- with Senior Company Executives, HR and Inhouse Counsel

- in European Union

- in European Union

- with readers working within the Property and Law Firm industries

Article Summary

Many people believe that assets can simply be transferred to a spouse, family trust, company or other related entity before bankruptcy to place them beyond the reach of creditors. In reality, Australian bankruptcy law provides trustees with extensive powers to investigate pre-bankruptcy transactions, recover property, and unwind arrangements that improperly prejudice creditors.

The Bankruptcy Act 1966 (Cth) distinguishes between legitimate long-term asset protection planning and transactions entered into after financial distress has emerged with the purpose of defeating creditors. Whether an arrangement is effective will often depend upon the timing of the transaction, the consideration paid, the debtor’s financial position, the relationship between the parties, and the statutory provisions governing trustee recovery.

This guide explains which assets generally vest in a bankruptcy trustee, which assets may remain protected, how the family home, superannuation, companies and discretionary trusts are treated under Australian law, and when transfers may be challenged under the Bankruptcy Act. It also examines the trustee’s recovery powers under key provisions, including sections 120, 121 and 122, together with the principles developed by the High Court and Federal Court in leading Australian authorities.

Importantly, neither transferring property into another person’s name nor using trusts or corporate structures automatically protects assets from creditors. Australian courts focus on the legal rights created by the transaction, the surrounding circumstances, and whether the statutory requirements for recovery have been satisfied. Even arrangements that appear valid on their face may be scrutinised where they occur against the background of financial distress or creditor claims.

Because every bankruptcy turns on its own facts, effective asset protection requires careful planning well before insolvency becomes foreseeable. Once serious financial difficulty has emerged, transactions intended to preserve wealth become significantly more vulnerable to investigation and potential recovery by a bankruptcy trustee.

Whether you are seeking to protect assets before financial difficulties arise, responding to trustee investigations, or attempting to understand your legal position after bankruptcy has commenced, obtaining early legal advice can substantially affect the outcome.

Asset Protection and Bankruptcy

Asset protection is one of the most misunderstood aspects of Australian bankruptcy law.

Many people assume that transferring assets to a spouse, moving property into a family trust, or restructuring ownership shortly before insolvency will automatically place assets beyond the reach of creditors.

In reality, the Bankruptcy Act 1966 (Cth) gives bankruptcy trustees extensive powers to recover certain transactions, investigate pre-bankruptcy dealings, and challenge arrangements that have the effect of defeating creditors.

Australian bankruptcy law distinguishes between legitimate long-term asset structuring and transactions entered into to shield property once financial distress has already emerged.

That distinction is often highly fact-specific.

The timing of a transfer, the relationship between the parties, the financial position of the debtor, and the commercial reality of the arrangement may all become critical issues if a trustee later investigates the transaction.

In The Trustees of the Property of John Daniel Cummins, A Bankrupt v Cummins [2006] HCA 6; (2006) 224 ALR 280, the High Court considered whether transfers of matrimonial property and shares were void against the trustee in bankruptcy because their main purpose was to defeat or delay creditors.

The Court stated at [34]:

What had been required for the Trustees to succeed at trial was that the circumstances appearing in the evidence gave rise to a reasonable and definite inference, not merely to conflicting inferences of equal degree of probability, that, in making the August transactions, Mr Cummins had the ‘main purpose’ required by the statute.

This article examines what assets may be protected in bankruptcy, what property may still vest in a bankruptcy trustee, when transfers may be reversed under the Bankruptcy Act 1966 (Cth), and when asset protection planning may become ineffective or unlawful under Australian insolvency law.

If you are facing bankruptcy or insolvency proceedings in Australia and require legal assistance contact one of our experienced team of insolvency professionals.

What Happens to Assets When a Person Becomes Bankrupt?

When a person becomes bankrupt in Australia, control of many of their assets passes to a bankruptcy trustee.

Subject to the Bankruptcy Act 1966 (Cth), property belonging to or vested in the bankrupt at the commencement of bankruptcy generally vests in the trustee under s 58. Section 116 separately identifies the property that is divisible among the bankrupt’s creditors and the categories of property that are excluded.

The trustee’s role is to identify, secure, investigate, and realise divisible property for the benefit of creditors.

Section 116 of the Bankruptcy Act 1966 (Cth) defines what property is “divisible among the creditors of the bankrupt”.

Broadly speaking, this includes most real estate, shares, vehicles, bank account balances, investments, and other valuable property owned at the commencement of bankruptcy.

Vehicles may be protected only up to the applicable indexed value limit; higher-value vehicles may be sold by the trustee.

Importantly, bankruptcy may also capture some after-acquired property.

Property acquired by, or devolving on, the bankrupt before discharge may constitute after-acquired property and vest in the trustee, subject to the exclusions in s 116(2). This may include an inheritance received or becoming payable before discharge. The treatment of compensation or damages depends on the nature of the payment and the applicable statutory exemption. Income is dealt with separately under the income-contribution provisions, and contributions may become payable where the bankrupt’s assessed income exceeds the applicable indexed threshold.

Many people mistakenly assume that transferring legal ownership of property before bankruptcy will necessarily prevent trustee recovery.

That is not correct.

A trustee may investigate both the bankrupt’s legal title to property and any equitable or beneficial interest held by the bankrupt. Different issues arise where property has been transferred pursuant to orders made in family-law proceedings.

In Official Trustee in Bankruptcy v Mateo [2003] FCAFC 26, the Full Court considered the interaction between s 121 of the Bankruptcy Act 1966 (Cth) and a transfer of property effected pursuant to orders under s 79 of the Family Law Act 1975 (Cth). The decision turned on the statutory and procedural circumstances of the case and should not be treated as establishing that every transfer made under Family Court orders is either immune from, or automatically vulnerable to, a bankruptcy challenge.

Similarly, in The Trustees of the Property of John Daniel Cummins, A Bankrupt v Cummins [2006] HCA 6; (2006) 224 ALR 280, the High Court examined whether transfers of matrimonial property and other assets were void against the bankruptcy trustee because they were undertaken to defeat creditors.

The proceeding considered whether the evidence supported an inference that the transfers were undertaken with the requisite creditor-defeating purpose under s 121 of the Bankruptcy Act 1966 (Cth).

The Court found at [34]:

What had been required for the Trustees to succeed at trial was that the circumstances appearing in the evidence gave rise to a reasonable and definite inference, not merely to conflicting inferences of equal degree of probability, that, in making the August transactions, Mr Cummins had the ‘main purpose’ required by the statute.

Whether a creditor-defeating purpose may properly be inferred depends on the whole of the evidence, including the timing, financial circumstances, consideration, relationship between the parties, and commercial substance of the transaction.

What Assets Are Protected in Bankruptcy?

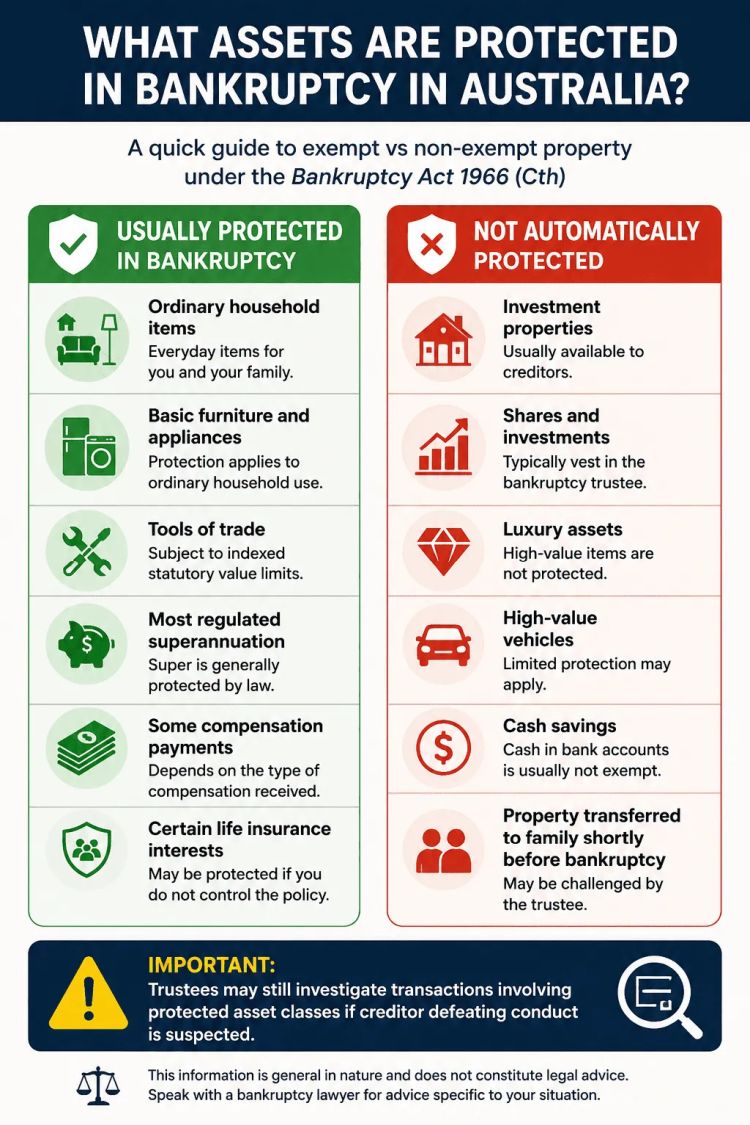

Understanding which assets are exempt under the Bankruptcy Act 1966 (Cth) is critical when assessing what property may remain protected during bankruptcy in Australia.

Exempt Assets in Bankruptcy Under Australian Law

Not all property owned by a bankrupt person becomes available to creditors.

Section 116(2) of the Bankruptcy Act 1966 (Cth) excludes certain categories of property from division among creditors.

These are commonly referred to as exempt assets in bankruptcy.

Subject to the statutory conditions, excluded property may include household property of the kind and quantity reasonably appropriate to the bankrupt’s household, property used by the bankrupt in earning income by personal exertion up to the applicable indexed value, a motor vehicle used principally as a means of transport up to the applicable indexed value, and qualifying interests in regulated superannuation funds. Certain life-assurance interests and damages or compensation relating to personal injury or wrong may also be excluded, although the precise treatment depends on the statutory provision and the character of the payment or interest.

However, these protections are limited and highly technical.

The exemptions under s 116(2) are interpreted according to the statutory language of the Bankruptcy Act 1966 (Cth) rather than broad notions of fairness or hardship.

Whether an asset is protected may depend on its value, ownership structure, use, and the timing of relevant transactions.

Superannuation is frequently misunderstood in this area.

Although qualifying superannuation interests are generally excluded from divisible property under s 116(2), the Bankruptcy Act contains specific provisions permitting recovery of certain superannuation contributions made to defeat creditors. Sections 128B and 128C address contributions made by the bankrupt or by a third party for the bankrupt’s benefit where the statutory requirements are satisfied. The mere fact that a contribution was made before bankruptcy does not, without more, establish that it is recoverable.

Courts determine the parties’ legal rights by applying the relevant statutory provisions and general law. The documentation, consideration, performance of the arrangement, and surrounding commercial circumstances may all be relevant when the court characterises a transaction or determines its purpose.

In Cannane v J Cannane Pty Ltd (In Liquidation) [1998] HCA 26; (1998) 192 CLR 557, Brennan CJ and McHugh J explained that undervalue may be relevant to intent, but does not itself determine whether s 121 applies.

Their Honours stated at [13]:

If property be disposed of by sale and the sale price received by the disponor is equal to the true value of the property at the time of the disposition, the creditors have an undepleted fund against which to prove their debts. But if property is sold for an undervalue or is given away, that fact is relevant to the intent to be attributed to the disponor in disposing of the property.

This reflects the broader principle that bankruptcy courts closely scrutinise transactions that appear designed to place assets beyond creditor reach.

Is the Family Home Protected From Bankruptcy?

One of the most common questions in family home bankruptcy Australia matters is whether a bankrupt person can keep their house.

There is no automatic protection for a family home under the Bankruptcy Act 1966 (Cth).

If a bankrupt person solely owns residential property with available equity, the trustee may seek possession and sale of the property to realise funds for creditors.

Where property is jointly owned with a spouse or partner, the position becomes more complex.

The trustee generally acquires the bankrupt person’s interest in the property, rather than the co-owner’s interest.

The co-owner’s interest does not vest in the bankruptcy trustee. However, the trustee may seek to realise the bankrupt’s interest, including by agreement with the co-owner or by applying for orders for sale under the applicable co-ownership legislation or other available jurisdiction. The co-owner will ordinarily be entitled to their share of the net proceeds after secured liabilities and relevant sale costs are addressed.

Disputes commonly arise regarding beneficial ownership and equitable interests between spouses.

In The Trustees of the Property of John Daniel Cummins, A Bankrupt v Cummins [2006] HCA 6; (2006) 224 ALR 280, the High Court considered both the validity of pre-bankruptcy transfers and the beneficial ownership of matrimonial property. The decision demonstrates that beneficial ownership is determined by applying the relevant equitable principles to the particular facts, including the title, contributions, relationship between the parties and evidence of their intentions. A resulting-trust presumption based on contributions is not invariably decisive in the context of a matrimonial home.

Accordingly, whether a family home is protected in bankruptcy will often depend on ownership structure, available equity, competing equitable interests, and whether earlier transactions may be challenged by the trustee.

Asset Protection Before Bankruptcy: What is Lawful?

Not all asset protection bankruptcy strategies in Australia are unlawful.

Australian law recognises that individuals and business owners may legitimately structure their affairs to manage commercial risk and preserve wealth.

The effectiveness of an asset-protection arrangement may depend on the legal rights created, the timing and consideration for any transfer, the transferor’s solvency, and the purpose for which the transaction was entered into. Under s 121, the relevant question is whether the transferor’s main purpose was to prevent, hinder or delay the transferred property from becoming divisible among creditors. The statutory circumstances permitting an inference of that purpose must be considered separately.

Lawful Asset Protection Strategies

Asset protection is not inherently unlawful under Australian law.

Many individuals and business owners legitimately structure their affairs to manage commercial risk, preserve family wealth, and separate personal assets from business exposure.

However, the legality of asset protection bankruptcy planning often depends on timing, intention, and commercial reality.

Lawful asset protection strategies may include the use of discretionary trusts, corporate structures, superannuation planning, estate planning arrangements, and careful ownership structuring undertaken well before financial distress arises.

Operating a business through a company may separate the company’s liabilities from those of its shareholders because the company is a distinct legal person. That separation does not protect a shareholder from the shareholder’s own personal liabilities, and shares owned by a bankrupt shareholder will ordinarily constitute property available to the bankruptcy trustee unless a particular statutory exclusion applies. Directors may also incur personal liability under guarantees or specific statutory provisions.

In Salomon v Salomon & Co Ltd [1896] UKHL 1; [1897] AC 22, Lord Halsbury LC stated:

Once the company is legally incorporated it must be treated like any other independent person with its rights and liabilities appropriate to itself.

Discretionary trusts are frequently used in long-term estate and business planning. However, their effect in a bankruptcy must be analysed by identifying the precise legal rights held by the bankrupt and the source of the assets held by the trustee.

Property held by the trustee of a valid discretionary trust does not ordinarily become property of a bankrupt discretionary beneficiary merely because the bankrupt may receive distributions or exercise practical influence over the trustee. A beneficiary’s right to due administration of the trust is distinct from ownership of the trust assets.

The bankruptcy trustee may nevertheless acquire any proprietary rights, choses in action, powers or other property that were legally held by the bankrupt and are capable of vesting under the Bankruptcy Act. The trustee may also investigate whether the trust is a sham, whether the bankrupt is the true beneficial owner of particular property, whether trust property is held on resulting or constructive trust for the bankrupt, or whether transfers to the trust are recoverable under ss 120, 121, 128B, 128C or another applicable provision.

ASIC v Carey (No 6) [2006] FCA 814, commonly referred to as Richstar, was an interlocutory freezing-order decision and should not be treated as establishing a general rule that practical control of a discretionary trust makes all trust assets the controller’s property. Kennon v Spry [2008] HCA 56 concerned the distinct property-adjustment jurisdiction under the Family Law Act 1975 (Cth) and likewise does not establish that discretionary-trust assets automatically vest in a bankruptcy trustee.

Why Timing Matters in Asset Protection Bankruptcy Planning

Timing is one of the most important issues in how to protect your assets from bankruptcy lawfully.

An arrangement established before financial difficulty may still be investigated, particularly where questions arise concerning ownership, contributions, sham arrangements or retained beneficial interests. However, the timing and circumstances may make it less likely that a particular transfer satisfies the statutory requirements of ss 120 or 121.

Warning signs may include:

- mounting tax liabilities,

- pending litigation,

- creditor demands,

- loan defaults,

- cashflow problems,

- or exposure to personal guarantees.

Once financial distress becomes apparent, transactions involving transfers to spouses, family trusts, or related entities become significantly more vulnerable to challenge under the Bankruptcy Act 1966 (Cth).

Courts and trustees frequently assess these transactions retrospectively.

Insolvency-related litigation often involves a detailed examination of the debtor’s financial position at the time the transaction occurred, rather than the explanation later provided after bankruptcy commences.

Financial distress does not by itself make every subsequent transaction void. However, evidence that the transferor was insolvent, was about to become insolvent, faced substantial creditor claims, or entered into a transaction that caused insolvency may be relevant under ss 120 and 121. Under s 121, the court must ultimately determine whether the transferor’s main purpose was to prevent, hinder or delay the property from becoming divisible among creditors, applying the statutory inference provisions and all surrounding evidence.

Disposing of Assets Before Bankruptcy: When May a Transfer Be Void or Recoverable?

Australian bankruptcy trustees have extensive powers to investigate and potentially reverse certain transactions entered into before bankruptcy, particularly where creditors may have been prejudiced.

| Transaction | Potential issue |

|---|---|

| Gift of property to a spouse or relative | Possible transfer for no consideration under s 120 and, depending on purpose, s 121 |

| Sale for less than market value | Possible transfer at undervalue under s 120 |

| Transfer to a trust or related entity | May be examined under ss 120 or 121; outcome depends on consideration, timing, solvency and purpose |

| Payment of an existing debt to a relative or other creditor | May constitute a void preference under s 122 if the statutory elements, timing requirements and insolvency conditions are satisfied |

| Historical estate or succession planning | Not automatically protected; validity depends on the legal rights created and whether any recovery provision applies |

| Genuine arm’s-length sale for market value | Less likely to fall within s 120, but may still require consideration under s 121 in unusual circumstances |

| Backdated or fabricated loan documentation | May be ineffective or expose the parties to civil and criminal consequences |

| Superannuation contribution | May be recoverable under ss 128B or 128C if the statutory creditor-defeating requirements are satisfied |

Bankruptcy Transfer of Assets and Undervalued Transactions

One of the most heavily scrutinised areas of Australian insolvency law involves disposing of assets before bankruptcy.

The Bankruptcy Act 1966 (Cth) gives trustees extensive powers to recover certain pre-bankruptcy transactions that improperly reduce the property available to creditors.

Two of the most important provisions are s 120 and s 121 of the Bankruptcy Act 1966 (Cth).

Although they are often discussed together, they operate differently.

Section 120 applies to certain transfers where the transferee gave no consideration or consideration of less value than the market value of the transferred property. It does not require proof that the transferor acted dishonestly or intended to defeat creditors. However, the provision contains statutory qualifications and exclusions, and its operation depends on matters including the date of the transfer, the transferor’s solvency and the relationship between the transfer and the commencement of bankruptcy.

By contrast, s 121 focuses on intention.

It applies where property is transferred with the main purpose of preventing, hindering, or delaying property from becoming available to creditors.

Importantly, transactions involving relatives, spouses, family companies, and discretionary trusts frequently attract close scrutiny because of the ease with which assets may be shifted informally between related parties.

The legal character and effect of a transaction are determined from the parties’ rights, the relevant documentation, the consideration provided, the performance of the arrangement and the surrounding evidence. A transaction described as a sale may fall within s 120 where no consideration, or consideration below market value, was provided. It may fall within s 121 where the statutory main-purpose test is satisfied. Sham documents, fabricated liabilities and backdated agreements may also be legally ineffective or expose the parties to additional consequences.

In Cannane v J Cannane Pty Ltd (In Liquidation) [1998] HCA 26; (1998) 192 CLR 557, the High Court considered allegations involving transfers undertaken in circumstances where substantial liabilities already existed.

The Court found at [92](4):

…facts are the building blocks upon which the decision about the “intent” will ultimately be derived from all of the evidence. Obviously, the fact that the transferor is shown not to have been in a sound financial position at the time of the disposition of property in question will commonly be a prerequisite to the operation of the section, for otherwise an intent to defraud creditors will not so readily be inferred. In judging what that “intent” was, a court is entitled to ask itself: what was the purpose of placing the property at such a time in another’s name? If that purpose was to defeat creditors, the trustee (or liquidator) will be in a strong position to establish that the section attaches.

Likewise, in The Trustees of the Property of John Daniel Cummins, A Bankrupt v Cummins [2006] HCA 6; (2006) 224 ALR 280, the High Court examined whether transfers of matrimonial property were void because their main purpose was to defeat creditors.

The Court affirmed at [34]:

What had been required for the Trustees to succeed at trial was that the circumstances appearing in the evidence gave rise to a reasonable and definite inference, not merely to conflicting inferences of equal degree of probability, that, in making the August transactions, Mr Cummins had the “main purpose” required by the statute…

These principles are central to bankruptcy transfer of assets litigation in Australia.

Can a Bankruptcy Trustee Reverse Asset Transfers?

A bankruptcy trustee may commence recovery proceedings to reverse certain transactions entered into before bankruptcy.

This is often referred to as “clawback” litigation.

Trustees commonly investigate:

- transfers of houses to spouses,

- low value sales to relatives,

- movement of funds into trusts,

- repayment of preferred creditors,

- and transactions involving related entities.

The relevant recovery period depends on the statutory cause of action. Broadly, s 120 may apply to a transfer made within five years before the commencement of bankruptcy. However, a transfer made more than two years before bankruptcy is not void under s 120 where the transferee proves that the transferor was solvent at the time of the transfer. Separate rules determine when the bankruptcy commenced and how the relation-back provisions operate.

Section 121 is not confined to the same two-year or five-year structure. It applies where the statutory creditor-defeating purpose is established, subject to the terms of the section and available protections for relevant third parties. A transaction may also be examined under s 122 if it constitutes a void preference within the applicable statutory period.

In practice, trustees possess broad investigative powers.

They may obtain bank records, taxation material, property records, trust documents, and corporate records when examining suspicious transactions.

The burden of proof may also shift depending on the statutory provision relied upon and the surrounding circumstances.

Importantly, courts do not simply accept a transaction because it was formally documented.

Commercial reality remains critical.

In Official Trustee in Bankruptcy v Mateo [2003] FCAFC 26, the Full Court of the Federal Court considered whether a transfer of a matrimonial home undertaken pursuant to Family Court consent orders could nevertheless be challenged under the Bankruptcy Act 1966 (Cth).

The principal issue raised by the appeal is whether s 121 of the Bankruptcy Act 1966 (Cth) (‘the Bankruptcy Act’) applies to a transfer of property effected pursuant to orders made by the Family Court of Australia under s 79 of the Family Law Act 1975 (Cth).

The Full Court held that the s 121 case advanced against the recipient could not succeed on the facts and statutory notice relied upon. Branson J observed that any available remedy in the circumstances was instead to seek relief in the Family Court under the legislation then applicable.

The decision demonstrates that the legal consequences of a transfer made pursuant to family-law orders depend on the interaction between the Bankruptcy Act, the family-law jurisdiction, the form of the orders and the case actually pleaded. It should not be summarised as establishing that a Family Court order may simply be disregarded or reversed under s 121.

The decision should therefore be treated as turning on the particular statutory procedure, pleaded facts and interaction between bankruptcy and family-law remedies.

What Happens if Assets Are Hidden or Transferred Improperly?

Improper attempts to hide or dispose of assets before bankruptcy may expose a person to significant legal consequences.

Potential consequences may include:

- civil recovery proceedings;

- compulsory examinations and demands for books, records or information;

- an objection to discharge, which may extend the period before discharge to five or eight years depending on the statutory ground;

- adverse costs orders; and

- prosecution for an offence under the Bankruptcy Act 1966 (Cth), where the relevant offence provisions are engaged.

Where a company is also insolvent, separate issues may arise under the Corporations Act 2001 (Cth), including voidable-transaction claims, breaches of directors’ duties, insolvent-trading liability and, in an appropriate case, disqualification. Those corporate remedies are distinct from the recovery powers available to a trustee in an individual’s bankruptcy.

A company’s separate legal personality must be respected unless a recognised statutory or general-law basis permits a different result. The company’s assets are not the personal assets of its shareholders or directors. However, a bankruptcy trustee may realise shares or other property owned by a bankrupt individual, enforce rights belonging to the bankrupt, challenge recoverable transfers made to a company, and pursue any applicable statutory or equitable remedy. Allegedly fabricated or sham documentation must be analysed under the law governing shams, ownership, evidence and the relevant recovery provision rather than by treating separate corporate personality as a merely formal matter.

These issues frequently become central in disputes concerning disposing of assets before bankruptcy and whether a trustee can recover transferred assets.

Family Trusts, Companies, and Bankruptcy: Are They Safe?

Family trusts and companies are frequently used in asset protection and bankruptcy planning in Australia, but they are not automatically immune from creditor claims or trustee scrutiny.

The effect of a company or trust structure depends on the legal and equitable rights created by the arrangement, the ownership of the relevant property, and the application of any statutory or general-law recovery remedy. Control, benefit and the commercial operation of the structure may be relevant evidence, but do not by themselves determine ownership.

Family Trusts and Bankruptcy Risks

Assets validly held by the trustee of a discretionary trust are ordinarily trust property rather than property of an individual beneficiary. A beneficiary does not acquire ownership of any particular trust asset merely because the beneficiary may receive distributions, holds an appointor position or exercises influence over the trustee.

The bankruptcy analysis instead requires identification of the bankrupt’s actual legal and equitable rights. Depending on the trust deed and surrounding facts, those rights might include a vested or contingent interest, a debt owed by the trustee, a right of indemnity, a proprietary cause of action, or a power that is itself property capable of vesting. In other cases, the bankrupt may have only a right to due administration of the trust and an expectancy that the trustee may exercise a discretion in the bankrupt’s favour.

A bankruptcy trustee may investigate whether:

- the bankrupt transferred property to the trust in a transaction recoverable under the Bankruptcy Act;

- the trust is a sham;

- the trustee holds particular property on resulting or constructive trust for the bankrupt;

- the bankrupt has a fixed or vested interest rather than a merely discretionary expectancy;

- money is owed by the trust to the bankrupt;

- the bankrupt misappropriated, concealed or failed to disclose property; or

- a corporate trustee or associated person has a separate liability to the bankrupt estate.

Neither ASIC v Carey (No 6) [2006] FCA 814 nor Kennon v Spry [2008] HCA 56 establishes that practical control alone causes all discretionary-trust assets to vest in a bankruptcy trustee. Richstar was an interlocutory freezing-order decision, while Kennon concerned the distinct statutory jurisdiction of the Family Court.

Company Structures and Personal Bankruptcy

Corporate structures are also frequently misunderstood in bankruptcy planning.

Under Australian law, a company is ordinarily treated as a separate legal entity distinct from its directors and shareholders.

In Salomon v Salomon & Co Ltd [1896] UKHL 1; [1897] AC 22, Lord Halsbury LC stated:

Once the company is legally incorporated it must be treated like any other independent person with its rights and liabilities appropriate to itself.

This principle remains fundamental to Australian corporate law.

However, incorporation does not automatically protect directors from personal exposure.

Directors may nevertheless incur personal liability under guarantees, the insolvent-trading provisions, the director-penalty regime for specified taxation and superannuation liabilities, compensation provisions concerning breaches of duty, or other applicable statutes. A director is not personally liable for every company debt merely because the person holds office as a director.

ASIC v Plymin, Elliott & Harrison [2003] VSC 123; (2003) 46 ACSR 126, is principally relevant to corporate insolvency and the indicia of insolvency considered in an insolvent-trading proceeding. It does not establish that a bankruptcy trustee may disregard a company or trust merely because a bankrupt person exercises practical influence over it.

Companies and trusts may form part of legitimate planning, but their effect depends on the legal ownership of the assets, the rights retained by the bankrupt, any personal liabilities incurred, and the possible application of statutory recovery provisions.

Common Asset Protection Mistakes Before Bankruptcy

Many asset protection mistakes occur after financial distress has already become apparent.

By that stage, transactions intended to preserve wealth are far more likely to attract scrutiny from a bankruptcy trustee or the court.

One of the most common mistakes involves transferring property to a spouse or family member shortly before bankruptcy.

These transactions are frequently challenged under s 120 and s 121 of the Bankruptcy Act 1966 (Cth), particularly where little or no market value was paid.

Creating discretionary trusts after creditor pressure has already commenced may create similar difficulties.

Trust structures established during impending insolvency are often examined closely to determine whether they were genuine commercial arrangements or attempts to place property beyond creditors.

Backdating agreements, documenting sham loans, and creating artificial liabilities also create significant legal risk.

Courts regularly examine the commercial reality of transactions rather than merely accepting the labels attached to them.

Another common misconception is that superannuation is always untouchable.

While many superannuation interests receive statutory protection, contributions made for the purpose of defeating creditors may still become vulnerable to recovery proceedings.

Payment of a genuine debt owed to a family member may be investigated under s 122, but the relationship alone does not make the payment void. The trustee must establish the statutory elements of a preference, including the debtor-creditor relationship, the bankrupt’s insolvency at the relevant time, the applicable statutory period and the preferential effect of the transaction, subject to any available statutory protection or defence.

Tax liabilities are another area commonly underestimated by debtors.

In The Trustees of the Property of John Daniel Cummins, A Bankrupt v Cummins [2006] HCA 6; (2006) 224 ALR 280, the High Court examined transactions undertaken against the background of substantial taxation liabilities and allegations that assets had been transferred to defeat creditors.

The Court described the proceeding as involving:

Whether transfer of assets void against trustee in bankruptcy.

These asset protection mistakes frequently become central issues in litigation concerning illegal asset transfers before bankruptcy.

When Is It Too Late to Protect Assets From Bankruptcy?

One of the most common questions in asset protection insolvency Australia matters is when asset protection planning becomes “too late”.

There is no single statutory cutoff point.

Instead, the issue is highly fact dependent.

Sections 120 and 121 contain different statutory tests. Under s 120, relevant matters include whether the transfer was for no consideration or less than market value, when it occurred and whether the transferor was solvent at the relevant time. Under s 121, the central question is whether the transferor’s main purpose was to prevent, hinder or delay the property from becoming divisible among creditors.

Evidence of insolvency, impending insolvency, creditor demands, litigation, tax liabilities, the relationship between the parties, inadequate consideration, secrecy or continued enjoyment of the property may be relevant, but no single fact necessarily determines the result.

Transactions undertaken after tax demands, litigation threats, loan defaults, or mounting creditor pressure are substantially more vulnerable to challenge.

The court may infer improper purpose from surrounding circumstances even where there is no direct admission of intent.

Importantly, bankruptcy law does not prohibit legitimate historical asset structuring undertaken long before financial distress arises.

The focus is generally on transactions that improperly prejudice creditors once insolvency concerns have emerged.

In Cannane v J Cannane Pty Ltd (In Liquidation) [1998] HCA 26; (1998) 192 CLR 557, the High Court considered allegations involving transfers undertaken after substantial liabilities had already arisen.

The Court stated at [97]:

Mr John Cannane clearly intended that, if he were to become bankrupt (or if JCPL were to be wound up), the creditors at that time should not have available to them the shares in Wisbeck for whatever they were then worth. His intention (and thus the intention of JCPL) was to deprive the creditors of something to which they would, at that time, be entitled, namely the then value of the Wisbeck shares. In this sense, his intention was to defeat future creditors, that is, creditors in the future.

Similarly, in The Trustees of the Property of John Daniel Cummins, A Bankrupt v Cummins [2006] HCA 6; (2006) 224 ALR 280, the High Court examined whether the “main purpose” of the transfers was to defeat or delay creditors.

Accordingly, there is no universal point at which asset planning becomes “too late”. Each transfer must be assessed under the applicable provision, including the consideration provided, its timing, the transferor’s solvency and, where s 121 is relied upon, the transferor’s main purpose.

Key Takeaways on Asset Protection

Asset protection and bankruptcy law in Australia involves far more than simply transferring assets out of a person’s name once financial pressure emerges.

The Bankruptcy Act 1966 (Cth) gives trustees extensive powers to investigate transactions, recover property, and challenge arrangements that improperly prejudice creditors.

While legitimate long term asset structuring may form part of prudent financial planning, the distinction between lawful planning and creditor-defeating conduct often depends on timing, intention, and commercial reality.

Each transaction must be assessed under the applicable statutory or general-law test. Transfers to spouses, trusts, companies or other related parties may be recoverable where the requirements of provisions such as ss 120 or 121 are satisfied.

Assets validly owned by a company or held by the trustee of a trust do not become property of a bankrupt individual merely because that individual exercises influence or may receive benefits. The relevant inquiry concerns the bankrupt’s actual legal and equitable rights, together with any recoverable transfers or other available remedies.

Importantly, bankruptcy law is not designed to punish ordinary historical asset ownership arrangements undertaken years before financial difficulty arises.

Rather, the law principally targets transactions that operate to improperly place assets beyond the reach of creditors once insolvency concerns have crystallised.

Because these issues are highly fact sensitive, even seemingly informal family arrangements may ultimately become the subject of trustee recovery proceedings, public examinations, or complex litigation concerning ownership and creditor rights.

Frequently Asked Questions

The following frequently asked questions address common issues in asset protection bankruptcy Australia matters, including family trusts, superannuation, property transfers, trustee recovery powers, exempt assets, and when transactions may become vulnerable under the Bankruptcy Act 1966 (Cth).

Can I transfer my house to my spouse before bankruptcy?

Possibly, but the transfer may later be challenged by a bankruptcy trustee under s 120 or s 121 of the Bankruptcy Act 1966 (Cth).

Transfers for less than market value, or transfers made to defeat creditors, are particularly vulnerable.

The outcome may depend on the consideration provided, the date of the transfer, the transferor’s solvency and, under s 121, whether the transferor had the required main purpose of preventing, hindering or delaying the property from becoming divisible among creditors.

What assets are protected in bankruptcy in Australia?

Some assets are exempt under s 116(2) of the Bankruptcy Act 1966 (Cth).

These may include ordinary household items, certain personal effects, tools of trade up to the indexed limit, and most regulated superannuation interests.

However, exemptions are technical and limited.

Not all property is protected simply because it is used personally or held within a family arrangement.

Is superannuation protected from bankruptcy?

In many cases, properly constituted superannuation is protected from creditors under the Bankruptcy Act 1966 (Cth).

However, contributions made to superannuation with the intention of defeating creditors may still be recoverable by a bankruptcy trustee.

Large or unusual contributions made shortly before bankruptcy often attract close scrutiny.

Can a bankruptcy trustee recover assets transferred to family members?

Yes.

A trustee may seek to recover assets transferred to spouses, children, relatives, trusts, or related companies if the transfer falls within the clawback provisions of the Bankruptcy Act 1966 (Cth).

This commonly arises where property was gifted, sold below market value, or transferred after financial distress had already emerged.

Are family trusts protected from bankruptcy?

Not automatically.

The relevant question is what legal or equitable property, if any, the bankrupt owns. Appointor powers, trustee roles, beneficiary rights and the terms of the trust deed may be relevant to that inquiry, but practical control or receipt of discretionary benefits does not, without more, make all trust assets property of the bankrupt.

Can creditors access trust assets in Australia?

Ordinarily, a personal creditor of a discretionary beneficiary cannot execute directly against trust assets merely because the debtor is a beneficiary or exercises influence over the trust. Different consequences may follow where the debtor has a fixed or vested proprietary interest, is owed money by the trust, is the true beneficial owner of particular property, holds a power that constitutes property, or has transferred assets to the trust in a transaction recoverable under the Bankruptcy Act. A sham trust or other legally ineffective arrangement will also not achieve asset separation.

How far back can a bankruptcy trustee investigate transactions?

The period depends on the recovery provision. A transfer at undervalue under s 120 may fall within a five-year period before bankruptcy, although a transfer made more than two years before bankruptcy is not void under that section if the transferee proves the transferor was solvent when the transfer occurred. Section 121 applies a different creditor-defeating-purpose test and is not confined to that same two-year or five-year structure. Preferences under s 122 and superannuation contributions under ss 128B and 128C are governed by their own statutory requirements. The calculation may also depend on the commencement and relation-back provisions of the Act.

Does bankruptcy automatically wipe all debts?

No.

Discharge releases the bankrupt from most debts that were provable in the bankruptcy, but statutory exceptions apply. Depending on the precise liability, these may include penalties or fines imposed by a court, maintenance liabilities, certain debts incurred by fraud or fraudulent breach of trust, liabilities under proceeds-of-crime legislation and certain student-assistance debts. Discharge also does not extinguish a secured creditor’s rights against its security, although any unsecured shortfall may be dealt with as a provable debt unless another exception applies.

Can I sell assets before bankruptcy?

Selling assets before bankruptcy is not automatically unlawful.

However, transactions conducted below market value, involving related parties, or undertaken to defeat creditors may later be challenged by a trustee.

Courts closely examine whether the transaction had genuine commercial substance and whether fair consideration was paid.

When is it too late to protect assets from bankruptcy?

There is no fixed date.

There is no single date on which all planning becomes ineffective. Each transaction must be tested against the relevant provision. A transfer for no consideration or less than market value may be recoverable under s 120 within the applicable period, while a transfer made with the main purpose described in s 121 may be void under that provision. Evidence of insolvency, impending insolvency and creditor pressure may be highly relevant, but the precise statutory elements must still be proved.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]