- within Government, Public Sector, Finance and Banking and Insurance topic(s)

- with readers working within the Technology industries

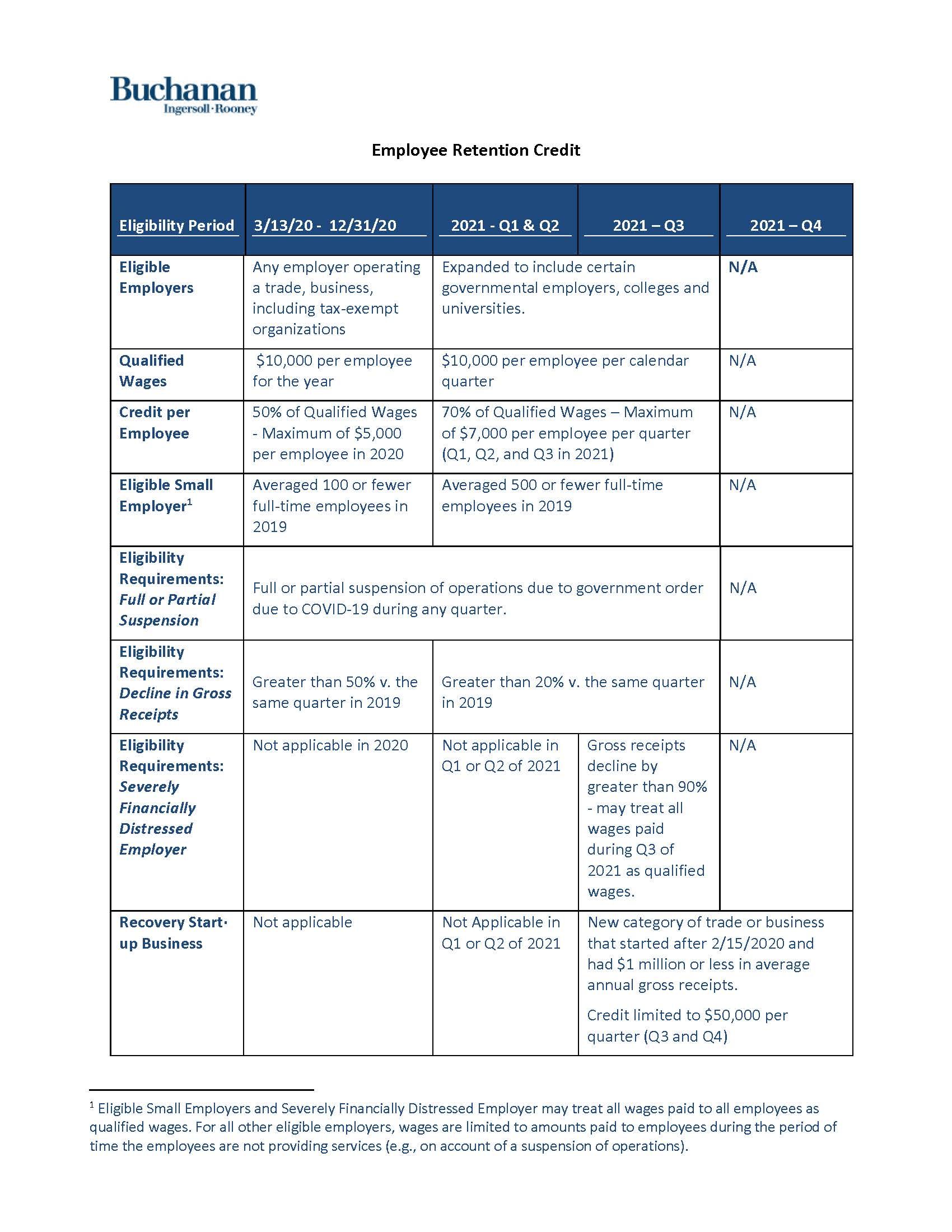

The Employee Retention Credit (ERC) is a refundable tax credit against certain payroll taxes that was originally created under the CARES Act to assist businesses in covering the cost of keeping workers employed during the pandemic. The ERC is available to trades or businesses whose operations were subject to a full or partial suspension on account of a governmental order, or who experienced a significant decline in gross receipts during the pandemic. The amount of the credit is calculated based on a percentage of "qualified wages," including allocable qualified health plan expenses that an eligible employer pays to employees.

Who qualifies for the ERC?

The ERC is available to trades or businesses whose operations were subject to a full or partial suspension of operations on account of a governmental order, or who experienced a significant decline in gross receipts during the pandemic. The eligibility rules for calendar years 2020 and 2021 vary, as described in more detail below.

Are non-profit organization eligible for the ERC?

Yes. for purposes of the ERC, a non-governmental tax-exempt organization described in section 501(c) of the Internal Revenue Code that is exempt from tax under section 501(a) of the Code is deemed to be engaged in a "trade or business" with respect to all operations of the organization.

Can trades or business who received a PPP loan qualify for the ERC?

Yes. Originally, employers were required to choose between taking a Paycheck Protection Program (PPP) loan or applying for the ERC. The Taxpayer Certainty and Disaster Tax Relief Act of 2020 eliminated this restriction and eligible employers can claim the ERC even if the employer has received one or more PPP loans. An eligible employer, however, cannot claim the ERC on any qualified wages that it used to obtaining PPP loan forgiveness (i.e., no double dipping).

What rules apply for purposes of calculating the ERC for 2020 (IRS Notice 2021-20)?

For calendar year 2020, employers are eligible to claim the ERC if they operated a trade or business during the calendar year and experienced either:

1. A full or partial suspension of the operation of their trade or business during any calendar quarter on account of a governmental order limiting commerce, travel or group meetings due to COVID-19; or

2. A significant decline in gross receipts by more than 50% when compared to the same quarter in the prior year (beginning with the calendar quarter starting January 1, 2020).1

The maximum amount of qualified wages taken into account with respect to each employee for all calendar quarters is $10,000, so that the maximum credit for an eligible employer for qualified wages paid to any employee is $5,000 (50% of $10,000).

For an employer that averaged more than 100 full-time employees in 2019 (a large eligible employer), qualified wages are generally those wages paid to employees that are not providing services because operations were fully or partially suspended or due to the decline in gross receipts. For an employer that averaged 100 or fewer full-time employees in 2019 (a small eligible employer), qualified wages are generally those wages paid to all employees during a period that operations were fully or partially suspended or during the quarter that the employer had a decline in gross receipts regardless of whether the employees are providing services.

What rules apply for purposes of calculating the ERC for 2021 (IRS Notices 2021-23, 2021-49 and Code Section 3134)?

For calendar year 2021, eligible employers can claim a credit against 70% of qualified wages they pay to employees after December 31, 2020 and before October 1, 2021, up to a maximum $10,000 limit per employee, per calendar quarter in 2021 (resulting in a maximum credit of $7,000 per quarter per employee – a total of $21,000 for 2021).2

Effective January 1, 2021, employers are eligible to claim the ERC if they operated a trade or business during 2021, and experienced either:

1. A full or partial suspension of the operation of their trade or business during a calendar quarter on account of a governmental order limiting commerce, travel or group meetings due to COVID-19; or

2. A decline in gross receipts in the first, second or third calendar quarter in 2021 where the gross receipts of that calendar quarter are less than 80% of the gross receipts in the same calendar quarter in 2019.3

For purposes of determining eligibility based on a decline in gross receipts, employers are permitted to elect to use an alternative quarter to calculate gross receipts.4 Under this election, an employer may determine if the decline in gross receipts test is met for a calendar quarter in 2021 by comparing its gross receipts for the immediately preceding calendar quarter with those for the corresponding calendar quarter in 2019. For example:

- For the first calendar quarter of 2021, an employer may elect to use its gross receipts for the fourth calendar quarter of 2020 compared to those for the fourth calendar quarter of 2019; and

- For the second calendar quarter of 2021, an employer may elect to use its gross receipts for the first calendar quarter of 2021 compared to those for the first calendar quarter of 2019.

Effective January 1, 2021, for purposes of claiming the ERC based on qualified wages paid in 2021, a large eligible employer is defined as an employer that averaged more than 500 full-time employees in 2019 (as opposed to 100 full-time employees).

How does the ERC affect federal income taxes (income and deduction)?

The IRS has indicated that the ERC is not included in gross income for federal income tax purposes. The ERC, however, does reduce the expenses that an eligible employer can otherwise deduct on its federal income tax return (i.e., no deduction may be taken for the portion of wages paid equal to the sum of credits determined for the applicable taxable year).

Is there still time to claim the ERC?

Yes. There is still time to retroactively claim the ERC by filing a Form 941-X (Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund).

The statute of limitations for filing amended quarterly returns is generally three years from the date of filing the Form 941. For example, in order to apply for the Employee Retention Credit for the second quarter of 2020, the amended return needs to be submitted by July 2023.

Employers should seek out experienced legal counsel to discuss eligibility and minimize risk during the claims process. To help employers navigate the ins and outs of ERC eligibility and claims, our team of employee benefits attorneys created an Employee Retention Credit Eligibility Questionnaire and summary chart of the eligibility requirements below. Click here to request your copy of the Employee Retention Credit Eligibility Questionnaire.

Footnotes

1. A significant decline in gross receipts begins on the first day of the first calendar quarter of 2020 during which an employer's gross receipts are less than 50% of its gross receipts for the same calendar quarter in 2019. A significant decline in gross receipts ends on the earlier of January 1, 2021, or the first calendar quarter following the calendar quarter in which the employer's gross receipts are more than of 80% of its gross receipts for the same calendar quarter in 2019.

2. Section 80604 of the Infrastructure Act amended section 3134(n) of the Code to provide that the employee retention credit under section 3134 shall apply only to wages paid after June 30, 2021, and before October 1, 2021. Accordingly, the ERC is not available for the fourth quarter of 2021.

3. Compare to 2020, where an employer is considered to have a significant decline in gross receipts in any calendar quarter in which the employer's gross receipts are less than 50% of the gross receipts in the same calendar quarter in 2019.

4. See, Section 2301(c)(2)(B) of the CARES Act, as amended by section 207(d)(2) of the Relief Act.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]