- within Tax topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- in European Union

- in European Union

- in European Union

- in European Union

- in European Union

- with readers working within the Accounting & Consultancy and Law Firm industries

I. INTRODUCTION

With this publication, we shall explore the notion of management and control as this is applicable in Cyprus and affects the taxation of Cyprus and Overseas companies.

II. THE LAW

Basis of Taxation

A company or an individual are taxed in Cyprus, subject to specific exceptions1, if they are residents of Cyprus.

The residency requirement as the basis of taxation, is provided in article 5(1) of the Income Tax Law, No. 118(I) of 2002 as amended, herein after referred to as the "Income Tax Law".

Article 5(1) of the Income Tax Law provides the following:

"Subject to the provisions of this law, in the case of a person who is resident in the Republic, tax shall be charged at the rate or rates specified hereinafter for each year of an assessment upon the income accruing or arising from sources both within and outside the Republic, in respect of: ..."

Meaning of Resident in the Republic

The meaning of "resident in the Republic" is defined in the Income Tax Law article 2 which provides the following:

"Resident in the Republic, when applied to an individual, means an individual who stays in the Republic for a period or periods exceeding in aggregate 183 days in the year of assessment and when applied to a company, means a company whose management and control is exercised in the Republic and "non-resident or resident outside the Republic" shall be construed accordingly: ...".

Pursuant to this provision, a company is considered to be resident of Cyprus, and in effect liable to Cyprus taxation, when its "management and control" is exercised in Cyprus.

In addition to the above meaning of resident in the Republic, as from 01.01.2023, a company which is established or registered pursuant to any law in force in Cyprus, will by default be considered as resident of Cyprus, provided it is not tax resident in any other country.

In Article 2 of the Income Tax Law, the proviso of the definition of the meaning of "Resident in the Republic", provides the following:

"It is provided that, a company which has been established or registered pursuant to any law in force in the Republic, it is considered that it is resident in the Republic, unless the said company is tax resident in any other country".

This provision is applicable as from 01.01.2023.

Meaning of Company

The Income Tax Law, in article 2, identifies the notion of company to be "any legal body registered either in Cyprus or abroad".

Taxation of Companies

As per the above provisions of the Income Tax Law, a company:

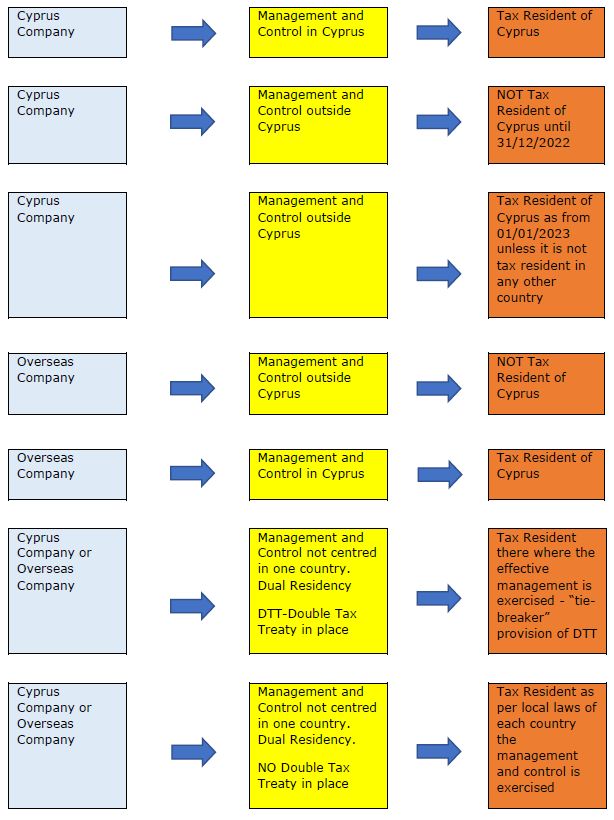

- If it is incorporated in Cyprus with management and control in Cyprus, it is tax resident of Cyprus;

- If it is incorporated in Cyprus with management and control outside Cyprus, it is NOT tax resident of Cyprus. As from 01.01.2023, such company, it will be tax resident of Cyprus, unless it is tax resident in any other country2;

- If it is incorporated outside Cyprus but its management and control is in Cyprus then it is tax resident of Cyprus.

Note: A special case might arise when a company has dual residency. This happens when there is fragmentation of the management and control in various countries. In such a case, if a Double Tax Treaty (DTT) between the relevant countries is in force, the company will be tax resident in the country where its effective management lies. In case of no Double Tax Treaty is in force, the company will be tax resident as per the applicable laws of each country where the management and control is exercised.

A non - Cyprus tax resident company, despite the fact that it is not tax resident of Cyprus, is taxed on income accrued or arising from a business activity which is carried out through a permanent establishment in Cyprus and/or from sources in Cyprus.

In addition, all companies tax residents of Cyprus are taxed on their income accrued or arising from sources in Cyprus and/or abroad. With effect as from 1 January 2019 Controlled Foreign Company (CFCs) rules apply, i.e., non-distributed profits of CFCs directly or indirectly controlled by a Cyprus resident company, may become subject to tax in Cyprus - certain exceptions apply. Foreign taxes paid can be credited against the Cyprus corporation tax liability.

III. MANAGEMENT AND CONTROL – DEFINITION

There is no definition in the Income Tax Law or in any other enactment as to the meaning of the notion of "management and control" which will identify whether a company is tax resident of Cyprus or not.

There is no definition in the law, stating who exercises management and control and how it is exercised. There is also, no definition in the law as to what particular acts constitute the management and control.

Having in mind this interpretation gap as to the meaning of "management and control" in the Cyprus legislation, we shall request assistance from any court judgements interpreting this notion. By operation of article 29 (1) (c) of the Courts of Justice Law no. 14/60 as amended, Common Law3 and the Principles of Equity4, are among the sources of the Cyprus legal system, provided they do not come in conflict with local statutes.

In this respect, since the Cyprus legal system, is also based on the Common Law system and the Principles of Equity, we may refer to English court cases, in the absence of Cyprus court cases, in order to interpret the meaning of "management and control" as it is abstractly laid down in article 2 of the Income Tax Law. There are no Cyprus court cases interpreting the management and control principle.

IV. ENGLISH LAW CONCERNING THE RESIDENCY OF A COMPANY

The management and control test to identify the residency of a company was applicable in the UK until 1988 for UK registered companies. In 1988, it was replaced by relevant statutory provision, (Finance Act 1988), and now all UK registered companies are automatically treated as tax residents of UK, taxable in UK, irrespectively of their place of management, unless they can show that their place of effective management is in a country with which UK has relevant double tax treaty5. In this case the so called, "Tie – breaker" article of the OECD model treaty as to effective management, usually included in all double tax treaties signed among the countries, apply and controls the tax residency.

The management and control test, which is the Common Law test of corporate residence, irrespectively of the above statutory provision which applies automatically to UK companies, is according to the UK law, applicable to non-UK companies – foreign registered companies.

Under these Common Law provisions, a foreign company i.e., Cyprus, BVI etc., might be taxable in the UK if their central management and control is exercised in the UK.

This corporate residency test is a fundamental concept of international corporate taxation and is the tool of income tax authorities to impose taxation on foreign / overseas companies for their activities undertaken abroad BUT managed and controlled onshore.

In view of the provisions of the UK law as above indicated, there is a considerable number of court decisions which deal with the interpretation of the management and control test and from which we are getting guidance as to how this test will be applied in Cyprus, if a case arise and interpretation of this term will be required by the Cyprus authorities and courts.

In this respect, since our legal system is based on the Common Law and the Principles of Equity, our courts and the Commissioner of Income Tax, it is expected to follow the principles laid down by UK authorities in interpreting the term "management and control". English court cases, will give the guidance for Cyprus in the interpretation of the management and control test.

V. INTERPRETING THE MANAGEMENT AND CONTROL TEST

In the following chapters we shall deal with the notion of management and control and we shall try to identify its core elements. In this respect we shall examine:

- Where is a company tax resident according to the management and control test and when is a company tax resident of Cyprus?

- Which company body exercises the management and control?

- Which are the factors identifying where the management and control is exercised; and,

- How the management and control must be exercised in order for a company to be considered tax resident of Cyprus?

VI. ANALYSIS

A. Where is a company tax resident according to the management and control test and when is a company tax resident of Cyprus?

1. The leading case on company residency is De Beers Consolidated Mines Ltd v Howe [1906] AC 455, 5 TC 198. In this case it was established that a company resides, for tax purposes, there where its real business is carried out. In the same case it was decided that the real business of a company is carried out, not there where the trading operations are taking place, but where the central management and control of its business actually takes place, as said in the judgement, there "where the central management and control actually abides".

As per the facts of this case, the company was incorporated in South Africa and the whole of its profits were made from mining and disposal of diamonds. The head office of the company was at Kimberley in the Cape of Good Hope, where general meetings were held. The directors met both in Kimberley, South Africa, and in London but the majority resided and met in London.

It was found as a fact that the chief control of the company's affairs was in the hands of the London directors who controlled the negotiation of contracts, determined policy in regard to the disposal of diamonds and other assets and the working and development of the mines. The House of Lords, confirming the decision in both courts below, unanimously held that the company was resident in the UK. In the course of his opinion Lord Loreburn observed (at p. 213):

"The decision of Chief Baron Kelly and Baron Huddleston, in the Calcutta Jute Mills v Nicholson and the Cesena Sulphur Co. v Nicholson, now thirty years ago, involved the principle that a Company resides, for purposes of Income Tax [now Corporation Tax], where its real business is carried on. Those decisions have been acted upon ever since. I regard that as the true rule; and the real business is carried on where the central management and control actually abides.

It remains to be considered whether the present case falls within that rule. This is a pure question of fact, to be determined, not according to the construction of this or that regulation or byelaw, but upon a scrutiny of the course of business and trading."

De Beers is a case where the majority of the directors of the overseas company, incorporated in South Africa, were reside and met in London and the company was held to be resident in the UK for tax purposes.

2. Important is also the Court of Appeal case in Bullock v Unit Construction Co Ltd (1959) 38 TC 712 at 729 – 730 also at, [1960] AC 351.

The Facts:

The case concerned a UK-resident subsidiary of Alfred Booth & Co Ltd, a UK-resident parent company. This subsidiary made certain payments to three fellow subsidiaries in Kenya and claimed these as allowable business expenses in arriving at its UK taxable profits. However, these payments would only have been allowed for tax purposes if the three subsidiaries to which they were made were resident in the UK, not Kenya. They were incorporated in Kenya and their Articles of Association expressly stated that management and control rested with the directors and also required directors' meetings to be held outside the UK. Presumably this had been done with the intention of protecting the company from any future accusation of residence outside Kenya.

The Issue:

Whether the companies were resident in the UK and thus taxable in UK.

Held:

It was found as a fact that due to trading difficulties at the material times the boards of directors of the Kenyan subsidiaries were standing aside in all matters of importance and also many matters of minor importance affecting the central management and control and that real control of them was being exercised by the Board of Alfred Booth & Co Ltd in London. Therefore, all subsidiaries physically located in Kenya were in fact UK tax residents.

This case confirmed the view that, where the business of a subsidiary of a company is under the control of the directors of its holding company, it is the place at which that control is exercised and not the residency of the subsidiary's directors, that determines the residence of the subsidiary.

Bullock is a case where the foreign subsidiaries, incorporated in Kenya, were managed and controlled by the board of directors of the holding company situated in UK and the subsidiary companies was held to be resident in the UK and thus taxable in UK.

Place of management and control Vs. Place of business operations of the company

The central management and control of the business must be distinguished from where the company's business is actually taking place. The management and control of the business need not be in the same place where the actual trading activities and operations of the company are conducted.

3. The same principle has been reconfirmed in R v Dimsey (1999) STC 846, where the court emphasised that the central management and control test is a composite test designed to identify where the decisions of fundamental policy are made as opposed to the place where the day - to - day profit earning activities are undertaken. Central management and control of the business must be distinguished from (and need not be in the same place as) the place of business, where the actual trading and business operations of the company are conducted. We need to distinguish where the decisions of fundamental policy are made as opposed to the place where the day-to-day profit earning activities are undertaken.

The central allegation in those cases was that companies incorporated in Jersey and other tax heavens, and of which Mr Dimsey, a solicitor, was a Jersey resident director, were in fact centrally managed and controlled in the UK, such that the companies were liable to UK corporations' tax. The evidence accepted by the jury was that Mr Dimsey's client in the UK (Mr Allen), who was not an actual director, was a shadow director, and was in fact actually managing and controlling the companies in respect of board level decisions. The result for the companies was that they were resident in the UK rather than Jersey.

R v Dimsey is a case of a shadow director residing in UK who was instructing the company director residing in Jersey how to act6.

4. In addition, In Trevor Smallwood Trust v HMRC [2010] EWCA Civ 778, the Court of Appeal confirmed that a Mauritian trust that has been arranged and orchestrated in the UK was ultimately controlled and managed in the UK.

This was a case about the residence of a trust, not about a company and although there are important differences between a Trust and a Company ,the concept of management and control is applicable in the same way.

The facts:

Mr. Smallwood was the settlor and beneficiary of two trusts established for himself and his family in 1989 and he also had the power to appoint trustees. The trusts were based in Jersey and held shares in companies and the shares grew in value. There would potentially be a capital gain of over £6million on their disposal. The taxpayer appointed trustees in Mauritius. He relied on the double tax convention between the UK and Mauritius which has the effect of transferring the right to tax the gain in Mauritius, where the trustees were based at the time of the disposal of the shares property of the trust. The trustees sold the shares and considerable profit was made. Shortly afterwards the taxpayer and his wife, who were based in the UK, both became trustees. HMRC raised an assessment on the trust for £2.7million. The taxpayer appealed.

The issue:

Whether the gain which arose on the disposal of the shares done by the trustees in Mauritius, was exempt from capital gains tax in the United Kingdom.

The Decision of the commissioners

The commissioners found for HMRC: the place of effective management of the trust had been where Mr Smallwood was located, i.e., in UK. He directed and orchestrated the trust from UK. So, the income was taxable in UK.

Held on Appeal:

The Court of Appeal confirmed the commissioner's findings that the trust was managed from UK so the assessment and taxation imposed was correct.

Trevor Smallwood Trust is a case where the foreign trustee who conducted the trust business abroad, was in effect following the instructions of the settlor and beneficiary resident in UK. It was held that the taxation imposed on the settlor and beneficiary for the overseas activity was correct.

In conclusion, the tax residency of a company is identified by determining where the central management and control is exercised. If the central management and control is exercised in/from Cyprus then the company, anywhere registered, is a tax resident of Cyprus.

A Cyprus registered company with central management and control outside Cyprus, as from 01.01.2023, will be tax resident of Cyprus, irrespectively of where the central management and control is exercised, unless it is a tax resident of another country in which case the company will be considered, for Cyprus law purposes, as tax resident of that other country.

In answering the question, where is a company tax resident according to the management and control test, the answer is, at the place where its central management and control is exercised.

In answering the question, when is a company tax resident of Cyprus, the answer is, when its central management and control is exercised in Cyprus, and as from 01.01.2023, all Cyprus registered companies will be tax residents of Cyprus unless a Cyprus company having its management and control abroad is tax resident in another country.

B. Which company body exercises the management and control?

In order to answer the above question, the powers of the directors vs the powers of the shareholders of the company must be considered.

In our legal system, it is a well - established principle, that shareholders control the company through their votes at general meetings, while the directors exercise control of the business of the company by its management. A long line of authorities support this.

In this respect,

Directors ![]() control the business

of the company

control the business

of the company

Shareholders ![]() control the

company

control the

company

The above principle is also specifically adopted in our Companies' Law Cap 113, Table A, Section 80, subject to any special provisions of the articles of association of the company or the law. According to section 80, the directors exercise the day – to – day activities of the company and its administration.

Powers and Duties of Directors

80. The business of the company shall be managed by the directors, who may pay all expenses incurred in promoting and registering the company, and may exercise all such powers of the company as are not, by the Law or by these regulations, required to be exercised by the company in general meeting, subject, nevertheless, to any of these regulations, to the provisions of the Law and to such regulations, being not inconsistent with the aforesaid regulations or provisions, as may be prescribed by the company in general meeting but no regulation made by the company in general meeting shall invalidate any prior act of the directors which would have been valid if that regulation had not been made.

As per the authorities above mentioned7,

".... a Company resides, for purposes of Income Tax [now Corporation Tax], where its real business is carried on. ............... and the real business is carried on where the central management and control actually abides".

In view of the above, it is clear that corporate residence is related to the central management and control of the business of the company, which is exercised by the directors, and NOT to the control of the Company itself, which is exercised by its shareholders.

In effect, the control that we are discussing in this publication, is that which relates to the highest level of management of the company's business and must not be confused with the control which vests in the company's shareholders.

The distinction was laid down emphatically in the old case Stanley v Gramophone and Typewriter Ltd (1908) 5 TC 358.

The facts:

The appellant company (resident in England) held all of the shares in a German company. The appellant company was assessed on the monies retained by the German company, and the case depended on whether the unremitted funds considered as the gains of a business 'carried on' by the English company as opposed to a separate entity.

The Issue:

Whether the appellant company was liable under the Income Tax Act, 1853?

Held:

The Court of Appeal held that the fact that the appellant company owned shares in a German company was not enough to make the business of that German company the business of the appellant company (resident in England). Thus, the appellant company did not bear liability under the Income Tax Act, 1853. The court further held that the directors are not the servants of shareholders. They shall not obey shareholders' directions. They are not the agents of shareholders.

It follows, therefore, that a company whose business is in fact managed and controlled by a board of directors, will be tax resident of that country where the business is managed by the directors and not in the country where the shareholders reside.

In this case it was clearly laid down that corporate residence is related to the central management and control of the business of the company, which is exercised by the directors from the place where they meet and decide its business (and not to the control of the company itself, which is exercised by its shareholders).

The fact that the shareholders through their voting rights can remove the directors from their office does NOT affect the above principles. The business of the company will still be managed and controlled by its board of directors.

In conclusion, the answer to the question, which company body exercises the central management and control of the company's business, is, the board of directors, being the highest management body, which controls the business of the company.

Important note

Despite the above general principle, there are though, in some cases, specifically drafted articles of association of companies, which deprive the directors of the management and administration of the business of the company or give them limited authorities subject to the approval of the shareholders. This is a serious qualification moving the central management and control of the business from the directors to the shareholders and each case must be carefully examined. If such serious step is taken, the company might be considered as tax resident at the place of meetings and decision-making process of the shareholders.

C. Which are the factors identifying where the management and control is exercised?

The question as to where the management and control is exercised, is a matter of fact.

According to the above principles, the management and control is exercised by the board of directors and the place of exercise denotes the residency of the company.

As to Cyprus companies, as from 01.01.2023 all Cyprus registered companies will be considered as tax residents of Cyprus unless they have their management and control abroad and are tax residents in another country.

As to foreign / overseas registered companies, having their management and control in Cyprus, they are considered as tax residents of Cyprus.

We need to identify the facts which the board must undertake or which must be in place, in order to connect the location of the management and control, with Cyprus or any other country.

Location of Board meetings

It has been decided and stressed repeatedly in court cases that, the place where the directors meet in order to reach their decisions on company's policy, finance and related matters, subject to various qualifications which will be discussed further below, will be the place of central management and control of the company's business. If the intention is to have a Cyprus tax resident company, then all board meetings should be held in Cyprus. It is best practice, therefore, to avoid a moving / transit board, since that makes it harder to demonstrate clear residence in any one location and might create issues of multiple residencies.

In effect, the place where the directors meet for their board meetings, deciding on company's policy, finance and related matters, is the location of the central management and control of the company's business and consequently once the other factors are in place, the company is tax resident at that location. Additional considerations will need to be in place which we shall discuss further below.

The recurrent emphasis on the place of directors' meetings must not, however, lead one to suppose that the location of directors' meetings is the only factor used to determine the company's tax residency.

The place of directors' meetings is a significant factor to be taken into consideration but it can be of such importance only if those meetings constitute the medium through which the central management and control is in fact and in reality, exercised, as we shall discuss further below.

Various authorities, among others, support the above principle8.

POSITIVE factors strengthening the Cyprus location of management and control

The following factors, in addition to the basic requirement to hold the board meetings in Cyprus discussed above, will strengthen the management and control test of a company to be connected with Cyprus and the company to be considered as tax resident of Cyprus.

Directors' permanent residence to be in Cyprus

The residence of the directors is closely connected to the place where board meetings are held. If the intention is to have a Cyprus tax resident company, the directors or at least the majority of them must be permanent residents of Cyprus. In this way, it is easily proved that the board meetings have been taking place in Cyprus and the management and control is exercised in Cyprus.

Professional Directors

A board must consist of directors with sufficient knowledge, experience, and expertise to manage the strategic affairs of the company. Directors must be able to consider genuinely the company's affairs and reach a reasonable, commercial decision, justified by the activities of the company and their expertise and knowledge. The directors should be appropriately qualified and experienced in the relevant sector to enable them to consider (rather than merely follow) proposals and reach a reasonable conclusion.

Frequency of Board meetings

Board meetings should be sufficiently frequent to enable the directors to exercise control over the strategic affairs of the company. Depending on the level of activity in the company, a minimum of six board meetings in each year with each board meeting taking no more than two months after the last one.

Decision process – effective consideration and knowledge of the facts

The directors MUST decide the policy and crucial decisions as to the company and NEVER be directed by external bodies. They must think and decide on the key strategic decisions of the company based on sufficient knowledge they must have in order to decide accordingly.

This factor is extensively discussed further below under D. How the management and control must be exercised in order for a company to be considered as a tax resident of Cyprus?

Key Strategic decisions

What are regarded as "key strategic decisions" of the company depends on the nature of the company in question but might include, inter alia, decisions relating to:

- The acquisition or disposal of assets;

- Capital expenditure;

- Budgets approval;

- Operational decisions;

- Financial decisions such as granting or receiving loans;

- Decisions on the engagement or dismissal of directors and other senior personnel;

- Concluding and execution of contracts;

- Mergers and acquisitions;

- Expanding or changing the line of business;

- Appointment of consultants; and,

- Nominating accountants and auditors.

Records and administrative matters

Full and accurate minutes of each board meeting should be taken.

- The time and place of the meeting and who was present.

- What was resolved and the reasons for such resolution should be recorded in as much detail as possible. Discussions in board meetings should be recorded in detail. Any views or debates or agreements or disagreements are important to be recorded in detail as these are important evidence that the directors applied their minds to the relevant questions. Establishing a pattern of decision making is also important. The key point is that these minutes are likely to be more comprehensive than is perhaps the norm.

Copies of notices, agendas and other documentation circulated to directors should be kept at the company's office.

Minutes should be prepared as soon as possible approved and signed.

Decisions of the board should not be made by unanimous written resolutions circulated among the board members as these can suggest "rubber stamping" procedures.

Directors' remuneration

Directors should be paid market price directorship fees and not nominal fees as nominee directors usually receive.

Administrative Office

A fully fletched office must be established in Cyprus where the actual management and control of the company's business will be exercised. In this office, the fundamental policy and management decisions must take place, and the properly recorded board minutes must be kept. The company secretary should be resident of Cyprus and accounting records, corporate records and other significant original documents should be maintained.

Signing of Contracts

Signing of contracts, issuing of invoices, and any other relevant company documents relating to the management, control and administration of the company must be executed in Cyprus by its directors and or local employees properly authorised.

Employees

Employees must be employed and paid reasonable salaries according to market levels.

Stationery

Stationery must be printed with the letterheads of the company and its office address and other contact details such as telephone, fax numbers, email address and website.

Bank accounts

Bank accounts must be opened also in Cyprus and managed by the local directors or employees.

Accounting records

Maintenance of accounting records should be in Cyprus.

NEGATIVE factors weakening the Cyprus location of management and control

The following factors will weaken the management and control of a company being in Cyprus once a Cyprus tax resident company is desired.

Appointment of Nominee directors

Nominee directors, non-professionals, appearing in hundreds of companies should NEVER be used. If such type of directors is used it is a clear indication that such directors do not think and decide the affairs of the company but simply "rubber stamp" the decisions directed to them by the shareholders or other advisors.

Appointment of directors residing outside Cyprus

The appointment of directors residing outside Cyprus, although possible, must be avoided if a tax resident Cyprus company is desired. In case it is impossible to avoid such appointment, then the law of the country of residence of the foreign director to be appointed, must be very carefully examined to avoid adverse tax possible effects.

There are countries which apply the management and control test in a similar manner that Cyprus does, i.e., UK, and in implementing this test, they might consider that, if a foreign company (Cyprus) is managed by a director who resides in their jurisdiction, becomes their tax resident and impose or claim taxation from the company concerned.

The fact that as from 01.01.2023 such a Cyprus company, from Cyprus law perspective, will be considered tax resident of Cyprus unless it is tax resident in another country, does not save the situation. The foreign country might claim that the company is tax resident in its jurisdiction and impose taxation, despite the implication of the Cyprus law.

In such a case we may have dual residency issues which will be explained further below under chapter, VI. Double Tax Treaties – Their impact on the residency issue of Cyprus Companies.

Appointing directors residing in countries in which the management and control test for foreign companies is applicable, such as the UK as explained above, must be avoided. There are considerable risks which need not be taken.

In effect, it is not advisable to appoint as directors in Cyprus tax resident companies, persons residing in countries that will be in a position to claim the tax residency of the company, such as UK, or other tax treaty countries, since there is a risk to be considered that a company intended to be Cyprus tax resident company, might be considered as managed and controlled in the foreign jurisdiction with serious adverse tax and legal consequences.

Delegation of powers

No key, strategic decisions should be made other than by a formal meeting of the directors.

Where discretionary powers have been delegated to any person (including a director), that power should only relate to day-to-day affairs and should not include the power to make key strategic decisions.

Parent/holding Company directing the decisions of its Cyprus subsidiary

There is a risk that a parent/holding company, residing outside Cyprus, may exert significant influence over a Cyprus subsidiary. The exercise of powers available to a shareholder in general meetings (appointments to the board, changes to financial structure etc.) do not on their own affect the residence of the subsidiary. It is, however, important to avoid the parent/holding being deemed to have usurped the functions of the subsidiary board, and thereby to exercise central management and control over the subsidiary's business.

The degree of autonomy of the subsidiary board is important in conducting the business of the company, including the extent to which the directors take decisions on their own authority as to investments, production, marketing and procurement, without reference to the parent/holding. It is the management and control of the subsidiary's business, rather than the location of shareholder control, that determines residence.

Relevant is the case discussed already Bullock v Unit Construction Co Ltd (1959) 38 TC 712 and the cases to be discussed further below, Laerstate BV v HMRC [2009] UKFTT 209, and HMRC v Development Securities plc and others [2020] EWCA Civ 1705.

Important note

A lot of Cyprus tax resident companies have as their holding companies, companies registered in UK. In such a case, extra attention must be paid as if the holding company with its board of directors residing in UK, controls and directs the business of the Cyprus subsidiary, then the Cyprus subsidiary might be considered from UK tax law perspective, as tax resident of UK and relevant taxation to be imposed on its income.

Advisers / consultants

Similar questions of influence can arise in relation to advisers/consultants, or other officers of the company giving instructions to directors residing overseas.

In the tax case Calcutta Jute Mills v Nicholson (1876) 1 TC 83, the director of the company, although residing in Calcutta, India, was receiving instructions from the company's office in London. This fact was sufficient for the court to consider that the company was a tax resident of UK instead of India and then taxable in UK.

The case, Wood v Holden, 2005 BTC 253 - High Court 18.4.2005, the facts of which are analysed further below, clearly directs to the avoidance of such appointments.

Similar considerations apply to the presence of observers or other non-directors at board meetings. Inviting a particular person to present to the board on a particular subject on an ad hoc basis does not present concerns. However, where an individual is a regular attendee of meetings covering a range of subjects, Income Tax may argue that he is in fact taking part in central management and control and, if that person is based in any foreign country, this may point to decisions being taken outside Cyprus with possible risks.

Rubber-stamping Decisions

In all cases where proposals, suggestions or other advice is being submitted to the company's board by a person or entity who is resident or otherwise present abroad, the directors should examine them critically and adhere to a proper decision-making process. It is important that the board meeting at which such proposals etc. are considered cannot be seen as a sham or as merely "rubber stamping" decisions which have been taken not in Cyprus. The independence and expertise of the board, together with the manner of communication between the parties, is crucial here.

Appointment of directors residing in the place where the income of the company is generated

It is also advisable to avoid appointing directors who reside in the country where the income of the Cyprus tax resident company is expected to arise or in which country tax issues might be raised as to the taxation of the Cyprus company or as to the taxation of its beneficial shareholder.

If for example, the activities of the company are in Russia and the income is generated in or from Russia, it seems not proper to appoint as directors of the Cyprus tax resident company, persons residing, living and working in Russia.

In case of such appointments, one leaves room for arguments, that the company or its real beneficial shareholder are taxable in Russia as the effective management of the company is situated in Russia.

Also, an argument can be put forward that the company is not tax resident of Cyprus as its management and control might be alleged not to be exercised in Cyprus.

Again, in such cases, there is possibility for dual residency issues as discussed in chapter VI. Double Tax Treaties – Their impact on the residency issue of Cyprus Companies of this brochure.

We would like to clarify though, that the crucial issue is not the nationality of the director but his / her residency. Where he / she permanently resides. A foreign national permanently residing in Cyprus, being a tax resident of Cyprus, will be suitable director.

Issuing of general powers of attorney

General powers of attorney should never be granted to non – residents or otherwise. If a general power of attorney is issued, there is real risk the management and control of the business to be considered that is exercised in the country of residence of the attorney. Specific, (and not broad) powers of attorney, may be granted to non-resident-based persons.

The issuing of general powers of attorney to persons who are not directors and granting them full authority and power to decide on fundamental matters and operations of the company, such as to sign contracts, to have unlimited investment powers and to generally deal in blank with all the affairs of the company, may be considered as abdication of authority and a serious reason to consider that the management and control of the company is entrusted and passed to the attorneys.

In such a case, there is a high risk of the company being considered to be resident at the place of the residency of the attorney and not in Cyprus.

General powers of attorney giving unlimited and wide authorities to the attorneys, as a rule, must be avoided. The company can perfectly do its business by issuing special resolutions or special powers of attorney for the execution of particular acts. Such a step does not affect the management and control test. On the contrary it strengthens it.

Appointment of directors residing in Cyprus, in foreign / overseas companies

The same factors that will strengthen a Cyprus company to be considered as managed and controlled in Cyprus, will be considered whether a foreign / overseas registered company is managed and controlled form Cyprus.

In this respect, it is not advisable to appoint directors residing in Cyprus as directors in companies registered in tax haven countries like BVI, Panama, Bahamas, Nevis, etc. In such a case, there may be a real risk that these companies may be considered to be managed and controlled in Cyprus, and consequently taxable in Cyprus, as a consequence of the applicability of the management and control principle. The same argument applies for UK based directors in such companies and should be avoided.

If such a claim is put forward by the Inland Revenue, BVI, Panama, Bahamas, Nevis, etc., companies, in order to avoid taxation, will need to prove that the Cypriot or UK director acts only on instructions of the real owners or other advisors situated abroad transferring the management and control abroad, there where the shareholders or other advisors, reside.

In effect, the director who follows blindly the instructions of the shareholders, or other advisors, is a mere cipher, simply stamping documents and doing what he is told. Relevant evidence and confidential information will need to be disclosed to the Inland Revenue to prove the director's symbolic status.

There is no need though to be engaged in such complications since the possibility can easily be avoided with the appointment of directors not residing in a country which applies the management and control principle.

In conclusion, as to the factors which will support the argument that the management and control is exercised in Cyprus in order to have a tax resident company, the directors must meet, manage and control the affairs of the company in Cyprus, proper board meetings with minutes must be taken place in Cyprus, all or at least the majority of the directors to be permanent residents of Cyprus and the positive surrounding factual circumstances to be present in Cyprus and avoid the negative surrounding factual circumstances as explained above.

Any appointments in a Cyprus company of directors not residents of Cyprus, raise serious risks as the company might be considered as tax resident in another jurisdiction with adverse tax consequences. The provision of the law that such company without being officially tax resident in another jurisdiction, as from 01.01.2023 will be considered as tax resident of Cyprus, does not save the situation. The foreign jurisdiction where the directors reside and decide, might claim the residency for such company and claim to impose taxation for its activities.

D. How the management and control must be exercised in order for a company to be considered as a tax resident of Cyprus?

This is the most crucial and most important criterion in order for a company to be considered as tax resident of Cyprus.

Real exercise of management and control by the board of directors

A long line of court judgements has established that the board of directors, who meet in execution of their duties and powers, must in fact exercise management and control over the company's affairs.

The directors must apply their mind and decide at their own discretion, on all the company's issues and express their free opinion on the parameters which govern the activities and operations of the company.

In effect, the management decisions must be taken by the board of directors who, independently, without any external influence, think and decide on all policy matters, strategies, financing, declaring of dividends, marketing and all other relevant matters and execute all their functions as members of the board, acting in the best interests of the company. This policy making is the primary expression of management and control.

The directors must reach their decision NOT by simply following the instructions of the shareholders or of any third person such as the consultants, lawyers', accountants or other advisors of the shareholders or the board of directors. They must think and decide at their own discretion for each case that arrives or put forward for consideration and implement the company's policy in an autonomous way.

If they simply act on instructions received from third persons or the shareholders or lawyers or accountants or other consultants acting on behalf of the shareholders, they are mere ciphers simply stamping documents and doing as they are told. This is not management and control but secretarial execution of orders.

The board of directors will of course consider the suggestions put forward by the advisors or the shareholders, but in each case, they must only consider these suggestions and proceed to decide applying their thinking only having in mind the interests of the business of the company. They must be ready to refuse adopting decisions not to the benefit to the company's interest and be ready even to resign if their decision is not followed.

Autonomous status of the board

In effect, the board must act autonomously and be in the position to reject requests which it considers not to be in the interests of the company or contrary to local law.

Knowledge of the business of the company

The directors must know the business of the company and genuinely determine its affairs, acting from Cyprus. If they simply obey the instructions of the beneficial owner or his advisors who reside in another jurisdiction, the central management and control, and therefore the residency of the company for the purpose of its tax liabilities will be the location/residence of the ultimate beneficial owner or the advisor or as the case may be.

Directors' remuneration

The directors must be properly paid for the work and meetings they have in such manner that demonstrates that this fee is sufficient to allow them to spend time to get to know the business of the company. Nominee directors with nominee fee, should NEVER be used.

Consultants' involvement in the affairs of the Company

The various advisors and shareholders who would like a particular company to be a tax resident of Cyprus, must be very careful in the way they draft their requests to the directors. They must avoid phrases as "I instruct you to do this" or "I order you to do that" or similar phrases.

The proper wording would be that they request the board to consider the particular matter and if accepted by the board to be within the interest of the company, then to implement it.

Not only the old court decisions mentioned above but also very recent ones support the above principles9.

We shall examine in more depth three court cases as they play an important role in the development of the principle of central management and control and represent its current version.

1. Wood v Holden, 2005 BTC 253 - High Court 18.4.2005

A case where consultants (PWC) resident in UK were advising directors of a Dutch company resident in holland

In this case, the Special Commissioners in the UK found that a Dutch resident company, paying taxes in Holland and acting through its board of directors in Holland, was also resident and taxable in the UK.

Park J, rejected the above approach on the facts of the case but not on the principles put forward by the Special Commissioners, something which is highly important to have in mind. The Court in this case reaffirmed the above principles as to the management and control.

On the facts, the judge accepted that PWC, acting from UK, never directed the directors to do anything and were not in position to do so. PWC gave them only advice and asked that the directors consider the offer, subject matter of the case, and further decide whether they will accept it or not.

The court accepted that the directors applied their mind and decided whether the offer was within the interest of the company and so were not merely going through the motions and simply stamping and signing documents.

It was clear that, if the directors just mindlessly followed the advice of PWC, the taxation imposed in the UK on the Dutch company would have been upheld due to the PWC and shareholders' intervention, both residing in the UK.

As Park J mentioned in this case, "if directors of an overseas subsidiary sign documents mindlessly, without even thinking what the documents are it would be difficult to argue that the subsidiary was tax resident where the directors met. But if they apply their minds to whether or not to sign the documents, the authorities... indicate that is a very different matter".

The above court case on 26/01/2006 has been upheld by the court of Appeal [Wood v Holden (HM Inspector of Taxes) 2006 BTC 208]

What Wood v Holden established is that once the board of directors applied their mind on the relevant issue that was sufficient no to disturb the place of central management and control. They followed a formalistic approach.

2. Laerstate BV v HMRC [2009] UKFTT 209

A case where a parent UK company was instructing the board of directors of its subsidiary.

In this case, the First Tier Tribunal held that a company's residency cannot be established merely on the basis of the location of board meetings as decided in Wood v Holden.

In this case the First-tier Tax Tribunal found that a company incorporated in the Netherlands was centrally managed and controlled by its sole shareholder, and sometime director, in the UK. The existence of a dominant shareholder does not of itself determine the residence status of a company; it is still necessary to establish who exercises central management and control of the company and from where.

Central management and control requires to look beyond the board meetings and board resolutions and requires wider examination of company's 'course of business and trading'. The board of directors would need to really exercise management and control and would need certain minimum amount of information to make decisions.

As said:

"We do not consider that the mere physical acts of signing resolutions or documents suffice for actual management ... What is needed is an effective decision as to whether or not the resolution should be passed and the documents signed or executed and such decisions require some minimum level of information. The decisions must at least be informed decisions. Merely going through the motions of passing or making resolutions and signing documents does not suffice."

The court also went on to state that "there is nothing to prevent a majority shareholder indicating how the directors of the company should act. If they consider the wishes and act on them it is still their decision." The question is whether the directors have the absolute minimum amount of information that a person would need in order to be able to make a decision at all on whether to agree to the shareholder's wishes or to decide not to sign the documentation. In this case, that would have included information or advice on whether the price was sensible. There was no such information or advice given to the director.

As a consequence of the key decisions having been taken in the UK, Laerstate was held to be UK resident under domestic law.

it is not enough just to have the formal acts of a company documented as occurring outside the UK in order to maintain that it is not UK tax resident. It is essential that the directors are kept informed so that they can properly make their decisions (whether they accede to the shareholder's wishes or not).

Sufficient knowledge of the affairs of the company plays an important role in reaching an independent decision.

Laerstate BV v HMRC abandoned the formalistic approach followed in Wood v Holden and followed a substantial approach as to how the board of directors must act in reaching the decisions in issue.

3. HMRC v Development Securities plc and others [2020] EWCA Civ 1705

A case where the UK parent company was directing the acts of the board of directors of the subsidiary

This case considered whether certain wholly-owned Jersey-incorporated subsidiaries of a UK property development and investment group were resident in the UK for corporation tax purposes. The Court of Appeal (CA) has overturned the decision of the Upper Tribunal (UT) and restored the decision of the First-tier Tribunal (FTT) that the Jersey-incorporated companies were centrally managed and controlled (and therefore tax resident) in the UK at the material times.

They were acting under instructions from the UK, and were thus UK resident.

In Wood v Holden in 2006 it was held that mere influencing of the decision of the directors by a third party (e.g.: a parent or third-party adviser) does not necessarily lead to a conclusion that the central management and control is removed from the non-UK company's directors.

In this case, it has now been held that the UK parent could be taken to effectively take the decision for the non-UK company by giving instructions to proceed with the specific transactions notwithstanding that the non-UK's director considered (or satisfied themselves of) the legality of the relevant transactions but did not give any decision to the merits of the transactions. This led to the conclusion that the central management and control was conducted by the parent and therefore in the UK and not in Jersey where the subsidiaries were incorporated.

This shows that there may be a high bar in future to establish that central management and control is exercised outside the UK in case of a UK parent company in place.

The Court of Appeal's decision also serves as a timely reminder that resident directors cannot provide a purely "administrative" service for the benefit of the parent owner but each director carries all the duties and responsibilities of a director generally, and as such, must ensure that they have sufficient knowledge and understanding of the business of the company and individually decide on all company matters.

This case has shown that,

- decisions by subsidiaries should be taken at proper board meetings and that,

- such board meetings properly consider the merits of any decisions to be taken as well as the legality of those steps. Particular care should be taken that, in implementing proposals given by a parent company, directors do not treat such proposals as instructions and that they consider carefully the commercial context for the decision.

In Wood v Holden a formalistic approach was adopted as to what was constituting a proper decision taken by the board of directors of the subsidiary. It was enough that the directors applied their mind and decided whether the decision was within the interest of the company and lawful.

In HMRC v Development Securities plc a clear substantial approach was adopted, following in effect the approach of Laerstate BV v HMRC. The board of directors must substantially be involved in the taking of the decision, knowing the facts and the surrounding environment to reach such decision. The question is simple: Did they take the decision or this was directed to them?

In conclusion, in order to have a Cyprus tax resident company, the directors must always genuinely meet in Cyprus, apply their mind, think and decide on all fundamental issues and policy decisions of the company with regard to its best interest using their own experience, knowledge and judgement. They must be well informed of the business of the company and this information must be recorded and in discharging their duties must make informed decisions and keep proper minutes showing that the corporate formalities are met. They must never act on instructions of third persons, whoever these may be, by simply stamping resolutions sent to them. Following other root, might move the tax residency of the company in the place where the decision-making body is situated, outside Cyprus with adverse tax consequences.

VII. DOUBLE TAX TREATIES – THEIR IMPACT ON THE RESIDENCY ISSUE OF CYPRUS COMPANIES

Cyprus has signed a considerable number of Double Tax Treaties which regulate taxation on various matters between the contracting states.

In order for a company to take advantage of the provisions of the Double Tax Treaties, it must be resident of one of the two contracting states. In our case, the Cyprus company, must be resident of Cyprus for tax purposes.

A definition of what a "resident of a Contracting State" means, is given in article 4.1 of the Organisation for Economic Co-operation and Development - OECD, model treaty which provides the following:

"RESIDENT

For the purposes of this Convention, the term "resident of a Contracting State" means any person who, under the laws of that State, is liable to tax therein by reason of his domicile, residence, place of management or any other criterion of a similar nature, and also includes that State and any political subdivision or local authority thereof. This term, however, does not include any person who is liable to tax in that State in respect only of income from sources in that State or capital situated therein".

Further, according to the Commentary to the OECD Model Tax Convention:

"The place of effective management is the place where the key management and commercial decisions that are necessary for the conduct of the entity's business are in substance made. To determine the tax residency of a company, tax authorities would be expected to take into account various factors, including among others where the chief executive officer and other senior executives usually carry on their activities and where the senior day-to-day management of the person is carried on."

Place of effective management as per relevant article in Double Tax Treaties. Tie – breaker article

Article 4.3 of the OECD model treaty, provides the following:

Where by reason of the provisions of paragraph 4.1, cited above, a person other than an individual is a resident of both Contracting States then it shall be deemed to be a resident only of the State in which its place of effective management is situated.

The above crucial provision, known as the "tie – breaker" article, which provides the solution to a possible problem of dual residency, is included nearly in all treaties that Cyprus has signed.

Definitions of the terms in the Double Tax Treaties

There is no definition of the terms, place of management, effective management, head office, registered office, place of registration, headquarters, place of incorporation, or other similar criteria which are used in the Double Tax Treaties.

Applicability of local laws as to residency

The lack of any definition of the above terms used in respect of all legal bodies in the Double Tax Treaties, leads to the consideration of the Cyprus law in order to establish the residency of a Cyprus company, under such law, for tax purposes and consequently for treaty purposes as well.

In effect, the treaties point to the local laws of the contracting states, in order to identify, under which conditions a company registered in their jurisdiction, or not registered there, will be considered as their tax resident. Local tax law provisions will need to be examined in order for a company to be considered as tax resident under the provisions of the Double Tax Treaties.

In considering whether a Cyprus company is a tax resident of Cyprus, and consequently being benefited from the provisions of the Double Tax Treaties, the analysis provided in the previous chapters of this brochure as to the management and control test, applies.

Dual residency

There might be a situation where a company is a resident of more than one country. This might be the case when the management and control of the affairs of the company is not centred in one country but is divided or distributed among one, two or more countries.

Such situations might appear when the directors of the company, which form the highest level of management of the company, are resident in various countries and execute their management duties from their place of residence and not from Cyprus.

Also, such situations might appear when the advisors or the shareholders of the company reside in different countries than where the board meets and from their place of residence direct the decisions of the board.

If such factual situations exist, then the allegation and possibility of dual residency of a company can be raised by Inland Revenues with drastic tax effects. It is for this reason that we are of the opinion that if a Cyprus tax resident company is needed, the appointment of directors with effective management, residing outside Cyprus must be avoided, as dual residency issues may arise.

The above possibilities as to the dual residency of a company have been considered in many court cases10.

The above authorities clarify and confirm that there where there is a fragmentation of the central management and control of the business of the company exercised in effect from two or more countries, there can be dual residency for the company with further tax issues to be considered.

Allegation of dual residency by a treaty country

If dual residency exists or if such allegation is raised by any one of the treaty states, e.g., that a Cyprus company is also resident in that other state which claims taxation, then the solution is provided by the "tie – breaker" article of the Double Tax Treaties, article 4.3 discussed above.

According to article 4.3, if dual residency exists, the company is deemed to be resident where its effective management is exercised.

The answer to the question, where the effective management is exercised, identifies the tax residency of the company and in effect the country of its taxation.

As to the effective management test and its conditions, the analysis provided in the previous chapters of this brochure relating to the management and control test, apply accordingly.

In the court case, Wensleydale's Settlement Trustees v IRC [1996] STC (SCD) 241, a Special Commissioner considered that the place of effective management is there where the shots are called, implying realistic positive management. In effect, the analysis of the management and control test provided above applies for this issue too.

Case study

Suppose that the Russian or the UK tax authorities or the Inland Revenue of any other treaty country, allege that a tax resident Cyprus company, for matters of management, domicile or other similar issues, is also tax resident of Russia or UK or in that other country and not only in Cyprus. Because of this conclusion, they seek to impose taxation on the Cyprus tax resident company for a particular operation.

In case of such a dual residency problem, (Cyprus also alleges that the company is a tax resident of Cyprus liable to taxation in Cyprus) article 4.3 of the Double Taxation Treaty signed between Cyprus and Russia, and the relevant article of the UK treaty or as the case might be with the other treaty countries, applies and gives the solution.

This tie – breaker article, as being a provision of an international treaty, supersedes any local laws and directs that the residency of the company is deemed to be there where the effective management of the company is exercised. If the effective management is exercised in Cyprus, taxation cannot be imposed in Russia or in the UK or in the other contracting State by operation of the Double Taxation Treaty.

In view of this provision which provides a solution, special attention must be paid to what has been said above in order to establish and to secure that the management and control of the company's affairs is exercised in Cyprus. Similar arguments can be put forward in all other cases where Double Tax Treaties have been signed with the above provision in place.

The judgement in Wood v Holden mentioned above, handles also the issue as to the effective management test, due to the fact that a relevant provision is in the Double Taxation Treaty between UK and Holland and the case was decided on this principle. It was decided that the effective management was situated in Holland and not in the UK.

In more recent court cases though, it was decided that the effective management was situated in UK and not overseas where the companies were registered and the board of directors was situated. See, HMRC v Development Securities plc and others [2020] EWCA Civ 1705 and Laerstate BV v HMRC [2009] UKFTT 209 and Laerstate BV v HMRC [2009] UKFTT 209, discussed above.

VIII. CYPRUS INLAND REVENUE APPROACH

The Cyprus Inland Revenue has not yet issued any practice guidelines as to how it will deal with the management and control test, its interpretation and implementation.

1. Cyprus companies under investigation by Cyprus Inland Revenue

It is clear that the Cyprus Inland Revenue will not disturb on its own initiative a Cyprus company which has decided to get registered as tax resident of Cyprus. Such a company is taxable in Cyprus on its worldwide income and the Inland Revenue will not object to such a request for obvious reasons.

As a matter of practice, the Cyprus Inland Revenue in order to accept a company as a tax resident of Cyprus requests the directors to declare that they exercise the management and control of the company in Cyprus.

Once this declaration is signed and submitted to the Inland Revenue, then the company is accepted and registered as a tax resident of Cyprus liable to the Cyprus taxation. Relevant Tax residency certificate is issued by the Inland Revenue, if requested. In such a case though a relevant questionnaire is completed confirming that the management and control is exercised in / from Cyprus.

No other conditions at this early stage of registration of the company as tax resident are examined or demanded by the Cyprus Inland Revenue.

As from 01.01.2023 all Cyprus companies, except in the case they are tax residents in another country, will be considered as tax resident of Cyprus by virtue of their registration and the Inland Revenue approach will be amended accordingly.

2. Foreign registered Companies under investigation by Cyprus Inland Revenue

The Cyprus Inland Revenue, if a case arise, might claim that a foreign registered company is tax resident of Cyprus if its management and control is exercised in Cyprus.

The burden of establishing that a foreign company is Cyprus resident, and liable to tax by virtue of its Cyprus residency, lies with the Cyprus Inland Revenue authority.

In order for the Cyprus Inland Revenue to claim that a company is within the Cyprus tax net, they will need to argue that:

- The directors of that company exercise management and control in Cyprus; or

- Someone other than the appointed directors, such as consultants, shareholders, or third parties, acting in effect as shadow directors, exercise management and control from within Cyprus over the business of the company.

In these cases, the Cyprus Inland Revenue, is expected to follow the above steps in order to identify the place of central management and control of such companies, and if found to be in Cyprus, local taxation laws will apply.

Important note

A lot of Cyprus based service providers, for various foreign companies they manage, i.e., BVI, Bahamas, Belize, Seychelles, etc., for their convenience, appoint as directors Cyprus resident persons. This is very risky as the Inland Revenue may institute an investigation whether the particular foreign company is tax resident of Cyprus based on the management and control principle having in its board local resident Cypriot directors managing its affairs from Cyprus.

3. Cyprus companies under investigation by foreign Inland Revenue departments

Tax residency problems though, might arise for Cyprus tax resident companies in foreign jurisdictions.

A foreign country, if a Cyprus company is managed and controlled from its territory, might allege that it is tax resident in its jurisdiction, and may claim to impose taxation to it.

In such a case, in order to avoid and be able to defend such allegation, the above factors strengthening the tax residency of a Cyprus company as being in Cyprus must be met.

In case a Double Tax Treaty between Cyprus and the claiming of residency country is in place, the effective management rule, "tie-breaker" provision, pointing to Cyprus must be invoked to defend such allegation.

If there is no Double Tax Treaty in place, then the local laws of each country will be invoked to solve the issue.

IX. THE MANAGEMENT AND CONTROL TEST IN ONE PAGE

What has been discussed in this publication is summarized below in the following diagram:

X. CONCLUSION – FINAL SUMMARY

Cyprus or foreign companies anywhere registered, will be considered tax residents of Cyprus if:

- Their management and control is exercised in Cyprus11;

- The management and control is exercised in Cyprus, if the board of directors resides or at least the majority resides in Cyprus and genuinely holds board meetings in Cyprus having in mind all the positive and negative factors explained above;

- The directors, at the board meetings give genuine consideration as to the affairs and business of the company and decide its policy, structural and main issues without simply following the instructions of the owners or their advisors. The directors must apply their mind, think and decide autonomously on all issues of the company and in its best interests; Knowledge of the business of the company and the business factual situation is of paramount importance.

- Any instructions and decisions relating to the business, management matters of the company, must be generated and given solely by the board of directors.

- Dual residency issues might be raised in case of fragmentation of power, namely, the management and control of the company's business is exercised by the directors / shareholders / advisors, in various countries. In such a case, if there is a Double Tax Treaty in place, the effective management rule "tie-breaker" article applies and identifies the residency of the company. If there is not any Double Tax Treaty in place, local laws will apply and give the solution.

Footnotes

1. See further below under Taxation of Companies, what is provided as to the taxation of non-resident companies.

2. The law speaks of being tax resident in any other country. There is no condition that the taxation laws of that other country impose any taxation on the income earned. So, any jurisdiction, where the Cyprus company is tax resident, meets the requirement.

3. "Common Law" is the body of legal rules, based upon court decisions and not on statutory law made by a parliament, embodied in reports of decided cases, that has been administered by the common-law courts of England since the Middle Ages. Common laws vary depending on the jurisdiction, but in general, the ruling of a judge is often used as a basis for deciding future similar cases.

4. "Principles of Equity" are set of rules which rectify injustice done by the rigid application of court precedents and statutory law. It is the rectification of legal justice.

5. FA 1994 s.249.

6. The shadow director principle is also past of Cyprus company law as per section 192(9) of the Companies' law Cap.113.

7. De Beers Consolidated Mines Ltd v Howe [1906] AC 455, 5 TC 198. Calcutta Jute Mills Co Ltd v Nicholson and Cesena Sulphur Co Ltd v Nicholson (1876) LR 1 Exch D 428, which were heard and decided together by the Court of Exchequer; R v Dimsey (1999) STC 846; Trevor Smallwood Trust v HMRC [2010] EWCA Civ 778.

8. Calcutta Jute Mills Co v. Nicholson [1876] 1 TC 83; Cesena Sulphur Co Ltd v. Nicholson 1876 1 TC 88; De Beers Consolidated Mines Ltd v. Howe [1906] Ac 455, 5 TC 198; Bullock v. Unit Construction Co Ltd [1959] 38 TC 712.

9. Re Little Olympian Each Ways Ltd [ 1994] 4 All ER 561; Untelrab Ltd v McGregor [1996] STC (SCD) 1; R v Crown Court at Kingston [2001] STC 1615; Esquire Nominees Ltd v Commissioner of Taxation [1971] 129 CLR 177; New Zealand Forest Products NV v Commissioner of Inland Revenue [1995] 17 NZTC 12,073}; Wood v Holden, 2005 BTC 253 - High Court 18.4.2005; Laerstate BV v HMRC [2009] UKFTT 209; and, HMRC v Development Securities plc and others [2020] EWCA Civ 1705.

10. Swedish Central Rly Co Ltd v. Thomson [1925] 9 TC 342; Union Corp Ltd v IRC [1952] 34 TC 207; Koitaki Para Rubber Estates Ltd v Federal Comr of Taxation [1940] 64 CLR 15; R v Holdon, High Court 18.4.2005.

11. It is clarified that for Cyprus law perspective as from 01.01.2023 all Cyprus registered companies are considered as tax residents of Cyprus, unless their management and control is exercised abroad AND they have been registered as tax residents in any foreign jurisdiction.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.