- within Intellectual Property topic(s)

- with readers working within the Retail & Leisure industries

Purchase price adjustment mechanisms are common in private M&A transactions to determine the final price to be paid by the buyer. However, the manner in which the price adjustment is achieved varies by jurisdiction. In the US, it is common to adjust the purchase price for cash, any excess or deficit of net working capital relative to a required level of net working capital, unpaid debt, and unpaid transaction expenses of the target business as of the closing, with an adjustment done at closing based on estimates and followed by a post-closing true-up. In the UK and Asia, what is commonly referred to as the "locked-box" approach is more frequently used, particularly in auction processes, corporate carve outs and private equity transactions.

What is a locked-box pricing mechanism?

The parties agree on a fixed price by referencing a set of agreed historical accounts – this is typically the last set of audited financial statements, but sometimes they're unaudited management accounts or a set of accounts prepared specifically for these purposes –referred to as "locked-box accounts." The locked-box accounts fix the equity price in respect of the cash, debt and working capital actually present in the target business at the date of the locked-box accounts, and determine the equity price that is written into the sale and purchase agreement (SPA).

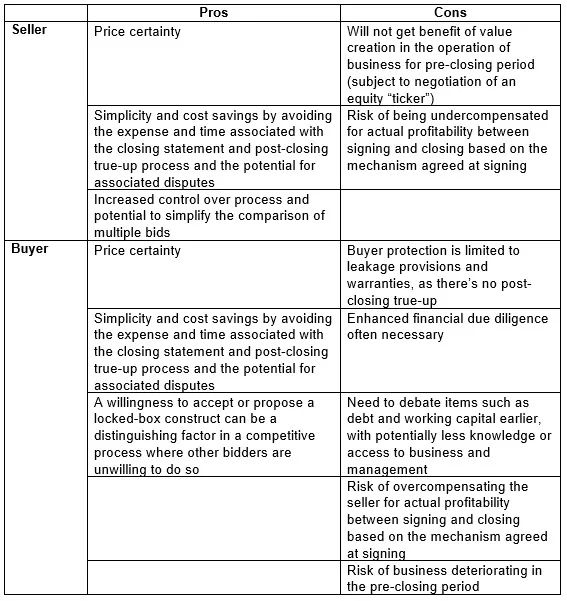

From the date of the locked-box accounts, known as the "locked-box date," the target company is essentially considered to be run for the benefit of the buyer – at least from a financial risk point of view – and no value, or "leakage," is allowed to leave the business for the benefit of the seller. The box is therefore "locked." Provided the box stays locked (more on this below), the SPA would not include any adjustment to the purchase price, and there would be no post-closing true-up. This is a key feature of the "locked-box" mechanism: The financial risk and benefit in the target pass to the buyer at the locked-box date.

To provide the buyer with comfort that there has been no value extraction by the seller or any persons connected with the seller since the locked-box date (i.e., the box has remained locked), the SPA will usually include protection for the buyer in the form of a "no leakage" dollar-for-dollar indemnity. In practice, the seller confirms that there will be no leakage from the business in the period from the locked-box date up to the date on which the closing occurs by including a no-leakage covenant in the SPA (that could also be backed up by warranties), which may be subject to certain exceptions in the SPA as agreed to by the parties, referred to as "permitted leakage." In transactions where there is a gap between signing and closing, sellers also typically agree to additional protections for the buyer in the form of restrictions in its conduct of the business during the pre-closing period, such as requiring the buyer's consent before agreeing to large long-term contracts, purchasing large fixed assets, etc.

In compensation for running the business between the locked-box date and the date of closing for the economic benefit of the buyer, the seller may sometimes seek an upward adjustment to the consideration for this "value accrual." In practice, the cash flow generated by the target company in the period between the locked-box date and closing is often taken as the basis for determining the value accrual. An alternative approach is an interest-based value accrual applied to the equity value using an agreed rate of return to the seller for the period up to the closing date – this is sometimes referred to as a "ticking fee." The rationale for these upward adjustments is that the buyer is benefiting from any profit earned during the locked-box period without bearing the cost of servicing the acquisition costs. To the extent the parties consider any adjustments for value accrual or ticking fees – and we see this less where the target is a loss-incurring business – the adjustments tend to be heavily negotiated.

When is a locked-box approach to the purchase price appropriate?

Depending on the situation, using a locked-box approach to a purchase price may or may not be appropriate.

- Stand-alone business: A locked-box mechanism is more appropriate when the target is a stand-alone business in terms of having separate accounting records with a history of reliable financial information, including where the target is a group of companies (i.e., there is a suitable box to lock). It is less likely to be appropriate for a seller with multiple businesses that are being split (e.g., a corporate carve out or restructuring) or with numerous affiliate transactions due to the increased risk of leakage.

- Seasonal business: A locked-box approach is less appropriate for a target business that is subject to significant seasonality or a business with uncertain short-term financial performance that makes pricing in the seller's compensation for operating the business during the pre-closing period challenging.

- Declining business performance: From a buyer's perspective, a locked-box mechanism is less appropriate if there is a risk that the target business performance will likely deteriorate in the pre-closing period.

- Long gap between signing and closing: A locked-box mechanism is less appropriate if there is expected to be a long gap between signing and closing.

Issues to consider

Locked-box accounts

The integrity of the locked-box accounts is critical. From the buyer's perspective, audited accounts will provide more comfort that a third party (the auditor) has reviewed and given an opinion on the quality of those accounts. In all cases, the buyer will need to conduct additional financial due diligence on the locked-box accounts to ensure that it and its advisers are comfortable with the basis of the preparation and accuracy of such accounts. In that regard, if the time or opportunity to conduct financial diligence is limited for any reason, the locked-box account approach may not be appropriate for the buyer.

Defining leakage and permitted leakage

The SPA will contain detailed definitions of "leakage" and "permitted leakage." These terms are a key area of negotiation, as they constitute the buyer's principal protection against the seller and any persons connected with the seller stripping value from the target, and they provide the contractual basis on which the seller will be able to make ordinary course payments – the permitted leakage – between the locked-box date and closing.

Typically, leakage is defined to cover any transfer of value from the target to the seller (or its affiliates) between the locked-box date and closing. This may include items such as dividends and distributions; returns of capital; transaction expenses; payments to directors; deal-related bonuses and other non-ordinary course intra-group payments. Permitted leakage will depend on the nature of the target business, but usually includes intra-group payments in the ordinary course of business and on arm's-length terms; identified items agreed between the parties and factored into the purchase price (e.g., dividend strip/monitoring fee); payment of salaries in the ordinary course of business; and debt breakage costs, such as bonds being taken out.

Funding issues

Third-party bank debt, intra-group debt and cash balances in the target business will vary through closing, as they reflect, among other factors, trading in the target business, interest accruals and payments, loan repayments, and additional borrowings. Although the actual levels of cash and debt in the business at closing are irrelevant from a valuation perspective in a locked-box mechanism, the seller will not be responsible for funding cash and debt requirements after the locked-box date. The buyer will need to fund the target business to enable it to repay existing intra-group debt payables at closing and may need to fund repayment of bank debt, depending on change of control issues and its own financing structure. The business also will need to maintain sufficient cash to be able to carry on its business. These issues mean that it will be important for a buyer – in particular, a private equity or other financial buyer using a leveraged finance acquisition structure – to understand the expected cash and debt movements and forecast funding requirements for closing, so it can properly structure its funding arrangements at closing.

Tax protections

Sellers are unlikely to offer any specific tax protection for the tax consequences of the business operations after the locked-box date. Complex issues arise regarding the interaction between any tax protections (e.g., a tax covenant) and the locked-box pricing mechanism, which will require detailed discussions with the seller's advisers.

Advantages and disadvantages of a locked-box construct

From the perspective of the seller and the buyer, there are a number of value and process-related advantages and disadvantages to the locked-box mechanism.

Is the locked-box construct the way to go for sellers?

On balance, the locked-box construct is sometimes thought of as a seller-friendly option, given the greater value certainty it delivers, although the seller risks losing the benefit of the anticipated growth of the business through closing unless it is captured in the headline price or otherwise. While there is some truth to that idea, the full picture is more complex, and use of a locked-box construct may be beneficial to the buyer and the seller, with the right set of facts and circumstances – and if they have appropriate advisers to help navigate the process. Private equity bidders on both sides of the pond tend to be comfortable with the locked-box mechanism, and we continue to see cross-border private equity deals conducted on this basis. We haven't yet seen the same uptake in strategic acquisitions and – given the slower pace of deals in 2022 and the more cautious approach taken by strategic acquirers, particularly public companies – moving away from the comfort of a full post-closing adjustment may take some time.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.