regulate the crypto asset sector in India. The country's Finance Minister Nirmala Sitharaman on multiple occasions reiterated that "crypto has been a very important part of the discussion under India's G20 Presidency, given so many collapses and shocks. We seek to develop a common framework for all countries to deal with this matter". The stage has already been set and it's just a matter of time before the crypto asset sector will be regulated by a set of comprehensive laws.

KEY ASPECTS OF STANDARD OPERATING PROCEDURES (SOPs)

India has begun engaging in dialogues on crypto regulation through platforms such as G20 where discussions shall be conducted on policy approaches towards this sector. Further, distinguished institutions such as the IMF are developing papers focused on "monetary policy and policy approach to crypto assets" through multi-stakeholder consultations. The government has time and again acknowledged the need for prioritizing crypto regulation and the need for developing SOPs.

Setting Minimum Standards

To achieve the overarching goal of promoting global regulations for Web3, it is essential to establish minimum policy and technology standards that countries around the world must adopt. These standards can be classified into different categories based on the nature of the regulatory measures a country wishes to adopt, ranging from conservative to liberal. The minimum standards cover a wide range of issues, including common definitions and classification, consumer protection norms, minimum data collection guidelines, transaction monitoring infrastructure, standardised due diligence, disclosure requirements, compliance measures including licensing for virtual asset service providers, technical standards for cybersecurity, standards to mitigate the adverse impact on the climate, and standardised audit requirements.

Data Sharing

Given the capacity of Web3 to facilitate the peer-to-peer transfer of value via crypto-assets, there is a potential for it to be exploited for unlawful activities, such as money laundering, terrorism financing, and tax evasion. It is, therefore, crucial to establish channels for nations to share information on crypto-asset transactions. Such a mechanism will serve as a crucial tool in promoting transparency in cross-border financial investments and combating offshore tax evasion, and other illicit activities. Thus, it is essential to incorporate a framework for the collection and automatic exchange of information on crypto-asset transactions in global efforts to regulate the Web3 space. The compliance mandate should aim to strike a balance between safeguarding investors and preventing illicit activities while simultaneously promoting innovation and competition.

Capacity Building

Capacity building is critical for the development and growth of the Web3 ecosystem. As industry evolves and new technologies emerge, it is essential to ensure that there is a skilled workforce equipped with the necessary knowledge and expertise to navigate the space effectively. These initiatives can take various forms, such as training programs, workshops, hackathons, mentorship, and education initiatives. These efforts can help create a pool of talented developers, entrepreneurs, and innovators who can drive the growth of the Web3 industry and contribute to the creation of new products and services. Additionally, by investing in capacity building, these organizations can help develop a talent pipeline that can meet the demands of the rapidly evolving industry.

Against this backdrop, we have identified four priority areas where there is a need to develop SOPs in order to effectively regulate the VDA sector in India (and globally).

Consumer and Investor Protection

- Lack of Effective Consumer Protection

Standards: In the international scenario, consumer

protection in relation to VDAs are driven predominantly from a

disclosure-based approach, similar to India. Certain countries have

proposed regulation as a conscious decision of dissociation from

the unregulated nature of crypto trading. In contrast,

jurisdictions that are still pondering regulation and consequent

legislation have advocated for cautionary standards to be included

while showcasing VDAs to the public, including advertisement

conditions and trading prohibitions. However, there is no singular

plan of action in relation to effective consumer protection

standards that have been adopted prominently by the international

community as a whole, which appears to be the need of the

hour.

- Advertising Guidelines: The Advertising

Standards Council of India ("ASCI"), the independent body

regulating advertising content in India and has issued specific

guidelines for advertising and promotion of virtual digital assets

and services, including cryptos on March 8, 2022 titled

'Guidelines for Advertisements of Virtual and Digital Assets

and Services' ("ASCI Guidelines").4 The

purpose of these guidelines is to provide advertisers and

advertising agencies with clear and comprehensive rules for

advertising and promoting virtual and digital assets and services

in a manner that is truthful, honest, and not misleading.

The ASCI Guidelines cover various aspects of advertising, including the use of endorsements and testimonials, the depiction of risk and safety, and the clarity and adequacy of disclosures, specifically by celebrities and prominent personalities. The ASCI Guidelines also require a categorical disclaimer to be made to the general public regarding the risky nature of VDAs and the potential unrecoverable loss of funds which may result from investments being made in VDAs.5 Additionally, advertisements are prohibited from portraying VDA products as being regulated in India or being compared to regulated asset classes.

- Caution to Investors due to the Unregulated Nature of

Crypto: Sectoral regulators have also cautioned investors

in relation to investments made in VDAs. The RBI had also issued

circulars in relation to the unregulated nature of crypto assets in

India, clarifying to users, holders, and traders of VDAs the

immense risk associated with an investment in an unregulated asset

class.6 The Union Ministry of Corporate Affairs has also

amended the Companies Act, 2013, requiring companies to disclose

any transactions in relation to VDAs in their balance

sheets.7 SEBI, in its responses to the Parliament

Standing Committee on Finance has also suggested the applicability

of existing laws like the Foreign Exchange Management Act, 1999,

Banning of Unregulated Deposit Schemes Act, 2019 and the Consumer

Protection Act, 2019 to endorsements of VDAs made in violation of

such laws.

Accordingly, from a regulatory perspective, there is a need to ensure that exposure to virtual assets is carried out through verified channels, after proper due diligence, in order to prevent larger macroeconomic impacts from any untoward incidents in the virtual asset industry. Issuance of SOPs may be helpful in this regard, to appraise entities involved in the banking and financial sector of the prevailing regulatory stance regarding virtual assets, requisite risk assessment practices, and guidance on broader impacts and avoidance of the same by such entities.

Access to Law Enforcement Agencies (LEAs) to Address Fraudulent Activities (AML/CFT)

- Issue of Jurisdiction: The primary issue with

VDAs is that VDA transactions seem to exist in a parallel space

where international boundaries and jurisdiction are in abeyance.

Most of the commentary around VDAs and the jurisdictional issues

faced by law enforcement agencies in clamping down on crypto-fueled

financial crime sees jurisdiction as a primary

challenge.8 The silver lining is that the lack of

centrality and domicile seems to be every regulator's problem

and can be tackled if agencies act in lockstep. Jurisdictional

issues are a matter of procedure and need to be dealt with at the

international level. Appropriate Conflict of Laws rules can be

formulated to deal with the post-investigation adjudication

stage.

- Issue of Inquiry and Investigation: At the

investigation stage, a robust system of inter-agency networks needs

to be put together for information sharing and cooperation. India

can take the lead in inter-agency information sharing and making

its financial systems available for investigation by other

agencies. A standard operating protocol, in line with international

best practice, as reflected in FATF Guidance for a Risk-Based

Approach to Virtual Assets and Virtual Asset Service Providers

(VASPs) must be adopted.9 India has taken a robust step

in this direction by including VDA Service providers in the

PMLA and can leverage its G20 presidency in heralding multilateral

cooperation in enabling VDA transactions with regulatory

oversight.

- VDAs under India's Money Laundering

Framework: As stated in the above point, India has made

notable advances in preventing the use of VDAs under money

laundering regulations. Reiterating India's commitment to the

Vienna Convention on combating money laundering, drug trafficking,

and countering the financing of terror (CFT), all crypto

transactions have been brought under the ambit of the Prevention of

Money Laundering Act, 2002 from March 7, 2023.10

Reporting requirements inscribed into the existing AML framework

under the Prevention of Money Laundering Act, 2002 now apply to

virtual asset providers equally. Further, transaction-related

information has also been mandated for reporting if it falls under

the category of "suspicious transactions".

- CERT-In Mandate for Cyber Incidents: Recently, the Indian Computer Emergency Response Team (CERT-In) issued new guidelines for cyber incidents.11 These rules have introduced record-keeping and KYC mandates for VASPs and custodian wallet service providers. The mandate is exhaustive enough to reconstruct the transaction in case of a cyber incident involving VDA transactions. These rules have been formulated based on the experience of CERT-In and the difficulties it has faced while investigating cyber fraud. In this manner, they ensure a timebound process to clamp down on the malicious use of VDAs.

Regulatory Arbitrage

- Absence of Uniform Regulation: Crypto assets

are functioning amidst varying jurisdictional oversight owing to

the absence of global governance or international standards. Given

its architecture, it may be excluded from the definition of

conventional securities. It thus operates outside any established

regulatory frameworks, thereby being vulnerable to regulatory

arbitrage. Lack of market transparency, clarity about client asset

custody, etc. can further lead to asymmetries that can cause voids,

loopholes, redundancies, and contradictions.

- Existence of Non-Integrated Crypto Exchanges:

Multiple non-integrated and non-compliant crypto exchanges have

propped up within the crypto ecosystem, which are independently

owned and exist in parallel across countries. On an individual

basis, the majority of these exchanges function like traditional

equity markets where traders submit, buy and sell orders, and the

exchange clears trades based on a centralized order book. However,

in contrast to traditional, regulated equity markets, the crypto

asset market lacks any provisions to ensure that investors receive

the best price while executing businesses.

- Deviations in Crypto Asset Prices: It has also

been observed that there exist deviations in crypto asset prices

across different exchanges, which are likely to persist for several

days and weeks. Studies have suggested that this arbitrage is

larger for exchanges across different countries than within the

same country. The absence of regulatory mechanisms increases the

role of arbitrageurs who can trade across different markets

heterogeneously and any constraints to the arbitrage capital flow

may result in market segmentation.12

- Co-opetition Approach for Crypto Regulations: The regulatory framework for crypto assets should follow a 'Co-opetition Approach', a term coined by renowned academicians Adam M. Brandenburger and Barry J. Nalebuff in 1996, where the principles of competition and cooperation are paid weightage while taking public policy decisions. This approach focuses on minimizing the chances of regulatory nationalism by attempting to balance domestic, political, and economic interests with international expectations. The recommendation aligns with the views of senior IMF counsel, Marianne Bechara, who believes that crypto regulatory frameworks need to be coordinated internationally but tweaked to meet local differences.

Financial Stability

- Regulatory Concerns in India: The RBI has been

vocal about the risks that virtual digital assets may pose to

traditional banking and financial institutions and to India's

financial stability. In 2018, the RBI issued a circular banning any

regulated entities, including banks, from dealing in crypto.

However, this ban was challenged and struck down by the Supreme

Court of India ("Supreme Court") in

the Internet and Mobile Association of India v. Reserve Bank of

India case.13 Even as the Supreme Court struck down the

ban under the circular, it had noted that - "Irrespective

of what VCs actually do or do not do, it is an accepted fact that

they are capable of performing some of the functions of real

currencies. Therefore, if RBI takes steps to prevent the gullible

public from having an illusion as though VCs may constitute a valid

legal tender, the steps so taken, are actually taken in good

faith.".

- Dollarisation of the Indian Economy: While the

RBI has generally recognized the benefits that cryptography and DLT

may provide to the financial sector, it has identified that there

exist broader financial and macroeconomic risks that are associated

with private virtual digital assets (like private cryptos, and more

broadly, for all private currencies). The use of private currency,

including virtual digital assets and crypto, results in the

"dollarisation" of the Indian economy - which refers to

the use of parallel currency in financial transactions. At times,

the use of crypto leads to literal dollarisation, if stablecoins

linked to the dollar start being increasingly utilised in financial

transactions. Acceptance of Cryptos as legal or acceptable tender

would adversely affect the integrity of the capital account regime,

as policy control on capital flows would be eroded. The consequence

of this on foreign exchange reserve accretion and exchange rate

management raises serious macroeconomic stability issues.

- Diminishing Credit Creation and Mobilisation:

Crypto priced in convertible currencies like the Euro and Dollar

may diminish the Indian banking system's ability to mobilise

deposits in Rupees. Additionally, utilisation and adoption of such

crypto would also reduce the banking system's ability to create

credit and would further reduce the impact of the government's

monetary policies on credit creation in relation to the foregoing

convertible currencies.

- Reducing Sovereign Control over Monetary and Fiscal

Landscape: Considering that most virtual currencies and

virtual digital assets are controlled solely by corporate

enterprises, utilisation of such currencies for transactions will

reduce the impact of government control on monetary policy and

impair financial and macroeconomic stability of the country.

Accordingly, the RBI has clarified that private virtual digital assets and crypto do not qualify as legal tender in India. Importantly, the RBI has introduced the central bank digital currency ("CBDC") of India called Digital Rupee or e₹, which incorporates the unique advantages of central bank money, namely, trust, safety, liquidity, settlement finality and integrity. Through the CBDC, the RBI aims at providing the public with benefits that virtual currencies or blockchain based currencies offer. Further, through the CBDC, the RBI intends to route investors in virtual digital assets to adopt the e₹ for conducting transactions in place of private virtual digital assets. This enables sovereign control over Indian currency, while providing tangible benefits of DLT to entities engaged in financial transactions, within the legal and regulatory framework of India. But it must be noted here that CBDCs and VDAs are two independent technologies, aimed at solving different things, and hence can coexist. While one is a legal tender, the other is the representation of blockchain which incentivises truly decentralized ledgers. Assuming that CBDCs could solve for what VDAs offer, and vice versa would not be entirely accurate.

Click here to continue reading . . .

Footnotes

1. Indias-1-Trillion-Digital-Asset-Opportunity.pdf (crosstower.com)

2. Sections 115BBH, Section 194S and Section 56 of the Income Tax Act, 1961 (as amended by Finance Act 2022).

3. News report available here.

4. ASCI guidelines can be accessed here

5. The guidelines require the following disclaimer to be made - "Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions."

6. RBI's public notices dated December 24, 2013, February 01, 2017 available here and December 05, 2017 available here. These were later challenged in the Internet and Mobile Association of India v. Reserve Bank of India case (2020 SCC OnLine SC 275).

7. Corporate Affairs (MCA) notification dated 24.03.2021 available here

8. Columbia Journal of Transnational Law publication "Crypto exchange's jurisdiction-shopping: a regulatory problem that requires a global response" dated 23 February, 2023, Kaal, W.A. and Calcaterra, C., 2017. Crypto transaction dispute resolution. The Business Lawyer, 73(1), pp.109-152., Salmon, J. and Myers, G., 2019. Blockchain and associated legal issues for emerging markets.

9. Financial Action Task Force, 'Updated Guidance for a Risk-Based Approach to Virtual Assets and Virtual Asset Service Providers', (2021). This can be accessed here.

10. Notification No. S.O. 1072(E)., Dated 07.03.2023, available here

11. CERT-In, "Directions under sub-section (6) of section 70B of the Information Technology Act, 2000 relating to information security practices, procedure, prevention, response and reporting of cyber incidents for Safe & Trusted Internet" No. 20(3)/2022-CERT-In dated 28 April, 2022 available here.

12. Volume 135 of the "Journal of Financial Economics" dated February 2020 available here

13. 2020 SCC OnLine SC 275.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.