On 22 November 2023, Chancellor Jeremy Hunt presented his Autumn Statement to Parliament and started making, in his words, the long-term decisions necessary to strengthen the economy and build a brighter future. Fueled by falling inflation and stabilised public finances, focus is now being applied to reducing debt, cutting tax and rewarding hard work.

Headlines included generous National Insurance Contribution (NIC) cuts for workers and the self-employed and the 'biggest permanent tax cut in modern British history for businesses'. Some other anticipated measures appear to be on hold ahead of a full Budget next Spring and an expected 2024 general election.

Below, we talk more about the Autumn Statement headlines and other measures announced. Please note that 'tax years' run to 5 April each year and that, for example, 2024/25 signifies the year to 5 April 2025.

CUTTING TAX AND REWARDING HARD WORK

For employees

In addition to income tax, all employees earning more than £12,570 a year pay Class 1 NICs. The main rate of Class 1 NICs will be cut from 12% to 10% from 6 January 2024. This will come into effect from January 2024 and, over a full year, the average worker on £35,400 will receive a NIC reduction of over £450. Workers earning more than £50,270 a year will receive a NIC reduction of £754.

The Class 1 NIC rate will remain at 2% for earnings above £50,270 a year.

Similarly, there are no changes to the rate of employer's Class 1 NICs, which remains at 13.8%.

For the self-employed

Self-employed individuals with profits of more than £12,570 a year pay two types of NIC: Class 2 and Class 4.

- Class 2 NICs have been at a flat rate sum of £179.40 a year (£3.45 a week) in 2023/24 but no one will be required to pay the charge from 6 April 2024.

- The main rate of Class 4 NICs will be cut from 9% to 8% from 6 April 2024. Class 4 NICs will continue to be calculated at 2% on profits over £50,270.

Taken together these changes will result in an average self-employed person with profits of £28,200 saving £336 in 2024/25.

Class 2 NICs currently provide the selfemployed with access to a range of state benefits, including the State Pension. From 6 April 2024, self-employed people with annual profits;

- Above £12,570 – will continue to receive access to the benefits.

- Between £6,725 and £12,570 - will continue to receive access to the benefits, via a National Insurance credit.

- Under £6,725 (or with losses) – will be able to continue to pay Class 2 NICs on a voluntary basis in order to maintain their access to state benefits. Class 2 NICs had been due to increase in 2024/25 but it seems that these will be maintained at the current £3.45 weekly level for those in this bracket.

STATE BENEFITS

The government will uprate all working age benefits for 2024/25 by the September 2023 Consumer Price Index (CPI) of 6.7% and will continue to protect pensioner incomes by maintaining the promised 'triple lock' and uprating the basic State Pension, new State Pension and Pension Credit standard minimum guarantee for 2024/25 in line with highest of the three possible measures, namely average earnings growth of 8.5%.

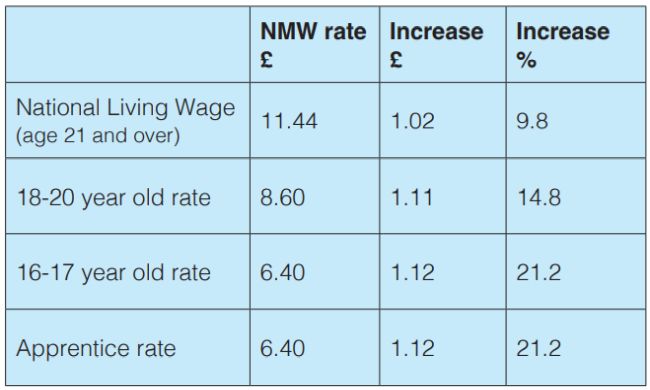

NATIONAL MINIMUM WAGE (NMW)

The biggest ever increase to the National Living Wage has been announced, with the government fully accepting the recommendations made by the Low Pay Commission. Eligibility for the National Living Wage will also be extended by reducing the age threshold to 21-year-olds for the first time. It was previously for those aged 23 and over only. From 1 April 2024 the minimum pay rates will be as follows:

BACKING BRITISH BUSINESS

Tax Relief for expenditure on plant and machinery

The Annual Investment Allowance (AIA) is now permanently set at £1million. This means that businesses can claim tax relief at 100% on up to £1million of expenditure on qualifying plant and machinery (e.g. capital equipment).

'Full expensing' is an additional and alternative relief for companies only. It allows unlimited 100% upfront tax relief on qualifying plant and machinery that is purchased in a new condition on or after 1 April 2023. There is also an associated 50% allowance for expenditure on certain types of plant and machinery that does not qualify for the full 100% (including space and water heating systems, for example).

This 'full expensing' regime was initially introduced in Spring 2023 and had an original end date of 31 March 2026. It has now been announced that it will be made permanently available. Described as the 'biggest business tax cut in modern British history' it must be noted that it will usually only benefit companies or groups of companies that have already utilised their £1million AIA. It is not available at all for unincorporated businesses, although the expansion of the cash-basis (see below) achieves a very similar effect for sole traders and partnerships.

Full expensing does come with some quite complicated rules on the amount of upfront relief and the calculation of tax charges that may apply when the purchased plant and machinery is sold. Please talk to us for more details.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.