- within Corporate/Commercial Law topic(s)

- in Canada

- with readers working within the Advertising & Public Relations, Banking & Credit and Business & Consumer Services industries

- within Employment and HR topic(s)

- with Senior Company Executives and HR

Despite factors that might have otherwise presented challenges for activists, shareholder activism in Canada proved resilient in 2025. The passing of a year marked by geopolitical and economic uncertainty – a trend which shows no signs of abating – invites reflection on the characteristics of the Canadian activism space today: larger issuers being targeted disproportionately, with U.S.-based activists leading high-profile efforts; an increased focus on business strategy in campaigns; and the rising frequency of settlements and few contested shareholder meetings.

There has also been a significant reshaping of the shareholder engagement landscape, with Glass Lewis & Co.'s retreat from benchmark voting; the U.S. administration's executive order targeting the influence of proxy advisors; J.P. Morgan and Wells Fargo's shift away from proxy advisors to in-house AI-assisted voting; and Exxon Mobil's adoption of an automatic retail voting program late last summer.

In this instalment of Governance Insights, we examine these trends and offer insights for both issuers and activists.

The Past Year

Given the strong returns delivered by the S&P/TSX Composite Index in 2024 (approximately 18.5%)1, we might have expected fewer vulnerable targets for activists to target in 2025. Additionally, geopolitical and economic uncertainty early in the year led to a general market slowdown and suggested a slower year for capital markets activity in general. Nonetheless, shareholder activism in Canada proved resilient in 2025, with activity levels (42 Canadian publicly listed companies subject to shareholder demands) consistent with 2024 (39 companies). Activity in the last two years remains only slightly below the average for the four years preceding the COVID-19 pandemic (45 companies).

Despite an inauspicious start, 2025 ultimately delivered stellar stock market returns (approximately 27.4% on the S&P/TSX Composite Index) and witnessed a second-half revival of M&A activity. Activists were generally rewarded for their efforts, as evidenced by their clear track record of success in 2025. Indeed, activists achieved all or part of their objectives in approximately two-thirds of campaigns that sought board representation, higher than the success rate achieved by activists in the prior two years.

Figure 1: Number of Canadian Issuers Subject to Activist Demands (2017 – 2025)

ACTIVISTS CONTINUE TO DISPROPORTIONALLY TARGET LARGER COMPANIES

Larger cap Canadian issuers with a market capitalization over C$1 billion were disproportionally targeted, comprising 30% of the targets in 2025, despite comprising approximately 15% of all operating issuers on the Toronto Stock Exchange and TSX Venture Exchange (excluding exchange-traded funds and close-ended funds). Figure 1 illustrates the historical number of larger cap and total Canadian issuers subject to shareholder demands.

High-profile efforts against larger cap Canadian issuers continue to be principally led by activists in the United States: for the past three years, U.S.-based activists have been responsible for almost half of all demands directed at larger cap Canadian companies. Notable campaigns in 2025 included Elliott Investment Management's engagements with Lululemon Athletica and Browning West's push for change at CAE, which it launched on the heels of its successful 2024 campaign at Gildan Activewear. We expect this trend to continue in 2026, especially given the increase in newly formed U.S. activist funds seeking to carve out a niche, including in the Canadian market. The rising number of players in the space may precipitate an increase in issuers being approached by multiple activists in parallel, forcing the issuer to simultaneously defend against competing demands.

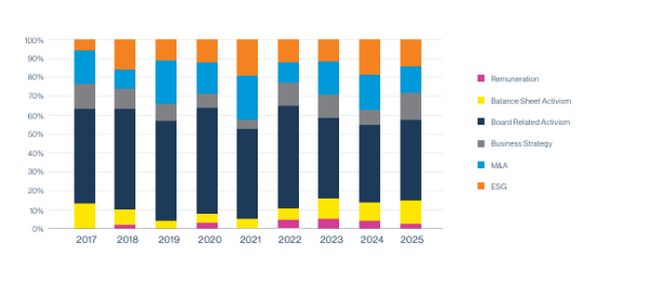

ACTIVISTS SHIFT THEIR FOCUS TO BUSINESS STRATEGY

The variety of shareholder demands has remained largely consistent over the past year, with the notable exception of a surge in campaigns focused on business strategy, which nearly doubled in 2025. In response to the tumultuous geopolitical and economic environment that unfolded throughout the year, companies have been compelled to revisit and refine their strategic direction. Companies that are slow to adapt risk becoming prime targets for activists who are increasingly emphasizing the imperative to build resilient, agile businesses capable of swift operational pivots in response to volatile and rapidly shifting economic and geopolitical landscapes.

Figure 2: Public Demands to Canadian Issuers Proportionally by Type of Demand (2017 – 2025)

FINDING COMMON GROUND: SETTLEMENTS ARE ON THE RISE

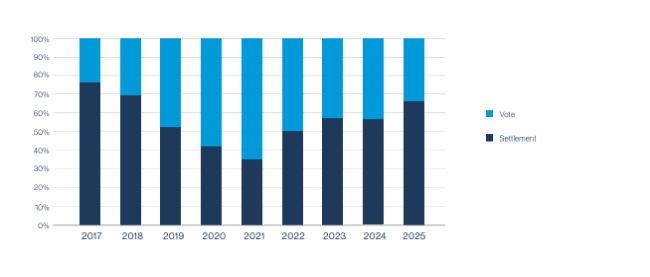

Despite significant activity levels in Canada in 2025, only four campaigns went the distance to a shareholder vote last year, with settlements continuing to dominate outcomes. In 2025, approximately two-thirds of board seats gained by activists at Canadian companies were achieved through settlement, the highest proportion in the last six years. This mirrors the trend in the United States, where over 90% of seats gained by activists at U.S.-based companies were secured by settlement.

Notably, all Canadian companies that proceeded to a contested shareholder vote in 2025 were smaller issuers with market capitalizations below C$200 million, while nearly half of those entering settlements were issuers with market capitalizations exceeding C$1 billion. Historically, large-cap issuers in Canada have overwhelmingly favoured settlements – all such issuers facing demands for board representation from 2022 to 2025 reached settlements. Outcomes for smaller companies remain more varied – on average, only half of non-large-cap issuers subject to demands for board representation over the past five years entered settlements, with the other half proceeding to a shareholder vote.

Figure 3: Board Seats Gained by Activists at Canadian Companies as a Percent of Total Seats Won, by Method Outcome and Year (2017 – 2025)

A Changing Landscape: Developments in Voting

GLASS LEWIS MOVES AWAY FROM BENCHMARK VOTING

In October 2025, Glass Lewis announced that it will phase out its single, one-size-fits-all voting recommendations, transitioning to customized voting policies beginning with the 2027 proxy season. Rather than issuing a benchmark policy reflecting its "house view," Glass Lewis will enable subscribers to select a voting policy better tailored to their priorities. While the approach remains under development, Glass Lewis indicated that clients will have access to a "spectrum of perspectives" to inform voting decisions, including a management-aligned perspective emphasizing board stability and operational execution; a governance fundamentals perspective focusing on board independence, accountability and pay-for-performance; an active-owner perspective prioritizing value creation (most closely resembling the current house view), capital allocation and performance turnarounds; and a sustainability perspective assessing environmental issues, social risks and policies that promote financial opportunities and mitigate materials risks associated with environmental and social issues.

This policy change underscores the growing recognition that shareholders have diverse perspectives and often distinct investment objectives. For activists, Glass Lewis' proposed approach represents a structural rebalancing of the proxy advisory landscape: with the universal "house view" recommendation no longer the dominant voice, well-crafted campaigns can be more precisely calibrated to resonate with specific investor segments and the priorities they value most. For issuers, voting outcomes are likely to become less predictable, requiring companies to deepen their understanding of and engagement with their shareholder base, including shareholders' evolving values and priorities.

While Institutional Shareholder Services Inc. (ISS) stated that it intends to maintain its benchmark guidelines, it has also recently expanded its product offerings for investors, including advisory services that do not include a voting recommendation. This may suggest potential openness by ISS to a more customized approach similar to the model announced by Glass Lewis.

UPDATE: ISS CLARIFIES POLICY ON ADVANCE NOTICE BYLAWS

In late 2025, ISS released its updated proxy voting guidelines for TSX-listed issuers, effective for shareholder meetings on or after February 1, 2026. The guidelines clarify that ISS will not look favourably on advance-notice bylaws that include disclosure requests exceeding requirements under Canadian corporate or securities law. In particular, director questionnaires are likely to be considered unacceptable if they require excessive disclosure or are not made publicly available. The update is clarifying in nature and does not change the substance of ISS' existing guidance on the subject. Notably, we understand that ISS will generally not apply its proxy voting guidelines for TSX listed issuers, including its policies relating to advance notice bylaws, to Canadian-incorporated issuers listed on the TSX that are also U.S. domestic issuers.

To read this article in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]