- with readers working within the Banking & Credit industries

- with readers working within the Banking & Credit industries

- within Antitrust/Competition Law, Environment and International Law topic(s)

1. ELTIF: DISTRIBUTING ALTERNATIVE STRATEGIES TO NON-PROFESSIONAL INVESTORS

Regulation (EU) 2015/760 on European long-term investment funds (ELTIF) has been amended by the revised ELTIF Regulation which is applicable since 10 January 2024.

On 19 July 2024, the European Commission published the draft delegated regulation supplementing the ELTIF Regulation (Draft RTS). This text is currently subject to a 3-month scrutiny period by the European co-legislators (subject to a possible extension of additional 3 months). It is expected that the Draft RTS will enter into force before the end of the year 2024.

The Luxembourg industry (and Elvinger Hoss Prussen in particular) have played an instrumental role historically in structuring investment products accessible to retail investors. More recently, we have been structuring investment funds, whether openended or closed-ended, that provide alternative strategies to non-professional investors.

These 'democratized' vehicles have been structured mainly as ELTIFs or Luxembourg undertakings for collective investment setup under part II of the Law of 2010 or the combination of ELTIFs and Part II structures. The Part II fund is a Luxembourg domestic AIF that may accept all types of investors, including retail.

The ELTIF regime enables alternative investment fund managers to market their AIFs in the EEA with a passport to retail investors. Part II funds have been well-known to investors beyond the EEA for several decades.

An ELTIF may be set-up as a Part II fund (or a compartment thereof) to release the full potential of its retail marketing passport.

2. OVERVIEW OF LUXEMBOURG INVESTMENT VEHICLES

3. ELTIF KEY FEATURES

- Alternative investment fund (AIF) – subject to AIFMD

- Managed by an authorised AIFM – no subthreshold AIFM

- Authorised and supervised by the financial regulator (CSSF) – for compliance with ELTIF Regulation aspects

- Authorisation at the level of the sub-fund - possible to add ELTIF sub-funds to an existing structure

- EU marketing passport for professional and retail investors – unique advantage for AIFs

- Objective to facilitate the raising and channeling of capital towards long-term investments in the real economy

- The ELTIF Regulation is directly applicable in all EU countries

- Member states are not allowed to add requirements in the field covered by the ELTIF Regulation (art. 1 paragraph 3)

- Notification procedure as per AIFMD for both professional and retail investors

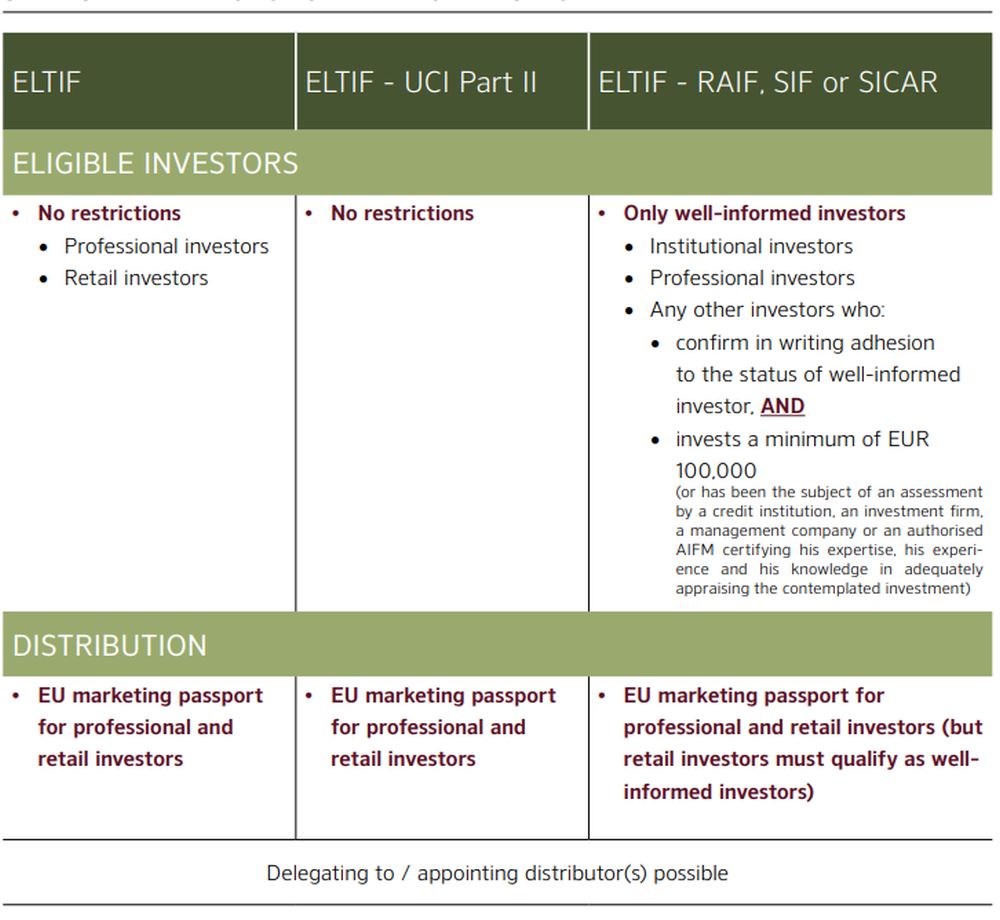

5. ELIGIBLE INVESTORS AND DISTRIBUTION

6. MARKETING TO RETAIL INVESTORS – ADDITIONAL REQUIREMENTS

Suitability test

- Obtaining information about retail investor (MIFID

II):

- their knowledge and experience in the investment field

- their financial situation

- their investment objective

- Providing statement on suitability (MIFID II)

- Express consent of investor possible in case of negative statement

- No MIFID II license required for AIFM marketing directly

Depositary – additional requirements (application of UCITS depositary regime):

- Entity authorised to act as depositary for UCITS (e.g. credit institution)

- No discharge of liability in the event of loss of financial instruments held by a 3rd party

- Liability of depositary cannot be excluded or limited

- Assets cannot be reused by depositary

PRIIPs Regulation

- PRIIPS KIDs

AIFMD

- Facilities: arrangement in host country(ies) to inform investors, handle orders, liaise with regulator... (no physical presence required)

7. ELTIF SECONDARY MARKET

- Listing of ELTIF possible

- Allowing free transfer of shares/units/interests is

mandatory

- subject to complying with regulatory requirements and conditions set out in the prospectus

- Possibility to provide for full or partial matching of

transfer requests between existing and potential investors

as detailed in the Draft RTS

- subject to conditions set out in a detailed policy (role of AIFM, timing, price, ratio, costs and fees)

To view the full article, click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.