- within Law Department Performance topic(s)

- with readers working within the Banking & Credit and Oil & Gas industries

The Court of Appeal's ("CA") ruling in April 2024 in the case of BlackRock Holdco 5 LLC v HMRC ("BlackRock")1 considered the deductibility of interest on a $4 billion intra-group loan put in place as part of the funding structure for a commercial acquisition. The CA reversed the decision of the Upper Tribunal ("UT")2 on the transfer pricing issue and concluded that the deductions for interest would not be restricted under the transfer pricing rules. However, the CA agreed with the UT that no tax relief was due as the interest costs were disallowed under the loan relationships unallowable purpose rule.

Background

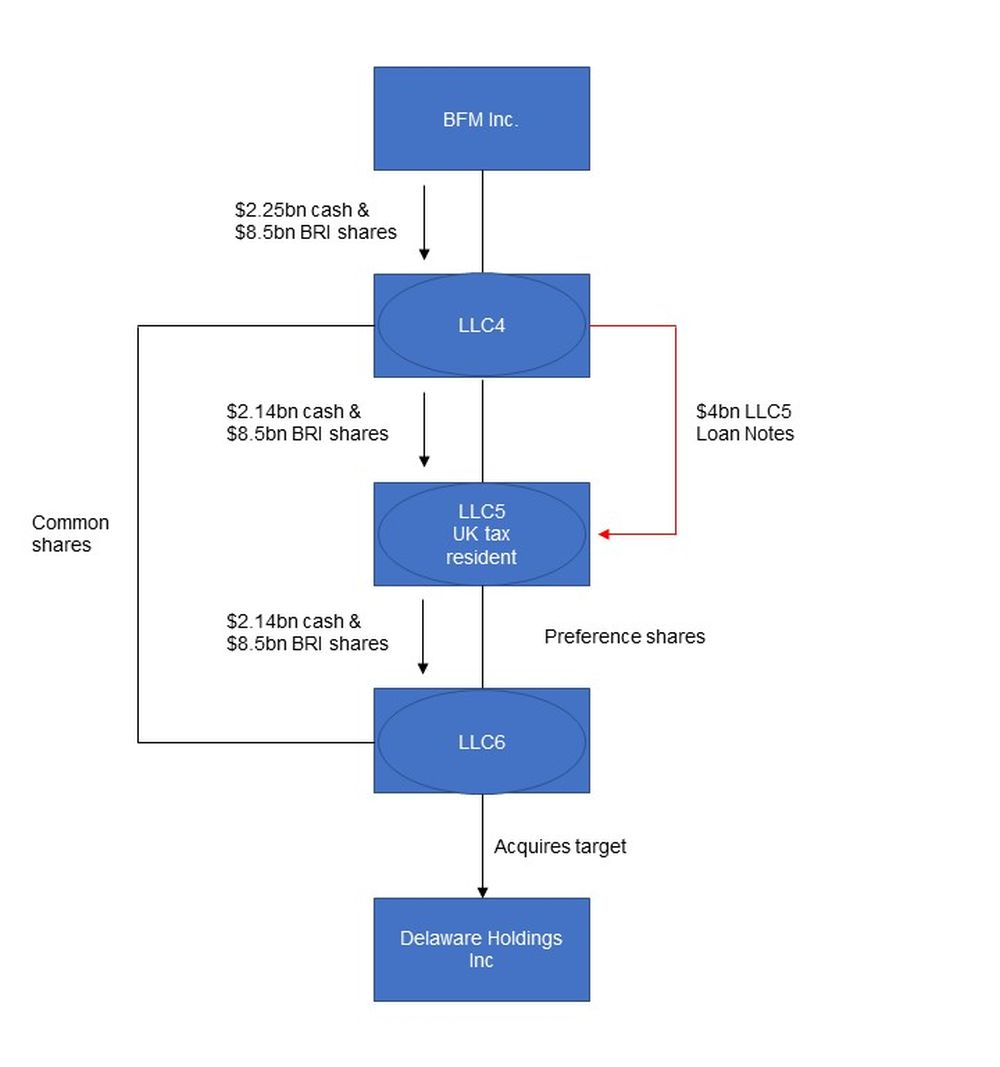

The litigation concerned the acquisition by BlackRock, in 2009, of the unrelated North American operations of Barclays Global Investors. The structure used by BlackRock for the acquisition included a newly formed Delaware incorporated but UK tax resident company ("LLC5"), which issued loan notes to its parental entity in the BlackRock group totalling $4 billion (the "LLC5 loan notes"). LLC5 lent the funds borrowed to a subsidiary company to effect the acquisition of the target company shares.

BlackRock Holdco 5 LLC (Court of Appeal's diagram of the financing arrangements):

Transfer pricing

On the transfer pricing issue, the CA overruled the decision of the UT and agreed with the First Tier Tribunal ("FTT") that interest deductions on the LLC5 loan notes would have qualified on transfer pricing grounds. The FTT had found that even though the usual arm's-length covenants and guarantees that would typically have been included in an arm's-length transaction were not in place, one could presume they were included.

The UT disagreed with this approach and held that only the actual terms of the lending were relevant to consider in the transfer pricing analysis. As an independent lender would have looked for the usual covenants and guarantees that the loan would be serviced, and such covenants and guarantees were absent, the interest deductions fell to be disallowed under the transfer pricing rules.

The CA overruled the decision of the UT and agreed with the FTT that it was not necessary to put formal covenants and guarantees in place for all internal borrowing. The lender (a US company referred to as "LLC4" in the judgement) had no need of such covenants and guarantees, the CA determined. Independently, LLC4 controlled the borrower (another US entity referred to as "LLC6" in the judgement)3 through owning the shares in the borrower's parent (being LLC5). The additional, artificial, inclusion of arm's-length covenants and guarantees would have added nothing in a situation where the lender (LLC5) had equivalent protection for its lending under the actual contractual, and share ownership, arrangements which existed within the group.

Unallowable purpose: Legislative Background and Tribunal Decisions

Under s442 of Corporation Tax Act 2009 ("CTA 2009"), if the main or one of the main purposes of being a party to a debt and paying interest is "a tax avoidance purpose", then this is an "unallowable purpose". Under section 441 of CTA 2009, interest costs are denied a deduction for corporation tax purposes to the extent that they relate on a "just and reasonable" apportionment to that unallowable purpose.

HMRC's challenge to disallow the interest deductions claimed by LLC5 relating to the LLC5 loan notes failed at the FTT. The FTT decided that, although there was an "unallowable purpose" of tax avoidance for entering into the LLC5 loan notes, there was also a commercial purpose. The FTT ruled that none of the interest deductions should be attributed to an unallowable purpose on a just and reasonable apportionment, with the effect that the interest costs were deductible in full.4

The UT overruled the findings of the FTT regarding the identification of an unallowable purpose. The UT stated that although there was both a commercial and tax purpose for the lending, the FTT had made a mistake in its "just and reasonable apportionment" of the proportion of the interest costs which were deductible, and all of the interest costs should be attributable to the unallowable purpose. The UT found there was no other reason, aside from obtaining a tax advantage, for LLC5 (being a UK resident entity) to exist at all in the predominantly US group structure. "Absent [the UK] tax benefits, LLC5 would not have existed", the UT had determined.5

Unallowable purpose: the CA's determination

The CA found that LLC5 had both a commercial and a tax main purpose for entering into the LLC5 loan notes. In deciding whether a loan relationship has an unallowable purpose, the courts look at "the company's subjective purpose or purposes in being a party to the loan relationship in question".6 That purpose for which a company is party to a loan may, or may not, be the same as, for example the purpose for which a company exists. The subjective element required analysing the purpose for LLC5 in the structure, and looking at the facts to determine the directors' intention. It was a matter for tribunals to determine on all the facts and did not just depend on the directors' categorisation of the arrangements. There were sufficient grounds on the facts, the CA stated, to conclude the arrangements regarding LLC5 "not only had no commercial rationale but had no real commercial function". These grounds included the fact that LLC5, as a UK resident company, had been inserted into "what is otherwise a wholly US-based, and equity funded, ownership chain".7

Unallowable purpose: "just and reasonable apportionment"

The process by which there was to be a "just and reasonable apportionment" of the purposes for which LLC5 was a party to the LLC loan notes loan (and thereby the attribution of interest costs) was to be determined objectively. The CA found on the relevant facts of the case that there was no principled basis to identify any particular amount or proportion of the debits as being attributable to the commercial purpose. The CA held that the purposes for which LLC5 was created could not be divorced from its purpose in entering the loans. The commercial advantage of the lending was "more in the nature of a by-product"8 of the transaction. The CA concluded that "in the absence of the tax advantage the decision to enter into the Loans would never have been made".9

Commentary

The decision in BlackRock, as with JTI Acquisition Company (2011) Ltd v HMRC,10 exemplify the need for taxpayers to ensure that they have sufficient contemporaneous evidence to support the commercial purpose of a UK resident company in obtaining a funding for a commercial acquisition. Where the evidence suggests that the main purpose may not be for commercial reasons but rather for an unallowable purpose, there will be a risk of disallowance of interest costs.

The CA's judgement is careful to state that the identification that LLC5 had a tax-focused main purpose was a conclusion which was reached on the facts of the case. A focus and awareness of the tax deductibility of interest costs was not, by itself, sufficient to trigger the unallowable purposes rule. Directors being aware of tax considerations regarding the deductibility of interest costs is not enough, by itself, to prevent that expense being deductible.

The key focus is on the purpose of the arrangements, and how that purpose came into existence. "However it might be dressed up, LLC5 became a party to the Loans to obtain a tax advantage"11, the leading judgement at the CA stated. With a different purpose for the interposition of LLC5 in the group structure, however, the outcome might have been different.

Footnotes

1. BlackRock Holdco 5 LLC v HMRC [2024] EWCA Civ 330.

2. Cadwalader covered the earlier Upper-tier Tribunal judgement in BlackRock, in a previous Brass Tax article: HMRC v BlackRock Holdco 5 LLC Throws a Spotlight on UK Transfer Pricing and the 'Unallowable Purposes' Rule - Brass Tax (cadwalader.com).

3. Please see diagram on the BrassTax Webpage.

4. BlackRock, para 101.

5. BlackRock, para 180.

6. BlackRock, para 106.

7. BlackRock, para 171.

8. BlackRock, para 182.

9. BlackRock, para 185.

10. JTI Acquisitions Company (2011) Ltd v HMRC [2023] UKUT 194. For further details please refer to the BrassTax article, Examining "Purpose" - Brass Tax (cadwalader.com).

11. BlackRock, para 163.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]