- within Wealth Management topic(s)

On 30 March 2023, the UK Government published an updated Green Finance Strategy (the "Strategy"). The Strategy, which updates the UK's 2019 Green Finance Strategy, outlines how "continued UK leadership on green finance will cement the UK's place at the forefront of this growing global market, and how we will mobilise the investment needed to meet our climate and nature objectives".

Objectives

The Strategy aims to deliver five key objectives to achieve the UK Government's goal of ensuring it is a world leader on green finance and investment:

- UK Financial Services Growth and Competitiveness – increase support to the UK's financial services sector to ensure the sector can prosper from a transitional global economy;

- Investment in the Green Economy – raise an additional £50-60 billion of private capital investment each year to help deliver net zero, build climate resilience and support nature's recovery;

- Financial Stability – produce an effective green finance framework to ensure the finance sector has the information needed to manage risks from climate change and nature loss;

- Incorporation of Nature and Adaptation – incorporate nature and climate into the UK Government's green finance policy framework; and

- Alignment of Global Financial Flows with Climate and Nature Objectives – support the alignment of global financial frameworks and stimulate investment towards emerging and developing markets where capital is needed.

Key themes

The Strategy discusses how the UK Government intends to achieve these objectives via three chapters: (1) Foundations; (2) Align; and (3) Invest. These chapters include a number of cross-cutting key themes:

Transition Finance and Transition Plans

The Strategy states that the UK Government will support the development of transition finance instruments that are consistent with the net zero pathway and the Paris Agreement goals. As part of this, the University of Oxford and the UK Centre for Greening Finance and Investment are developing a new Transition Centre of Excellence, which aims to become a provider of transition financial services and innovative instruments.

In addition, the UK Transition Plan Taskforce is expected to publish its Disclosure Framework and Implementation Guidance for Transition Plans in the summer of 2023, which aims to provide best practice for companies and investors seeking to disclose transition plans (for further information on the UK Transition Plan Taskforce, read our earlier blog post here). Once published, there will be a consultation on the introduction of transition plans for the UK's largest companies.

Sustainability Disclosure Requirements ("SDRs") and investment labels

The FCA announced a delay to the publication of its policy statement in response to its Sustainability Disclosure Requirements (SDR) and investment labels consultation (CP 22/20). The FCA has stated that it will publish the final policy statement in Q3 of 2023.

Once the policy statement is published, the Strategy states there will be a call for evidence aiming to ensure that the UK Government's legal framework delivers "decision-useful information in a cost effective, streamlined, and proportionate manner". The FCA also noted that, once developed, the UK Green Taxonomy (see below) could be aligned with the SDRs to ensure that in-scope assets meet a credible sustainability standard (for further information on the UK SDRs, read our earlier blog posts here and here).

UK Green Taxonomy

The Strategy reiterated the UK Government's intention to develop a UK Green Taxonomy. The UK Government has also proposed that nuclear – as a key technology within its pathways to reach net zero – will be included within the UK Green Taxonomy, subject to the outcome of a consultation.

The UK Government will continue to work through the Green Technical Advisory Group to develop the UK Green Taxonomy and will subsequently consult on the UK Green Taxonomy in the autumn of 2023. After the Taxonomy has been finalised, the UK Government will initially expect companies to report voluntarily against it for at least two years before the introduction of mandatory reporting obligations (for further information on the UK Green Taxonomy, read our earlier blog post here).

UK Non-Financial Reporting

The Strategy confirms that the UK Government will conduct a review of the UK's non-financial reporting, which will (among other things):

- consider the thresholds used to determine which companies must comply with reporting obligations under the Companies Act 2006;

- consider whether to incorporate mandatory non-financial reporting into UK company law;

- conduct a Call for Evidence on how the UK Government can support Scope 3 greenhouse gas emissions reporting, with the aim of improving understanding of the costs and benefits of producing and using emissions data;

- update the Environment Reporting Guidelines, including for Streamlined Energy and Carbon Reporting, with the hope that it will result in best practice guidance for gathering and reporting environmental data; and

- explore how to incorporate the Taskforce on Nature-related Financial Disclosure framework into UK policy (for further information on the TNFD, read our earlier blog post here).

ESG Ratings and Benchmarks

HM Treasury has also published a consultation on a future regulatory regime for ESG rating providers. The consultation proposes that UK and non-UK based ESG ratings providers who provide ESG ratings to users in the UK should be brought under the FCA's regulatory remit, with the hope that this would "improve the transparency of methodologies, governance, and processes of ESG ratings providers". In particular, HM Treasury anticipate that any requirements for ESG ratings providers would be based on the International Organization of Securities Commissions' recommendations for securities markets regulators. The deadline for responses to the consultation is 30 June 2023 (for further information on ESG ratings, read our earlier blog post here).

International Sustainability Standards Board ("ISSB") Standards

The UK Government intends to launch a formal assessment mechanism to determine whether the ISSB Standards are suitable for UK companies as soon as the final ISSB Standards are published, which is expected in June 2023 (for further information on the ISSB Standards, read our earlier blog posts here, here and here).

Carbon and Nature Markets

The Strategy states that HM Treasury will consider measures to help ensure that the Voluntary Carbon Markets ("VCM") can reach their potential. In particular, HM Treasury will consider upcoming guidance from the Voluntary Carbon Markets Initiative and the Integrity Council on Voluntary Carbon Markets (for further information on the VCMI and ICVCM, read our earlier blog post here). It is hoped that by considering this guidance, HM Treasury can provide clarity on what constitutes good quality credits and how the VCMs can be regulated to solidify such quality.

HM Treasury also intends to pilot new nature markets, including via its Natural Environment Investment Readiness Fund, which is a fund that supports the development of nature projects across England to generate revenue from nature markets and operate on repayable private sector investment. Further details are set out in the UK Government's Nature markets: a framework for scaling up private investment in nature recovery and sustainable farming publication.

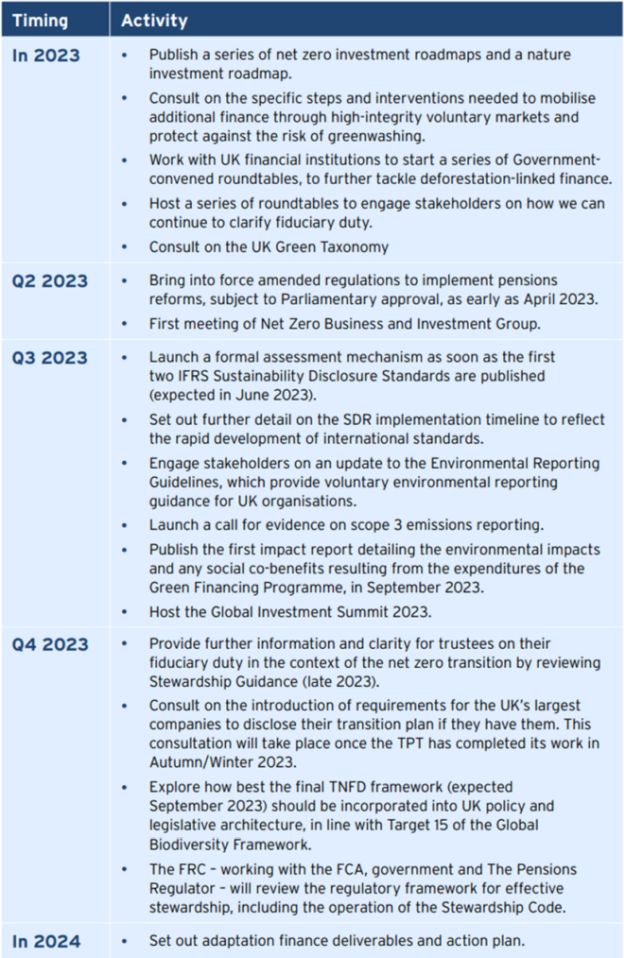

Next steps

The Strategy includes the following table, which shows the commitments of the UK Government over the next year:

Originally published 31 March, 2023

Visit us at mayerbrown.com

Mayer Brown is a global services provider comprising associated legal practices that are separate entities, including Mayer Brown LLP (Illinois, USA), Mayer Brown International LLP (England & Wales), Mayer Brown (a Hong Kong partnership) and Tauil & Chequer Advogados (a Brazilian law partnership) and non-legal service providers, which provide consultancy services (collectively, the "Mayer Brown Practices"). The Mayer Brown Practices are established in various jurisdictions and may be a legal person or a partnership. PK Wong & Nair LLC ("PKWN") is the constituent Singapore law practice of our licensed joint law venture in Singapore, Mayer Brown PK Wong & Nair Pte. Ltd. Details of the individual Mayer Brown Practices and PKWN can be found in the Legal Notices section of our website. "Mayer Brown" and the Mayer Brown logo are the trademarks of Mayer Brown.

© Copyright 2023. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.