Provisional Measure nº 563 ("PM 563") has been announced to amend the wording of Law nº 9.430 ("Law 9430") and brought important changes in connection with the transfer price control in Brazil. It should be pointed out that PM 563 was issued in a scenario of intense litigation between the Brazilian Internal Revenue Service and the taxpayers, in particular with respect to the criteria to calculate the RPM according to Normative Instruction 243 ("NI 243").

Resale Price Method (Preço de Revenda menos Lucro - "RPM")

The main change regards the new margins for the RPM. According to the previous legislation, the parameter price (comparable) was calculated based on 20% fixed profit margins for the resale activities, and 60% in the case of local production.

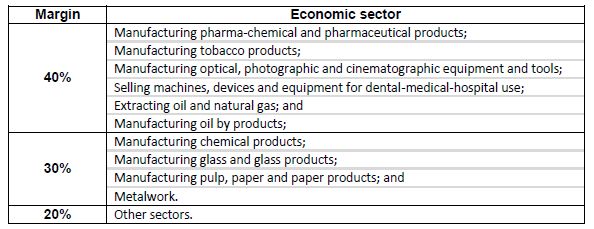

According to the new rules, the RPM has only one profit margin, irrespective of resale or local production. Moreover, the concept of "percentage of the imported product" was included on Law 9430, following the example of NI 243, which had previously introduced such concept without the proper legal instrument. The new profit margins would now vary according to the economic sector, and would be changed by the Ministry of Finance on its own initiative, or by request.

In case the taxpayer is engaged in more than one sector, the applicable margin will correspond to the destination of the goods. If the goods are used in different production processes, the amount of the imported goods will be apportioned, according to the destinations. Below are the new margins:

Another relevant aspect concerns addition of the freight, insurance and import duty in the transaction price, for the purposes of comparison with the parameter price calculated according to the RPM. Under the previous wording of Law 9430 and NI 243, such costs should be added in the transaction price, which may lead to more transfer pricing adjustments. Under the new rules, the freight, insurance and import duty should no longer be added to the transaction price, provided that such costs are paid to third parties who are not resident in tax havens.

Restrictions to the method of Compared Independent Prices (Preços Independentes Comparados - "CUP")

The Provisional Measure also added restrictions with respect to the use of comparable transactions to apply the CUP method. If the comparable transactions have been carried out by the taxpayer himself, such operations must represent at least five per cent of the total amount corresponding to the import operations with related parties in the same fiscal year.

New methods

Two new methods have been established , by quoting the price of the goods and services in commodities and futures exchanges chosen by the Brazilian Revenue Service, both upon import (Preço sob Cotação na Importação – "PCI"), and upon the export (Preço sob Cotação na Exportação – "PECEX").

Spread in international loans

PM 563 introduced variable spread margins for international loan agreements signed between related parties, which will be annually set by the Ministry of Finance. Additionally, the application of transfer pricing rules was extended to all international loan agreements signed between related parties. Previously, the rules were applicable only to those not registered before the Brazilian Central Bank.

Change of method

Law 9430 ensures that the taxpayer may choose the method that represents the lowest adjustment. Notwithstanding, many companies were assessed because the tax inspector deemed that the method indicated in the Income Tax Report could not be changed. According to PM 563, the methods can be changed until the start of a tax inspection procedure.

Moreover, if the tax inspector disregards the method presented by the taxpayer, he must request new calculations according to another method within 30 days. If the new calculation is not presented, the tax inspector can apply other methods with information available.

New rules may be applied in 2012

The new rules become effective in 2013. Nevertheless, taxpayers have the option to adopt the new transfer price rules set forth in the PM 563 in 2012.

(Provisional Measure nº 563, Apr. 03.2012 / DOU, Apr. 04.2012)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.