Parametric insurance operates on a simple principle. Instead of compensating for direct losses incurred, it provides coverage for a predetermined amount, often scaled according to the severity of the event.

Hurricane Maria, a Category 5 hurricane, wreaked havoc in the northeastern Caribbean countries of Puerto Rico and Dominica in September 2017, causing massive destruction and leaving individuals and businesses in dire need of aid. However, their experiences with insurance and recovery were markedly different. Puerto Rico battled with prolonged insurance recovery efforts, unresolved claims, and legal disputes between insurers and policyholders, resulting in over $1.6 billion in unsettled insurance claims even more than two years after the hurricane. On the other hand, Dominica had a parametric insurance policy through the Caribbean Catastrophe Risk Insurance Facility (CCRIF), which allowed for a rapid payout of $19 million within just 14 days of the hurricane's impact. This comparison demonstrates how parametric insurance, also known as index insurance, can provide expedited, flexible, and transparent relief.

$1.6

billion in unsettled insurance claims even more than two years after the hurricane in Puerto Rico.

$19

million rapid parametric insurance payout within 14 days of hurricane's impact in Dominica.

Parametric insurance operates on a simple principle. Instead of compensating for the direct losses incurred, it provides coverage for a predetermined amount, often scaled according to the severity of the event. This approach bridges the gap where traditional insurance falls short, offering swift, transparent, and vital financial support to countries and regions grappling with the aftermath of natural disasters.

One key advantage of parametric insurance is the guaranteed payment amount.

One key advantage of parametric insurance is the guaranteed payment amount. This feature empowers individuals and businesses in disaster-prone areas to plan effectively, making it a valuable tool for aiding recovery efforts and facilitating a rapid rebound from significant losses. The recognition of this advantage by the insurance industry, government bodies, and other policyholders has spurred a surge in innovative parametric insurance products in the last decade.

Examples of Innovative and Successful Parametric Insurance Products

- When Hurricane Lisa passed over Belize's Turneffe Atoll as a Category 1 hurricane on 2 November 2022, the MAR Insurance Programme's parametric triggered a $175,000 payout to the Mesoamerican Reef Insurance Fund (MAR Fund) within just two weeks of the event. The funds were allocated for reef recovery and restoration efforts, aiding the crucial Mesoamerican Reef system.

- UNICEF and WTW collaborated to pioneer a parametric insurance policy that aims to protect vulnerable children in climate-vulnerable nations. This innovative initiative combines climate resilience investments and anticipatory action with a unique parametric insurance policy tailored to children's needs. By doing so, it aims to protect and respond rapidly to cyclone-related impacts, benefitting an estimated fifteen million vulnerable children.

Despite its evident advantages and successful applications, the adoption of parametric insurance remains relatively limited compared to indemnity insurance. For instance, Hurricane Ian devastated Florida in September 2022, causing a staggering $100 billion in losses, with only $60 billion covered by insurance. However, among the few known parametric insurance payouts related to Hurricane Ian, Arbol delivered a $10 million payout to property and casualty (P&C) company Centauri Insurance just weeks after the hurricane struck in late September.

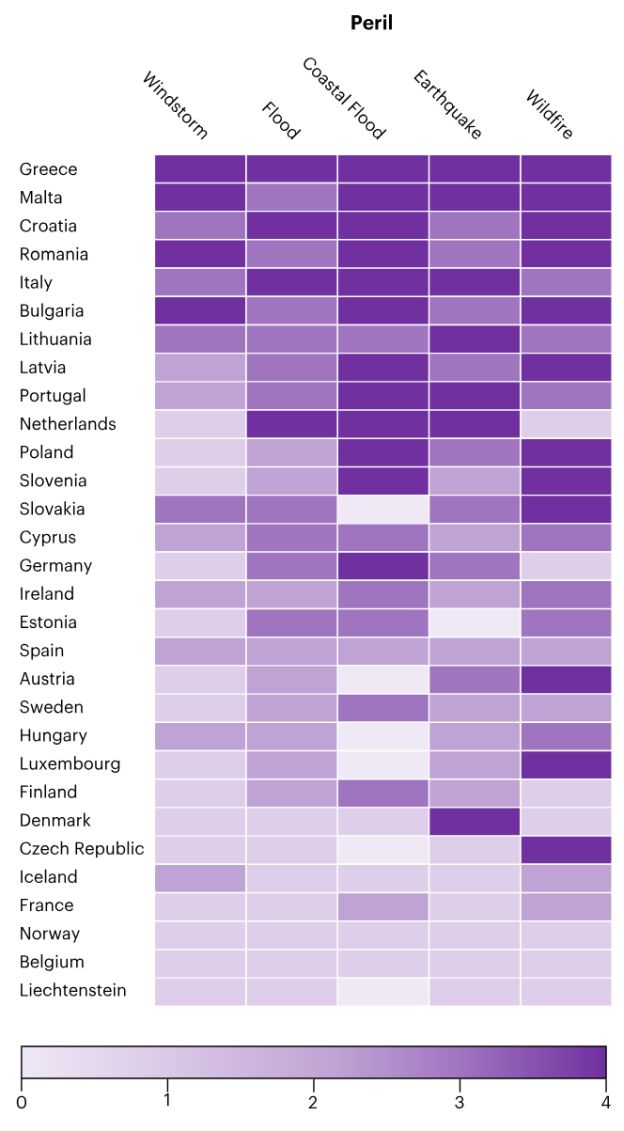

The graph below illustrates the level of insurance coverage for specific risks in various European countries, as measured by penetration scores ranging from 1 (low) to 4 (high). The low coverage rates can be attributed to factors such as a lack of financial literacy, distrust, credit constraints, pricing, and basis risk. However, among all the factors mentioned, basis risk stands out as a significant contributor to the low uptake of insurance coverage.

Insurance Penetration by Peril and Country

Basis Risk: A Double-Edged Sword

So, what exactly is basis risk? Essentially, basis risk refers to the possibility of a discrepancy between the actual losses incurred by a policyholder and the index used to determine the insurance payout, potentially disrupting the promissory exchange system that underlies private insurance transactions.

...basis risk refers to the possibility of a discrepancy between...actual losses incurred... and...index used to determine the insurance payout...

While parametric insurance products are designed to minimize basis risk by selecting a proxy that accurately captures the impacts experienced by the policyholder, there will always be some level of basis risk in any such product. This is equivalent to the small print and exclusions that may be found in an indemnity insurance policy, and lead to complaints if the policy holder is not aware of them when taking out the policy.

For example, a home insurance policy may cover fire damage but exclude earthquake-generated fire damage. So, while parametric insurance will provide a reliable payout when predefined conditions are met, there is a possibility that the payout may fall short of covering the actual costs of the event. This discrepancy could occur due to an a priori estimate of the cash requirement for an event of a specific magnitude or intensity, as reflected in the index used.

Moreover, potential missteps in the design of parametric insurance products could contribute to this risk. These missteps might involve not covering all aspects of the loss experienced, inaccuracies in selecting parameters or their values, disparities in index measurement locations compared to where the loss occurred, discrepancies in the timing of the considered loss event, or idiosyncratic factors affecting index design.

Negative & Positive Basis Risk

While the most commonly mentioned basis risk typically refers to the negative risk experienced by policyholders, it's essential to acknowledge that basis risk encompasses the discrepancy between the expected payment for a loss event, thus incorporating both positive and negative risk elements.

Negative basis risk occurs when coverage falls short of actual losses, leaving policyholders financially strained

Negative basis risk occurs when coverage falls short of actual losses, leaving policyholders financially strained. This mismatch can deter risk-averse individuals from finding parametric insurance attractive, as they may still face the risk of default and collateral losses. These individuals might perceive parametric insurance as an intricate and unpredictable lottery, eroding their trust in the insurance scheme.

Example of Negative Basis Risk

- In 2004, India introduced the Weather Based Crop Insurance Scheme (WBCIS) to safeguard farmers against unfavorable weather conditions such as deficient rainfall. However, a study conducted by Agricultural Finance Cooperation (AFC) in 2010 revealed that around 80% of the respondents were dissatisfied with the location of the weather station. The actual weather risk experienced by farmers in the vicinity often significantly differs from the data recorded at the weather station, which may not trigger a payout despite damage occurring on an individual farm.

... positive basis risk occurs when the payment exceeds the actual loss for the policyholder.

On the other hand, positive basis risk occurs when the payment exceeds the actual loss for the policyholder. In such situations, insurers face the challenge of overcompensation, requiring a capital cushion to absorb underpricing risk. Underpricing risk refers to charging insufficient premiums to cover potential claims, which can increase the risk of insolvency for insurance companies. To account for positive basis risk, insurers add ambiguity loads to premiums. However, in some cases, the level of risk ambiguity is too high for the insurance company to offer parametric insurance.

Examples of Positive Basis Risk

- In Sri Lanka, Oxfam worked with the insurance company SANASA to introduce a new scheme for rice farmers. Despite some short and sharp bursts of rain in 2016, most of Batticaloa experienced severe drought, severely damaging, or destroying the rice fields. Unfortunately, the amount of rainfall was higher than the minimum threshold required for a drought payout, which meant that 622 farmers who had subscribed to the Weather Index insurance program were not eligible for compensation. Oxfam worked closely with SANASA and negotiated a solution, resulting in the farmers getting ex gratia payments of LKR. 3,550,000 (US$ 24,359) from SANASA.

- In 2013/14, ACRE in Rwanda had a program to safeguard farmers' loans for a better seed and fertilizer package. However, the organization was compelled to offer ex gratia payouts, which ultimately resulted in one of the providers pulling out of the program.

Strategies for Mitigating Basis Risk

What strategies can be employed to reduce basis risk in parametric insurance? Mitigating basis risk in parametric insurance requires a multifaceted approach that incorporates various methods. One crucial strategy involves the careful selection of the parameter that represents the hazard which is responsible for causing damage. Additionally, it is necessary to determine appropriate trigger thresholds and devise a payout structure that scales the intensity of the parameter (and associated impacts). Additionally, incorporating multiple triggers or developing regional or localized triggers can be beneficial.

Mitigating basis risk in parametric insurance requires a multifaceted approach...

The use of multiple triggers results in varying payout depths, ensuring that policyholders receive smaller payouts at lower depths if they miss the primary trigger event. Likewise, triggers tailored to specific regions or locations, considering unique characteristics and risks, allow insurers to more precisely reflect the intensity of the risk event and provide accurate payouts.

Furthermore, advanced modeling techniques play a crucial role in reducing basis risk, even by marginal amounts, while also maintaining the simplicity of the actual triggers. Another potential solution closely linked to methodological advancements for mitigating basis risk involves improving the availability and accuracy of weather data.

... use of multiple triggers results in varying payout depths, ensuring that policyholders receive smaller payouts at lower depths...

Among data sources, the utilization of remote sensing or satellite data in parametric insurance mechanisms is on the rise and can be a valuable tool to ensure data availability.

Examples of Strategies:

- Insurers utilize the Hwind cumulative footprint to trigger parametric hurricane policies, reducing basis risk. Hwind is a system that aggregates observational data from over thirty sources, including satellite data, aircraft reconnaissance, buoys, and land-based anemometers, resulting in tens of thousands of individual measurements for each event. Typically, each snapshot reflects a six-hour data window before the valid snapshot time. By using Hwind as a trigger, insurers can accurately gauge the intensity of the risk event, providing precise payouts to policyholders.

- The CCRIF SPHERA model for tropical cyclones has introduced a new policy endorsement called the Localized Damage Index (LDI). This addition enables targeted coverage during tropical cyclone events, particularly when losses are concentrated in specific localized areas within a country. Additionally, the upgrade from the XSR 2.5 version to the improved XSR 3.0 version includes the introduction of the 'localized event trigger' (LET) to address extreme localized events.

- Flood Flash offers multi-trigger policies to enhance the flexibility and efficiency of flood insurance. Unlike traditional single-trigger policies, multi-trigger policies provide payouts at varying flood depths, addressing concerns about narrowly missing the trigger event. For example, a flood of 0.48m can trigger smaller payouts at 0.2m, 0.3m, and 0.4m, ensuring coverage even if the central trigger depth of 0.5m is not met.

- The R4 Rural Resilience Initiative provides insurance coverage for 20,000 impoverished farmers in Ethiopia and Senegal using satellite-based rainfall and vegetation data. Similarly, a portion of Agriculture and Climate Risk Enterprise (ACRE) products, which rely on satellite-derived rainfall estimates and satellite-based indices, have insured approximately 37,000 farmers in Rwanda.

- Descartes and Reask have partnered to provide AI-powered parametric cyclone insurance. This collaboration seeks to expand coverage to new areas by leveraging Reask's wind data and Descartes' expertise in integrating innovative technology into parametric insurance product design.

Addressing the Positive and Negative Basis Risk

When addressing basis risk mitigation in parametric insurance, it's essential to consider both dimensions: negative and positive basis risk, as they have significant implications for both policyholders and insurers.

Negative basis risk will result in customer dissatisfaction and reduced policy renewals. In contrast, positive basis risk can results in over-payouts, and higher long-term costs for policyholders due to a lack of cost efficiency in the product, rendering insurance unaffordable or financially unattractive.

While various strategies aim to mitigate overall basis risk, it's crucial to distinguish and address each dimension separately. What may work for one dimension may not be suitable for the other, and a one-size-fits-all approach may create more problems than solutions. Therefore, it's critical to identify and implement tailored strategies for each dimension of basis risk. A key way to achieve this is through working closely with those experiencing the risks. By doing so, we can gain valuable insights to select appropriate impact proxies, determine suitable thresholds, and refine modeling approaches. This inclusive approach enables customized strategies that cater to the diverse dimensions of basis risk, ultimately enhancing the relevance and effectiveness of risk mitigation efforts.

In conclusion, parametric insurance can be a game-changer in addressing disaster risk. However, effective basis risk management demands a sophisticated approach that addresses both negative and positive basis risk separately. Thus, it is needed to diagnose the specific issue at hand, understanding the unique challenges involved, and tailor strategies to suit the situation. A one-size-fits-all approach that focuses solely on reducing negative basis risk falls short of comprehensiveness. Instead, understanding the intricate factors that contribute to each type of basis risk is vital for developing tailored strategies that lead to a more robust and effective parametric insurance framework. This approach enhances risk management, promotes market acceptance, and facilitates expansion into new markets. Ultimately, reducing basis risk boosts confidence and improves the effectiveness of parametric insurance.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.