The defense profit pool was relatively insulated from COVID-related topline deterioration and profit erosion that acutely impacted the commercial aerospace sector. This resilience helped sustain strong sector revenue growth from 2017-2021. Industry profit growth, meanwhile, was dented by program execution challenges for large players, and defense players will need to navigate a shifting market environment to deliver on high profit growth expectations going forward.

Handful of U.S. Prime Contractors Account for Most of the Defense Profit Pool

Over the past five years, defense industry topline growth outpaced profit growth (7% versus 3%) as the industry experienced margin degradation, driven primarily by program execution challenges for select large players.

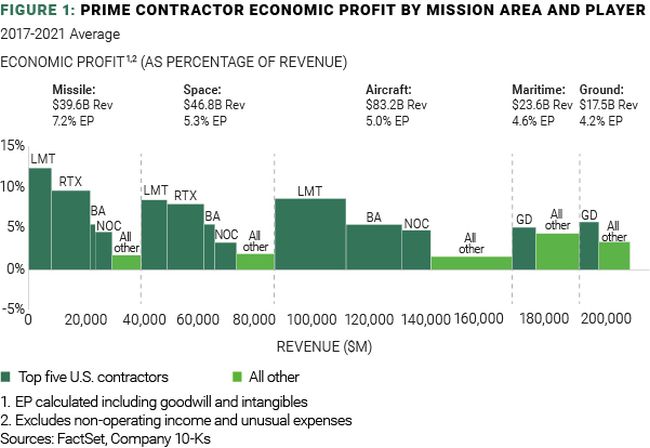

During the same period, five U.S.-based prime contractors (Boeing, General Dynamics, Lockheed Martin, Northrop Grumman and Raytheon Technologies), accounted for substantial defense market revenue and economic profits. This is especially pronounced across the aircraft, space, and missile segments – with prime contractors pulling in approximately 35% of total defense market revenue and 60% of profit. However, average profit margins for the group declined around 1% over this period, similar to the rest of the industry.

Challenging Industry Outlook

Looking to the next five years, total market revenue CAGR is expected to decelerate from 7% to around 2-3% through 2025, driven by modest DoD budget increases of 1.5% per year from 2020-2025. Budget increases related to the Ukraine conflict have started to materialize in some countries, including Germany, but the final outlook is still uncertain and for now investors appear restrained on topline growth expectations until more countries approve budget increases.

Conversely, investors expect the defense industry to reverse the recent margin degradation trend and accelerate profit growth going forward, even while topline growth slows. Investors remain bullish on industry profit growth (6-7% CAGR). This expectation is driven by 1) margin expansion for the top five, and 2) a combination of topline and margin growth for the other prime contractors outside the top five as the U.S. DoD seeks to diversify its supplier base.

From an industry segment perspective, space and missile – the two most profitable segments historically – are forecast to generate roughly two-thirds of prime contractor economic profit growth from 2021-2025, driven by above industry-average topline growth and margin expansion.

And after margin declines of nearly 2.5% since 2017, the maritime systems segment is expected stabilize and expand margins by 0.7% by 2025.

The aircraft segment is the only segment forecast to experience a decrease in revenue, although modest margin improvements are expected to keep profit growth positive over the period.

Largest Players Under Pressure

Going forward, investors expect revenue growth for the top five U.S. prime contractors to decelerate from over 6% to roughly 2% driven by budget shifts and an effort by the U.S. DoD to spread spending across additional contractors. As a result, despite expectations for modest margin improvement, the top five's share of total market profits is expected to decline by 5-10 pts through 2025. However, performance is not expected to be evenly distributed across the prime contractors. Many market analysts forecast outsized growth for Boeing and Raytheon through improved execution and expansion of key programs.

Necessary Adjustments to Focus and Approach

Even if Ukraine-related budget approvals increase topline growth, prime contractors need to at least maintain – if not expand – margins going forward to exceed investors' economic profit growth expectations and outperform peers. This will require improved performance as prime contractor margins deteriorated over the past five years as the industry experienced robust growth.

Here are two major questions to consider:

How do large contractors maintain their competitive advantage and accelerate profit growth?

- Operational excellence: First, meticulous detail to program management and operational excellence are required to expand margins on existing programs and avoid program setbacks. This includes proactively identifying and managing supply chain risks, particularly on high-margin sustainment programs.

- Smart program choices: In addition, focused R&D investment in growth areas, either self-funded or bought through acquisition, can boost performance in growing areas (e.g., space & satellite, missile systems) where the company has a competitive advantage and right-to-win. Companies must avoid subscale diversification into segments where a competitive advantage is absent.

- Differentiation: Likely winners of margin improvement will smartly re-invest profits into capabilities that will differentiate them from mission area competitors. Bolt-on M&A, meanwhile, can expand scope and extend capabilities in advantaged segments. This could include, for instance, expansion into systems integration or software.

How do smaller contractors capitalize on expected contract reallocation?

- Focus on the core: First, start with a focus on winning additional business in profitable areas where there is existing presence and capabilities. This is more effective than waging the uphill battle of trying to enter new markets and win against established, scaled players. Focus on capability development, including focused R&D, supply chain, and operations, to ensure business can continue to execute as new contracts are won.

- Exploit niches: Second, develop a clear forecast of government spend and work to gain business in newer, less crowded portions of the market, such as, space & satellite, missile systems, or greenfield technologies.

- Partnerships: And, of course, reassess teaming arrangements and who they choose to co-develop solutions and offerings with for large future defense programs.

Conclusion

The defense industry's profit pool held strong amid COVID-related disruption and other turmoil, but uncertainty surrounds the industry's outlook. Policy shifts regarding defense budget allocation present both opportunities and challenges to industry players.

Interest rate increases, an inflationary environment, and potential future COVID-19 risks represent additional unknowns and potential challenges that defense companies will have to successfully navigate to positively influence profit growth trends. Ukraine-related budget increases represent a potential tailwind, but the medium- to long-term impact on defense budgets is still largely unknown.

To outperform amid challenging and volatile market dynamics, defense players need to employ focused growth efforts supported by strong program execution and operational performance. For prime contractors, managing costs and improving efficiency will be critical to driving profit growth. Smaller contractors should look to expand their presence in existing niches and ensure they deliver on new contracts.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.