In the past two years, reverse vesting orders ("RVOs") have gone from obscurity to being the tool of choice in many complex restructurings under the Companies' Creditors Arrangement Act (the "CCAA"). As restructuring practitioners increasingly employ RVOs, it begs the question: Will RVOs replace traditional CCAA plans?

- RVOs transfer unwanted assets and liabilities out of a debtor company, leaving behind only the assets and liabilities that a purchaser wants to acquire.

- RVOs can achieve a similar outcome to a plan of compromise or arrangement, but with less cost, time, and fewer steps.

- Two lower court decisions (leave to appeal dismissed) have addressed contested reverse vesting transactions and confirmed that RVOs are permissible under the CCAA, but the extent to which RVOs may be used is still unclear.

Reverse Vesting Orders as a Third Restructuring Tool

In a traditional corporate restructuring under the CCAA, debtor companies typically follow one of two paths:

- Plan of compromise or arrangement, which allow debtors to emerge as "new and improved" restructured companies while retaining possession of their assets, agreements, employees, permits, licences, tax attributes, etc. Plans can be complex and time-consuming to implement: they require a claims process, a creditors' meeting, "double majority" approval by eligible creditors, and court approval, amongst other requirements.

- Liquidation, which involves the sale of debtor companies as going concerns (as opposed to outright liquidations), or the sale of some or all of the assets of debtor companies to one or more purchasers. Sale transactions are typically structured as asset purchase agreements. Purchasers can individually select which assets and liabilities they want to acquire/assume, while excluding unwanted assets and liabilities. Purchased assets and liabilities are transferred to and vested in the purchaser free and clear of pre-existing liabilities (other than assumed liabilities) by means of a court-issued approval and vesting order ("AVO"). AVOs do not require a plan or creditor approval.

RVOs have emerged as a new third option for debtor companies. RVOs combine the benefits of both a plan and an AVO, but without imposing the same costs, time considerations and requirements of a plan or the limitations of an AVO.

What is an RVO?

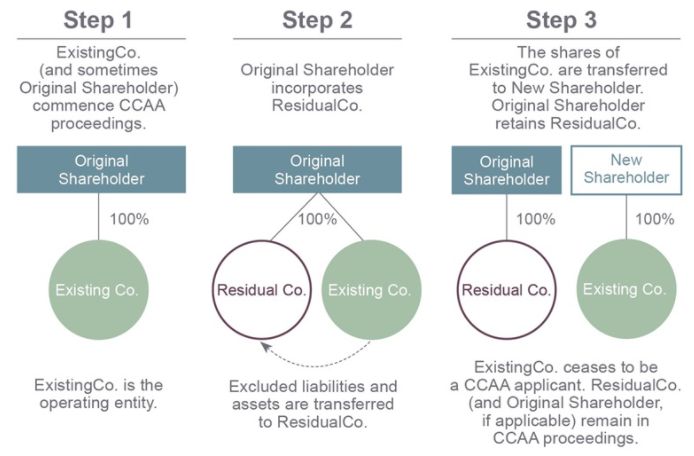

An RVO is a court order that transfers unwanted assets and liabilities out of a debtor company ("ExistingCo") to an affiliated (often, newly incorporated) company ("ResidualCo"). ExistingCo is left holding only the assets and liabilities that the purchaser wants to acquire. The purchaser can then acquire the shares of ExistingCo, and ExistingCo can exit CCAA proceedings. ResidualCo remains in the CCAA proceeding after ExistingCo exits, at which point ResidualCo typically makes an assignment in bankruptcy.

An RVO should be contrasted with an AVO. Whereas an AVO transfers wanted assets and liabilities out of the debtor company and to the purchaser, an RVO transfers unwanted assets and liabilities out of the debtor company. Similar to an AVO, and unlike a plan, RVOs do not require a creditor meeting or vote.

The following chart outlines a straightforward RVO transaction, which typically happens in three steps:

Why Use an RVO?

RVOs have many desirable characteristics, including the following:

- Preserve existing rights: ExistingCo continues to exist as a going concern, which preserves ExistingCo's rights such as permits, licences, agreements, and tax attributes.

- Reduce/eliminate ongoing obligations: Unwanted assets and liabilities can be identified and dropped from ExistingCo. Identifying unwanted assets and liabilities can sometimes be easier than identifying wanted assets and liabilities.

- Only available option: Certain assets, such as cannabis licences, mining licences, and tax attributes, cannot (or cannot easily) be transferred to purchasers by means of an AVO. An RVO bypasses such issues because wanted assets and liabilities remain with ExistingCo.

- Quick and economical: RVOs can achieve a similar result to a CCAA plan (including granting releases to directors and officers), but without the time, cost and steps of a traditional plan.

It is likely that as RVOs expand in usage, more advantages and use-cases will emerge.

When Have RVOs Been Used?

RVO transactions date back to at least 2000, when an RVO transaction was employed in the restructuring of T. Eaton Co. The next recorded use of an RVO transaction was in the 2015 restructuring of Plasco Energy Group Inc. et al. (Re). It took until late 2019, however, for RVO transactions to really take-off. From October 2019 to June 2021, at least sixteen RVO transactions were approved by Canadian courts.1

Almost all RVOs have been employed where the debtor company had assets that could not (or could not easily) be transferred to a purchaser as part of an AVO. These assets have included cannabis licences, mining licences or permits, and favourable tax attributes. Another common feature of RVO transactions is that the RVO transaction is typically the only option available to the debtor company, other than bankruptcy (e.g. there is only one prospective purchaser following a sales process, and that purchaser insists on an RVO).

Most RVO transactions have been unopposed. The first contested RVO transaction occurred in October 2020 in Nemaska Lithium Inc. (Re).2 In this case, Justice Gouin of the Superior Court of Quebec dismissed a creditor's opposition to the proposed RVO transaction and approved the RVO, writing that the CCAA does not restrict the use of RVOs and that the Court has the general discretion to issue any order that it considers appropriate pursuant to s. 11 of the CCAA. Justice Gouin found that the proposed RVO transaction was efficient and rapid, and noted that there were no attractive alternatives to the RVO transaction. The Court of Appeal of Quebec dismissed the objecting creditor's application for leave to appeal,3 as did the Supreme Court of Canada.4

Interestingly, RVOs are expanding beyond CCAA proceedings. In recent months, an RVO was granted in a proposal proceeding pursuant to the Bankruptcy and Insolvency Act,5 and another RVO was granted in a receivership.6

Could RVO Transactions Replace CCAA Plans?3

RVO transactions can be quicker, cheaper, and easier to implement than CCAA plans. Given these benefits, it is not surprising that RVO transactions have already started replacing traditional plans.

In Quest University Canada (Re),7 the debtor originally anticipated using a plan to sell its assets. One creditor, who effectively had a veto right, opposed the asset sale and was unlikely to vote in favour of the plan. The debtor, in turn, reformulated the sale as an RVO transaction. By using an RVO instead of a plan, the debtor could still transfer certain hard-to-transfer assets (like its university degree-granting authority) while simultaneously reducing opportunities for the opposing creditor to object. Justice Fitzpatrick of the Supreme Court of British Columbia granted the RVO, stating that "[t]here is no provision in the CCAA that prohibits an RVO structure",8 and stressing that there were "unique and exceptional circumstances"9 in this case that warranted an RVO, such as the non-transferability of certain assets and the lack of attractive alternatives. The Court of Appeal for British Columbia dismissed an application for leave to appeal by the creditor.10

The debtors in both Beleave Inc. et al. (Re) and Green Relief Inc. (Re) also replaced anticipated plans with RVO transactions. In Beleave Inc. et al. (Re), the debtors switched to an RVO transaction because their illiquidity meant that they could not fund the procedural steps required to implement a plan.11 In Green Relief Inc. (Re), the debtor switched to an RVO to, among other things, reduce its use of interim financing, minimize professional fees, and save time.12 Both cases involved the transfer of cannabis licences.

Whether there are any limitations on when RVOs can be employed (and when they can replace traditional plans) has yet to be explored in-depth by any level of court. Most RVO cases share similar facts: Nemaska Lithium Inc. (Re), Quest University Canada (Re), Beleave Inc. et al. (Re) and Green Relief Inc. (Re), for example, all involved hard-to-transfer assets and no attractive alternatives to an RVO. This makes it unclear whether RVOs can be employed in different circumstances, such as those more common to simple CCAA plans.

TakeawayThe growth of RVO transactions in the last two years

exemplifies the ongoing ability of the CCAA and the courts to

accommodate new and innovative transactions. In the coming years,

it is likely that RVOs will continue to expand and possibly be used

in novel circumstances. Close attention should be paid to whether

this expansion results in a corresponding reduction in the number

of traditional CCAA plans and the creation of limitations or

conditions on when RVOs can be employed.

Footnotes

1 RVOs were granted in the following proceedings: Stornoway Diamond Corp. et al. (Re); Wayland Group Corp. et al. (Re); Comark Holdings Inc. et al. (Re); Beleave Inc. et al. (Re); Nemaska Lithium Inc. et al. (Re); JMB Crushing Systems Inc. et al. (Re); Redrock Camps Inc. et al. (Re);Cirque du soleil Canada inc. et al. (Re); Green Relief Inc. (Re); Tidal Health Solutions Ltd. (Re) [note: this was a proposal proceeding under the Bankruptcy and Insolvency Act]; Quest University Canada (Re); Tribalscale Inc. (Re); JMX Contracting Inc. et al. (Re); FIGR Brands, Inc. et al. (Re); Salt Bush Energy Ltd. et al. (Re); and Vert Infrastructure Ltd. (Re) [note: this was a receivership proceeding under the Bankruptcy and Insolvency Act and Courts of Justice Act (Ontario)].

2 2020 QCCS 3218.

3 Arrangement relatif à Nemaska Lithium inc., 2020 QCCA 1488; Cantore c Nemaska Lithium Inc., 2020 QCCA 1333.

4 Brian Shenker v Nemaska Lithium Inc., et al., 2021 CanLII 35003 (SCC); Victor Cantore v Nemaska Lithium Inc. et al., 2021 CanLII 34999 (SCC).

5 Tidal Health Solutions Ltd. (Re) (20 November 2020), Montreal 500-11-058600-202 (Que Sup Ct [Commercial Division]), Approval and Vesting Order.

6 Vert Infrastructure Ltd. (Re) (8 June 2021), Toronto CV-20-00642256-00CL (Ont Sup Ct [Commercial List]), Approval and Vesting Order.

7 2020 BCSC 1883.

8 Ibid at para 157.

9 Ibid at paras 168, 172 and 180.

10 Southern Star Developments Ltd. v Quest University Canada, 2020 BCCA 364.

11 Beleave Inc. et al (Re) (17 September 2020), Toronto CV-20-00642097-00CL (Ont Sup Ct [Commercial List]), Fourth Report of the Monitor at paras 13 and 14.

12 Green Relief Inc. (Re) (16 September 2020), Toronto CV-20-00639217-00CL (Ont Sup Ct [Commercial List]), Factum of Green Relief Inc. at para 44.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.