- with readers working within the Accounting & Consultancy and Banking & Credit industries

- within Real Estate and Construction, Litigation, Mediation & Arbitration and Consumer Protection topic(s)

On 20 March 2018, the governments of France and Luxembourg signed a new double tax treaty ("New Treaty") replacing the current treaty dated 1 April 1958 ("Old Treaty").

The Old Treaty was in force for almost six decades and had been amended several times (the 4th and latest amendment of the Old Treaty entered into force only last year) These amendments were necessary in particular to accommodate OECD developments in the field of the exchange of information and to close a well-known loophole resulting from the divergent interpretations of Luxembourg and French case law on income derived from French real estate by a Luxembourg company. Nevertheless, Luxembourg remained a hub for structuring French real estate investments through Luxembourg funds. The New Treaty contains substantial derogations from the 2017 OECD Model Tax Convention ("OECD MTC").

The main differences between the Old Treaty and the New Treaty may be summarised as follows:

Residence

The residence definition generally follows article 2 OECD MTC, but is completed by the following precisions:

- in the case of France, residents include partnerships (société de personnes), groups (groupement de personnes) or similar entities:

-

- whose place of effective management is situated in France;

- which are subject to tax in France; and

- whose unitholders, partners or members are, pursuant to French tax law, personally liable to tax on their portion of profits of these partnerships, groups or similar entities;

- a trustee or fiduciary is not considered a resident of a Contracting State even if covered by the definition of a resident, to the extent that it is only the apparent beneficiary of the income, while such income benefits in fact, directly or indirectly through the intermediary of other individual persons or companies, another person which does not qualify as a resident of one of the Contracting States.

Pursuant to the protocol to the New Treaty ("Protocol"), it is understood that an undertaking for collective investments ("UCI") that is resident in a Contracting State and assimilated under the laws of the other Contracting State to a domestic UCI, benefits from articles 10 (dividends) and 11 (interest) for the portion on the income corresponding to the entitlements of residents of either Contracting State or of a State with which the source State has concluded a treaty on administrative assistance for the purpose of preventing tax evasion and avoidance. The situation of UCIs is improved compared to the Old Treaty by being able to claim the exemption / reduced withholding tax rate on dividends under the aforementioned conditions.

Permanent establishment

The definition of a permanent establishment is updated and reflects the provisions of article 5 OECD MTC.

A building site or construction or installation project constitutes a permanent establishment only if it lasts more than 12 months (as opposed to 6 months under the Old Treaty). Said 12- month period is however calculated broadly: separate periods of activity of more than 30 days by an enterprise on a building or construction site in the other State are added to determine the 12- month period. Similarly, periods of connected activity of more than 30 days exercised on said building or construction site by an enterprise closely linked to the main enterprise are also taken into account for the 12-month computation.

Dividends

The new article 10 relating to dividends is likely to have the most significant impact on existing cross-border investments:

- it provides for an exemption

from withholding tax of the gross amount of the dividends

if the beneficial owner is a company which holds directly

at least 5% of the capital of the company paying

the dividends throughout at least a 365 day period

that includes the day of the payment of the dividend (for the

purpose of computing that period, no account shall be taken of

changes of ownership that would directly result from a corporate

reorganisation, such as a merger or divisive reorganisation, of the

company that holds the shares or that pays the dividend).

It is noteworthy that the New Treaty is in this respect more favourable that the OECD MTC that only foresees a reduced rate of 5% in case of a holding of at least 25%. By comparison, article 119ter of the French General Tax Code (implementing the parent-subsidiary directive) requires a minimum participation of 10% for the exemption; - it provides for a withholding

tax rate of 15% of the gross amount of dividends

originating from income or capital gains derived from real estate

by an investment vehicle situated in a Contracting State (i) that

distributes the major portion of this income annually and (ii)

whose income and gains derived from such real estate are exempt

from tax, provided that the beneficial owner thereof is a resident

in another Contracting State holding directly or indirectly a

participation representing less than 10% of the share

capital of the distributing investment vehicle. In case

the beneficiary of such dividends holds directly or indirectly a

participation representing 10% or more of the share

capital of the distributing investment vehicle, the

dividends are subject to tax at the rate foreseen by the domestic

tax laws of the source State.

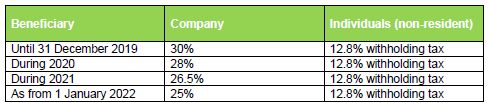

The aforementioned provision is likely to affect distributions made by French exempt real estate vehicles (typically established as organismes de placement collectif en immobilier – "OPCIs" - or as sociétés d'investissement immobilier cotées – "SIICs") which were subject under the Old Treaty to the reduced rate of 5%, in case the beneficiary was a Luxembourg company holding directly 25% of the distributing vehicle. Under the New Treaty, France is allowed to tax such dividend according to its domestic tax law, which applies the following rates:

The current exemption existing under the Old Treaty for dividends paid by French corporate taxpayers (including exempt real estate vehicles like OPCIs and SIICs) and received by Luxembourg corporate taxpayers with a participation of at least 25% will no longer apply under the New Treaty. In practice, Luxembourg institutional investors owning 10% or more of such a French exempt real estate vehicle would see their French taxation on dividends rise from 5% currently to 30%; - Finally, it provides for a 15% rate in all other cases.

Interest

The New Treaty does not allow for any withholding tax on interest. This derogation should have limited impact given that neither France nor Luxembourg levies withholding tax on interest (subject to exceptions).

Royalties

The New Treaty introduces the possibility of a 5% withholding tax. It is noteworthy that Luxembourg does not levy any withholding tax on royalties.

Capital gains

The capital gains treatment follows article 13 OECD MTC, including the taxation of gains from the alienation of shares or comparable interests which, at any time during the 365 days preceding the alienation, derived more than 50% of their value directly or indirectly from immovable property situated in a Contracting State in that State.

In addition however, the New Treaty allocates the right to tax a capital gain realised by an individual resident in a Contracting State on a substantial participation in the share capital of a company resident in the other Contracting State to such other Contracting State. A participation is deemed to be substantial if the beneficiary alone or together with his family, owns directly or indirectly shares, units or other rights providing an entitlement to the profits of the company of 25% or more. This provision however only applies to gains realised by a resident of a Contracting State who was a resident of the other Contracting State within the 5 years preceding the alienation. A similar provision was not included in the Old Treaty.

Employment income

Following the OECD MTC, employment income is generally taxable only in the State where the professional activity is exercised, save for temporary missions which do not exceed 183 days and for which the remuneration is paid and borne by an employer in the employee's State of residence.

The Protocol further specifies that a resident of a Contracting State who pursues employment in the other Contracting State and who, during a taxable period is physically present in the first State and/or in a third State to pursue employment during one or more periods not exceeding in aggregate 29 days, is deemed to have effectively exercised his professional activity in the other State for the whole taxable year. This provision is of significant interest for the 95,000 French commuters who are employed in Luxembourg: in case they are professionally active either in France or in a third State (being neither France nor Luxembourg), they will remain taxable only in Luxembourg provided their activity outside Luxembourg does not exceed 29 days within the fiscal year.

Capital

The New Treaty follows article 22 OECD MTC and capital represented by immovable property may be taxed in the State where it is situated. This provision allows France to tax French real estate directly owned by Luxembourg residents in accordance with the new wealth tax on real estate (impôt sur la fortune immobilière).

Indirect holdings through companies may however not be taxed in France.

Entitlements to benefits

The New Treaty includes an anti-abuse provision as provided for by article 20 OECD MTC. Accordingly a benefit under the New Treaty shall not be granted in respect of an item of income or capital if it is reasonable to conclude, having regard to all relevant facts and circumstances, that obtaining that benefit was one of the principal purposes of any arrangement or transaction that resulted directly or indirectly in that benefit, unless it is established that granting that benefit in these circumstances would be in accordance with the object and purpose of the relevant provisions of the New Treaty.

Entry into force

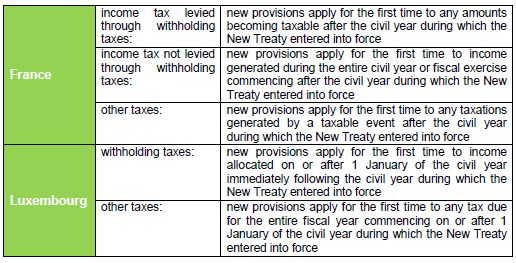

The New Treaty will enter into force after the notifications regarding the ratification by each Contracting State have been exchanged.

The provisions of the New Treaty will apply as follows:

Outlook

It is regrettable that the New Treaty does not foresee any transitional provisions to give the industry sufficient time to adapt its cross-border investment structures, in particular as regards the new dividend treatment of French real estate vehicles, which furthermore is not in line with the 2017 OECD MTC.

In practice, the application of the New Treaty as early as 2019 will require that the ratification process by the respective parliaments, as well as the exchange of the notifications thereof, be finalised by the end of this year.

In the meantime, it may be expected, in the light of the new tax treatment of dividends distributed by French real estate vehicles to Luxembourg residents, that the relevant real estate investment structures will need to be revisited.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.