- within Transport topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Accounting & Consultancy and Healthcare industries

Key takeaways

- In 2025, Canadian AI funding increased while overall PE and VC deal activity fell, reflecting a trend towards larger financings.

- Most AI capital in 2025 concentrated on larger rounds, creating a funding gap for proven companies seeking to scale.

- Investors face opportunities in growth capital for mid-tier AI scale-ups, buyouts in AI-enabled vertical software and infrastructure investments.

Artificial intelligence has quickly become one of Canada's most important technology export stories, and private capital is playing a key role in shaping how the story unfolds. No longer viewed as a specialized software niche, AI is increasingly underwritten as foundational infrastructure — akin to energy or telecommunications.

This industrial transformation has been driven, in part, by the rise of agentic AI systems — autonomous actors capable of executing complex enterprise workflows. These systems are fundamentally reshaping both technology companies and the organizations that have found ways to deploy these capabilities to drive value. With capital increasingly gravitating towards businesses poised to scale these agentic functions, the market effect appears to be a sharp capital concentration where investors are directing capital toward a select tier of AI champions positioned to anchor this emerging industrial ecosystem.

At the same time, domestic VC fundraising decreased to decade lows in 2025 and the federal government is mobilizing billions in infrastructure capital to address compute capacity gaps. These dynamics reveal distinct opportunities for private equity investors willing to deploy large‑scale capital into the right segments of the market.

Market momentum: AI deal activity in Canada

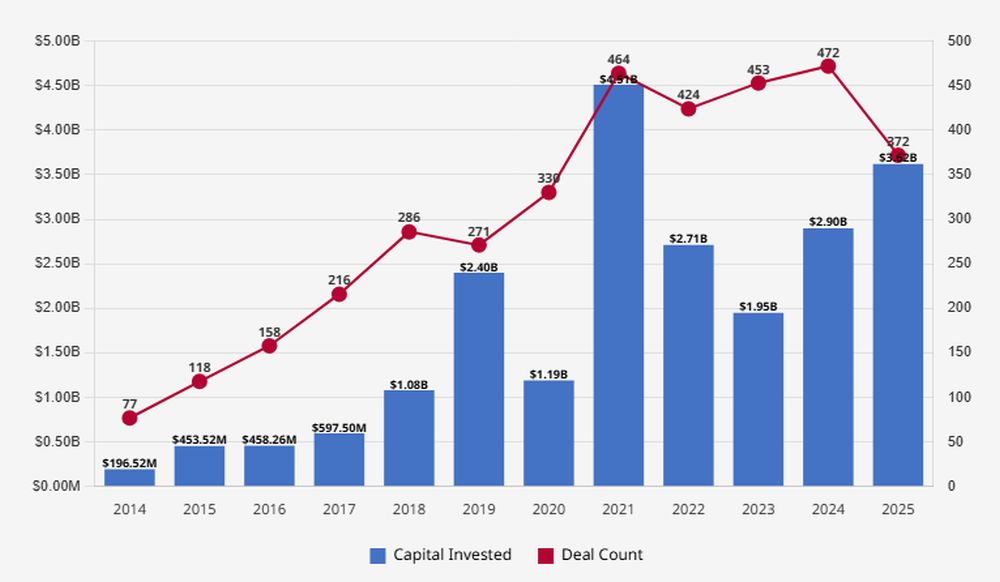

Capital deployed into Canadian AI firms surged in 2025 to the highest levels since 2021, according to data sourced from PitchBook.1 Yet that capital flowed into fewer companies: overall PE and VC deal activity fell in 2025 to the lowest levels since 2020, reflecting a more disciplined, high-conviction investment cycle.2

The composition of PE and VC deal activity also noticeably shifted in 2025: buyouts, add-ons, PIPEs, growth/expansion rounds and later-stage VC rounds all increased or remained on par with 2024 levels, while seed, early-stage VC and pre-accelerator/incubator rounds all declined.3 This divide suggests that investors may be selectively targeting established, revenue-generating AI firms with solid profit prospects, perhaps opening doors for PE sponsors to invest in areas where traditional VC interest has cooled.

Capital concentration and the emerging funding gap

In 2025, 84% of VC funding into Canadian AI companies flowed to larger rounds of US$25 million or more, up from 77% in 2024, while rounds between US$10 million and US$24.9 million declined 27% year‑over‑year.4 This capital concentration is creating a funding gap, particularly for companies that have proven product‑market fit but need institutional capital to scale.

From 2022 through 2025, the 10 most-funded Canadian AI companies pulled in around US$5.5 billion — roughly 40% of all capital invested in Canadian AI during the period.5 This reflects a clear "winner-take-most" trend, with private capital gravitating toward a handful of rising leaders. This concentration underscores a structural reality: building serious AI is both expensive and hard, making scale a critical factor for success. Frontier model development, specialized talent, proprietary data advantages and the massive compute requirements of modern AI all create significant barriers to entry. These challenges, in turn, reinforce competitive advantages for companies that have already achieved such scale and defensible market positions — and increasingly, these are companies building or deploying agentic capabilities.

This concentration is playing out in real time. Since August 2025, Osler has advised on three of the most significant AI transactions in Canadian history: Cohere's US$500-million financing at a US$6.8-billion valuation, Waabi's record $750-million Series C rounding out $1 billion in total funding and Clio's $1-billion acquisition of vLex alongside a $500-million Series G at a $5-billion valuation. These historic deals, all occurring within months of each other, exemplify how institutional capital is increasingly being funnelled toward established AI leaders, even as overall deal activity in the sector contracts. For private equity investors, the concentration reveals distinct opportunities that are accompanied by associated complexities.

Growth capital for mid-tier scale-ups

The shift toward mega-round funding leaves a cohort of proven AI scale‑ups — companies with credible products, paying customers and clear market positions — stuck between early-stage venture and hypergrowth. With traditional VC pulling back (Canadian VC firms raised just C$2.1 billion in 2025, the lowest since 2016), growth-oriented PE investors are well positioned to bridge this gap, playing a larger role in providing the scaling capital these businesses need.6 However, success in this space hinges on navigating highly competitive markets with unpredictable outcomes, meaning sponsors might need to embrace more venture-like risk in pursuit of higher returns.

Investors entering at this stage should recalibrate traditional technology diligence assumptions to reflect heightened risk profile as compared to diligence they would otherwise conduct for more mature acquisitions. In AI scale-ups, competitive advantage can sometimes erode quickly, particularly where differentiation depends on access to data that competitors can replicate or purchase. Reliance on foundation model providers introduces platform dependency risk, and as large language models and foundational models improve, they may replicate or subsume application-layer capabilities that once differentiated smaller AI companies. In addition, model performance can shift, foundational model dependencies can evolve, and data rights can be contractually constrained. These factors introduce greater volatility, underscoring why this segment behaves more like late-stage venture than traditional growth equity.

Buyouts and add-ons in AI-enabled vertical software

While capital concentration pushes mega-rounds toward a small group of AI champions, the doubling of buyout and add‑on activity from 2024 to 2025 suggests sponsors are finding opportunity outside the winner-take-most dynamic.7 Global PE trends point to vertical software with embedded AI as an attractive segment: businesses with predictable cash flows where AI enhances margins rather than defines the product.8 Record-level Canadian AI buyout deal volume in 2025 and broader software M&A momentum suggest potential for disciplined buyers targeting defensible, profitable assets in sectors where AI can be leveraged for operational improvement.9

In these transactions, particularly those involving a vertical integration strategy, diligence should focus not only on operational alignment, but on whether data rights and model architecture support scalable reuse. Sponsors must assess whether data acquired in a target business can be legally used beyond that business, whether due to limits imposed by customer contracts, privacy laws or other sector-specific regulation. Similarly, model performance achieved within a specific domain of a target company may also not translate seamlessly across adjacent verticals. This is a common issue in buy-and-build strategies, which can materially limit expected integration benefits. Where these assumptions are not carefully assessed, the anticipated value of the acquisition may not be fully realized.

Infrastructure investment in data centres and compute

For sponsors looking to sidestep single‑company risk, the infrastructure layer that underpins the entire AI ecosystem may offer an alternative risk profile. Data centre infrastructure is particularly compelling in this context. Canada's natural advantages — abundant renewable energy, cold climate for cooling efficiency, political stability and proximity to U.S. markets — position the country as an attractive location for AI-optimized data centre development. Unlike the more unpredictable fate of mid-tier growth firms or the risks tied to operational overhauls, data centre and compute capacity investments — or the "picks and shovels" of the industry — benefit from broad AI adoption regardless of which application‑layer players ultimately win their markets; every AI player depends on compute.

Infrastructure, however, carries other risks. Power and site availability remain fundamental constraints, as securing reliable grid connections, sufficient energy capacity and permitting can delay deployment or limit expansions. Hyperscaler concentration, where a few large tenants, like AWS, Microsoft Azure and Google Cloud account for most data center demand, creates counterparty exposure and bargaining asymmetry, particularly if build-to-suit commitments shift or fall short. The capital-intensive nature of state-of-the-art facilities and advancing AI hardware requirements create both construction risk and technology obsolescence risk, as data centres designed for one generation of chips and cooling infrastructure may soon fall behind newer standards. Rapid buildouts also raise the prospect of localized oversupply and underutilization if AI workload growth moderates more quickly than forecast. Environmental and resource pressures, including water use for cooling and community resistance to high energy consumption, add further operational complexity.

While infrastructure may, on one end, help an investor diversify single-company risks, the reality is that the overall risk profile is shifted, not eliminated. Outcomes remain highly sensitive to macroeconomic factors, such as interest rate fluctuations, inflationary pressures and broader economic cycles, which can materially influence project viability, financing costs and long-term returns.

Canada's AI strategy: infrastructure and scale-up support

The federal government has committed over $2 billion to sovereign AI compute, including $700 million through the AI Compute Challenge to co-invest in large-scale data centres alongside private sponsors, and an additional $925.6 million in Budget 2025.10 As part of this effort, the Canada Infrastructure Bank and the Major Projects Office are actively soliciting proposals for sovereign data centres over 100MW and streamlining federal approvals. For infrastructure investors, the strategy is designed to de-risk four key barriers: grid access, regulatory bottlenecks, long-term demand uncertainty and funding gaps.11

However, the "sovereign" designation introduces complex trade-offs that warrant scrutiny. Infrastructure investments demand careful navigation of a complex regulatory maze, including provincial electricity rules, federal environmental assessments, municipal zoning and growing data-residency and cybersecurity mandates tied to government anchor tenants. Sponsors must craft co-investment deals with government partners that clearly define governance, operational control and exit strategies — especially when public capital brings restrictions on foreign ownership, data management or future revenue generation.

While programs like the AI Compute Access Fund ($300 million) and SCALE AI offer some support to scale-ups, these initiatives are unlikely to adequately address the deeper scaling gap for the stranded cohort of Canadian AI companies that are starved for capital. Current government support strategy appears largely aimed at de-risking the infrastructure layer, not the application layer, which may partly explain why some investors are gravitating toward infrastructure plays over backing individual AI companies.

Looking ahead: from capital allocation to operational advantage

The concentration of capital into fewer but larger Canadian AI companies signals a maturing market where many institutional investors favour proven players with the scale to sustain AI's industrial transformation. For private equity sponsors, this shifting landscape has revealed potential investment pathways: growth capital for stranded scale-ups, M&A in AI-enabled vertical software, and infrastructure investments in compute capacity.

These opportunities all benefit from federal government recognition of AI as a national priority; however, each carries different risk profiles, return expectations and strategic considerations. The sponsors who recognize these distinctions, identify the right strategies and adapt their diligence frameworks accordingly will be better positioned than those who treat Canadian AI as a single asset class.

Footnotes

2. PitchBook.

3. PitchBook.

4. PitchBook.

5. PitchBook. The cited data has not been reviewed by PitchBook analysts and may be inconsistent with Pitchbook methodology.

6. "A perfect storm": 2025 was the worst year for Canadian VC fundraising since 2016," BetaKit, January 7, 2026.

7. PitchBook.

8. "Software M&A Dominates 2025 With 65% Market Share – M&A Alerts," The M&A Advisor, October 9, 2025.

9. "Software M&A Dominates 2025 With 65% Market Share – M&A Alerts," The M&A Advisor, October 9, 2025.

10. "Canada to drive billions in investments to build domestic AI compute capacity at home," Government of Canada, December 5, 2024.

11. "Canadian Sovereign AI Compute Strategy" and "Enabling large-scale sovereign AI data centres," Government of Canada.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.