The Securities and Exchange Board of India ("SEBI") has issued a Circular on June 6, 2024, introducing 'financial disincentives' for market infrastructure institutions ("MIIs") i.e., stock exchanges, clearing corporations, and depositories. This Circular outlines the Surveillance Related Lapses, the financial disincentive which can be levied on MII and the procedure to be followed. The amount of financial disincentive for Surveillance Related Lapses will be calculated based on the MII's total annual revenue from the preceding financial year and the frequency of such lapses during that year.

Surveillance Related Lapses ("SRL") are defined as any lapse observed in discharge of surveillance activities; any inadequate reporting or non-reporting of surveillance-related activity; or any lapse in implementing the decisions taken during the surveillance meetings including any non-implementation or partial implementation or delayed implementation of any decision or communication of SEBI as per agreed scope and timelines.

The purpose of the Circular is to establish a system of Financial Disincentives for Surveillance Related Failures ("FDSRL") for MIIs, but we think that it has some legal flaws that may compromise its integrity.

The Circular should have been issued under SCRA and the Depositories Act and not under the SEBI Act

The Circular in question is promulgated under Section 11(1) of the Securities and Exchange Board of India Act, 1992 ("SEBI Act"). However, Section 11(2) mandates that SEBI's functions and powers should align with the Securities Contracts (Regulation) Act, 1956 ("SCRA"), which governs stock exchanges and clearing corporations, and the Depositories Act, 1996 ("Depositories Act"), which oversees depositories. SEBI is empowered under Section 31 of the SCRA and Section 25 of the Depositories Act to enact regulations consistent with the provisions of these acts. The failure to invoke the authority granted by the SCRA and the Depositories Act in the creation of the Circular suggests that it exceeds the legal boundaries set by the SEBI Act.

The procedure prescribed under the Circular is ultra-vires the provisions of the SEBI Act, SCRA and Depositories Act.

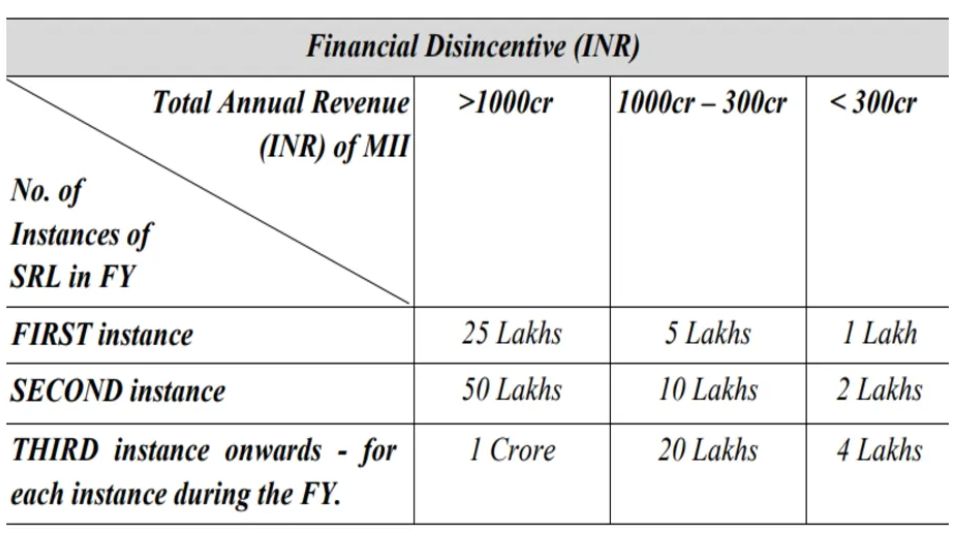

The Circular prescribes that the financial disincentives shall be determined on the basis of total annual revenue of the MII during the previous financial year and the number of instances of SRL during the financial year:

Before proceedings forward, it is to be noted that "financial disincentive"1 means a pre-defined penalty structure.

The circular outlines that once SRLs are identified, SEBI before imposing any penalty/s must provide an opportunity to the concerned MII to present their submissions, which will be considered. It's crucial to note that SEBI's authority to impose penalties is defined under sections Chapter VI-A of the SEBI Act, Chapter IV of the Depositories Act, and the SCRA which mandate an adjudication process by SEBI. The provisions stipulate that penalties can only be imposed "after holding an inquiry in the prescribed manner" and through an adjudication order. The Central Government has established the SEBI (Procedure for Holding Inquiry and Imposing Penalties) Rules, 1995 ("AO Rules"), under section 292 of the SEBI Act, detailing the inquiry process and penalty imposition under the SEBI Act. Similarly, the Central Government has also framed rules under the SCRA3 and the Depositories Act4.

Consequently, SEBI is authorized to levy penalties solely through adjudication orders, following the procedure outlined in the SEBI Act in conjunction with the AO Rules.

However, the circular appears to have two significant flaws. Firstly, it prescribes a procedure to levy penalty, which is beyond the scope of the SEBI Act, as the AO Rules already define this process. Secondly, it specifies penalty amounts, which is already mentioned under the SEBI Act, SCRA and Depositories Act which provides for penalties under various circumstances, including residual provisions5. Therefore, in our opinion the circular exceeds the legal boundaries of the SEBI Act.

Most importantly, the procedure to hold inquiry and levy penalty upon the stock exchanges/clearing corporations and depositories have been laid down in the SCRA6 and the Depositories Act7, respectively. Since the Circular has not invoked the powers under those acts, no penalty can be levied upon the MIIs.

One might contend that the Circular is an exercise of SEBI's administrative functions and therefore, the "financial disincentive" imposed by it is not an appealable order under the SEBI Act. However, this may be hard to accept, given the nature of the Circular. The Circular provides for an opportunity to make representations before any penalty is imposed - a procedure that is followed in quasi-judicial functions. In this regard, the Hon'ble Supreme Court in its ruling in Indian National Congress (I) vs Institute of Social Welfare & Others8 dated May 10, 2022, stated as follows:

"Where (a) a statutory authority empowered under a statute to do any act (b) which would prejudicially affect the subject (c) although there is no lis or two contending parties and the contest is between the authority and the subject and (d) the statutory authority is required to act judicially under the statute, the decision of the said authority is quasi-judicial.

What distinguishes an administrative act from quasi-judicial act is, in the case of quasi-judicial functions under the relevant law the statutory authority is required to act judicially. In other words, where law requires that an authority before arriving at decision must make an enquiry, such a requirement of law makes the authority a quasi-judicial authority.

A quasi-judicial function is an administrative function which the law requires to be exercised in some respects as if it were judicial. A typical example is a minister deciding whether or not to confirm a compulsory purchase order or to allow a planning appeal after a public inquiry. The decision itself is administrative, dictated by policy and expediency. But the procedure is subject to the principles of natural justice, which require the minister to act fairly towards the objections and not (for example) to take fresh evidence without disclosing it to them. A quasi-judicial decision is therefore an administrative decision which is subject to some measure of judicial procedure."

On a reading of the above judgement, the powers to be exercised by SEBI under the Circular is more of a quasi-judicial function than a mere administrative task.

On a demurrer, considering that the power to levy penalty as prescribed under the Circular to be an administrative function, there would be no recourse for initiating the recovery proceedings in case where the MIIs defaults on the payment of penalty. It may be noted that the power of recovery under the SEBI Act is applicable inter-alia in cases of failure to pay the penalty imposed under the act9. Since the Circular prescribes penalties while disregarding the Act's stipulations, SEBI would not be able to exercise recovery powers in these instances. Consequently, SEBI lacks the recourse to recover such penalties.

The penalty amount is to be credited to the Consolidated Fund of India

Section 15JA of the SEBI Act lays that "All sums realised by way of penalties under this Act shall be credited to the Consolidated Fund of India". However, in a sharp contrast, the Circular lays that "The "Financial Disincentive(s)" under the framework of FDSRL, if imposed, shall be credited by the MII concerned within 15 working days, to the Investor Protection and Education Fund ("SEBI–IPEF") established under the SEBI Act, 1992" It is a settled law that if a statute confers power to do a particular act and has laid down the method in which that power has to be exercised, it necessarily prohibits the doing of the act in any manner other than that which has been prescribed10. Thus, the provision to credit financial disincentive (which is akin to penalty) to the IPEF is in contradiction of the provisions of the SEBI Act.

Sanctity of surveillance meetings

As mentioned above, SRL includes any lapse observed in the implementation of decisions taken during the "Surveillance Meetings". There have been some instances in the past where the integrity of the decisions made during the surveillance meetings or mere communication from SEBI to exchanges have been questioned. In the matter of 52 Weeks Entertainment Ltd. v. SEBI and Anr.11, BSE suspended trading in the securities of a company based on SEBI's directions from a surveillance meeting. Though the suspension order was set aside, the questions regarding the sanctity of the decisions taken in the surveillance meeting was not gone into. In the case of J. Kumar Infraprojects Ltd. v. SEBI12, the Hon'ble SAT had stayed SEBI's communication to the exchanges due to which the exchanges had moved the scrip of the company in the GSM category. In another case of Axis Bank Limited v. SEBI and Ors.13, the NSDL had transferred securities from the demat account of Karvy Stock Broking Limited to its clients "as per the directions of SEBI and under supervision of NSE". Though there is no such formal direction issued by SEBI, the Hon'ble SAT held that "The action of NSDL under the directions of SEBI were wholly illegal and invalid". Thus, the question pertaining to the legal sanctity of the decisions taken during the surveillance meetings is another issue which needs attention.

Conclusion

In summary, the SEBI Circular on financial disincentives for MIIs presents a series of legal and procedural challenges that question its validity and enforceability. The circular's departure from the established legal framework, as outlined by the SEBI Act, SCRA and the Depositories Act, and its inconsistency with the penalty proceedings under the SEBI Act questions its validity. Furthermore, the stipulation for the penalty amount to be credited to the SEBI-IPEF, contrary to the mandate of crediting to the Consolidated Fund of India, is another critical oversight that cannot be overlooked. The sanctity of surveillance meetings, which are crucial in the implementation of decisions affecting the market, has been previously questioned and remains a concern. It is, therefore, incumbent upon SEBI to reassess the circular in its entirety, address the highlighted loopholes, and align its provisions with the statutory mandates to ensure that the regulatory measures are legally sound and operationally feasible. The withdrawal and reissuance of the Circular, with due consideration to the statutory framework and judicial precedents, would not only uphold the legal sanctity of SEBI's directives but also fortify the confidence of the market participants in the regulatory body's commitment to the principles of justice and equity.

Originally published in BW Legal World

Footnotes

1 The SEBI circular issued on July 05, 2021, outlines a 'Standard Operating Procedure' for addressing technical issues at Market Infrastructure Institutions (MIIs). It mandates a "pre-defined penalty structure" for any operational downtime that exceeds the specified threshold. Consequently, the circular introduces 'Financial Disincentives' as a form of penalty for such infractions.

2 Section 29 (1) of the SEBI Act lays that "The Central Government may, by notification, make rules for carrying out the purposes of this Act."

3 Securities Contracts (Regulations) (Procedure for Holding Inquiry and Imposing Penalties) Rules, 2005

4 Depositories (Procedure for Holding Inquiry and Imposing Penalties) Rules, 2005

5 SEBI has the power to levy penalty under section 15A, 15B, 15C, 15D, 15E, 15EA, 15EB, 15F, 15G,15H, 15HA and 15HB of the SEBI Act. Section 15HB is a residuary provision which provides for "Penalty for contravention where no separate penalty has been provided" and the penalty in such cases shall not be less than one lakh rupees but which may extend to one crore rupees.

6 Section 12A (2) and 23-I of the SCRA.

7 Section 19(2) and 19H (1) of the Depositories Act.

8 2002 AIR SCW 2245

9 "28A. (1) If a person fails to pay the penalty imposed 174under this Act or fails to comply with any direction of the Board for refund of monies or fails to comply with a direction of disgorgement order issued under section 11B or fails to pay any fees due to the Board, the Recovery Officer may draw up under his signature a statement in the specified form specifying the amount due..."

10 Dharani Sugars and Chemicals Limited vs. Union of India & Others (2019) 5 SCC 480.

11 SAT Order dated March 13, 2015 Appeal No. 23 of 2015

12 SAT Order dated August 10, 2017 Appeal No. 174 of 2017

13 SAT Order dated December 20, 2023 Appeal No. 35 of 2020

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.