In This Issue:

Accounting In Difficult Times

IFRS

Distributions Of Non-Cash Assets 2009 – A Year Of Change

Share-Based Payments

UK GAAP

Related Party Disclosures

Financial Reporting Round-Up

On The Horizon

The response to the global economic crisis has been wide ranging, including from those responsible for setting accounting standards. We look at developments in international and UK accounting standards, and focus on some of the accounting consequences of the turmoil in financial markets.

ACCOUNTING IN DIFFICULT TIMES

Whether reporting under IFRS or UK GAAP, many companies will be having to consider the implications of the global financial crisis. We examine some of the financial reporting consequences, both in respect of new standards and guidance and applying existing standards.

The Financial Instruments Challenge

While the initial shockwaves of the credit crisis may have faded, the ensuing economic downturn continues to pose problems for standard setters and preparers alike.

With financial instruments being subject to measurement at fair value under IFRS and users now being much more aware of the risks associated with some types of instrument, it is not surprising that this is the area that has seen the most direct response from standard setters. This is both in respect of changes to accounting standards and additional guidance, albeit primarily aimed at financial institutions.

Reclassification Of Financial Assets: Amendments To IAS 39, IFRS 7 And IFRIC 9

In late 2008 the International Accounting Standards Board (IASB) came under pressure to issue an amendment to IAS 39 'Financial Instruments: Measurement' that would permit the reclassification of some financial assets from fair value to cost categories in line with reclassifications which were already being allowed under US GAAP.

In October 2008, the IASB issued the amendments, citing their desire to create a 'level playing field' with the US. In recognition of the urgency of the issues, the amendments were issued without the usual due process and were subsequently endorsed by the European Commission (EC) in record time. However, later in the same month as a response to questions about the application date, the IASB was forced to issue clarifying guidance regarding the effective date and the transitional provisions. In March 2009 they then issued further amendments to IAS 39 and to IFRIC 9 'Reassessment of Embedded Derivatives'. This was to clarify the accounting treatment of embedded derivatives relating to financial assets reclassified in accordance with the original amendment.

Equivalent amendments have also been made by the Accounting Standards Board (ASB) to FRS 26.

Which Instruments Can Be Reclassified?

Non-derivative financial assets classified as held for trading (but not those voluntarily designated as at fair value through profit and loss under the fair value option) may be reclassified in two situations only.

- A financial asset meeting the definition of a loan or receivable at the date of reclassification, if the reporting entity now has the intent and ability to hold it for the foreseeable future or to maturity.

- In 'rare circumstances' other financial assets classified as held for trading not meeting the definition of a loan or receivable can also be reclassified. According to the press release accompanying the amendments, the deterioration of the world's financial markets in the third quarter of 2008 was a possible example of such 'rare' circumstances.

Companies may also reclassify available for sale assets to loans and receivables provided the asset meets the definition of a loan or receivable at the date of reclassification and the company now has the intent and ability to hold it for the foreseeable future or to maturity.

IFRS 7 has also been amended to incorporate extensive disclosure requirements relating to any assets reclassified as a result of this amendment.

How Are The Reclassified Assets Accounted For?

At the date of reclassification, the financial asset must be remeasured to fair value which then becomes its new cost or amortised cost, as applicable. Any subsequent increases in future cash receipts as a result of increased recoverability will be spread over the life of the instrument.

Application Date

The amendments to IAS 39 and IFRS 7 are effective from 1 July 2008 and reclassification cannot be made prior to this date. Any reclassification made in periods beginning on or after 1 November 2008 takes effect only from the date reclassification is made. However, any reclassifications made in periods beginning before 1 November 2008 can be deemed to have taken place at any date between 1 July 2008 and the end of the accounting period in question. The amendments to IFRIC 9 apply retrospectively for annual periods ending on or after 30 June 2009.

|

Smith & Williamson Commentary While the amendments received much publicity, they were aimed primarily at banks and other financial institutions. With many other financial instruments, including all derivatives, still being measured at fair value, volatility as a consequence of uncertain market-based measures is set to continue. |

Additional Disclosure Requirements

A further amendment to IFRS 7 'Financial instruments: disclosure' and its UK equivalent, FRS 29 requires enhanced disclosure about fair value measurements and reinforces the existing disclosure requirements in respect of liquidity risk.

Measuring Fair Value

Fair values are, in many cases, dependent on market values. The apparent instability and illiquidity of markets has caused some to question whether such bases are still relevant. By way of response, the IASB published educational guidance in October 2008 which is available on their website (www.iasb.co.uk/financial crisis) along with detailed information about all their activities relating to the credit crisis. While the guidance does not have the force of an accounting standard it is a useful summary of matters to consider.

IAS 39 'Financial instruments: measurement' and its UK equivalent FRS 26 require that where financial assets are measured at fair value, if there is a quoted price for the instrument in an active market, then it is that price that should be used to determine fair value. Both standards state that such a situation exists where quoted prices are readily and regularly available and they go on to clarify that fair value is not what would be paid in a forced transaction, liquidation or distressed sale. The question that has arisen therefore is whether instability in markets means that fair values are no longer readily observable.

While each case needs to be considered in the light of individual circumstances, the IASB guidance explains that the term active market does not mean that there needs to be a consistent number of transactions from one period to the next. A significantly reduced level of transactions does not necessarily mean that a market is not active. Neither does an imbalance between seller and buyers (more sellers than buyers) mean that a forced sale situation exists. As such, use of market-based prices may well still be appropriate. Indicators of a forced sale might include:

- a legal requirement to sell

- a need for immediate disposal of an asset without time to market it

- the existence of a single buyer as a result of legal or time restrictions (for example some of the recent bank 'bailout' arrangements).

Going Concern And Impairment

For many the applicability of the going concern basis may be more sensitive to assumptions than at any time in the recent past. The Financial Reporting Council (FRC) has issued updated guidance for the directors of listed companies and also separately for the directors of small companies. Both sets of guidance are available on the FRC website (www. frc.org.uk/publications) and although primarily aimed at specific audiences there is much of relevance to any company of any size.

Among the matters discussed, it is the basis of cashflow projections that are likely to be most significant for many preparers. Future cashflow projections are key to the going concern assumption and, now more than ever, there is a need for the projections to be realistic but, more importantly, sensitivity analysis has become a vital part of the considerations of many directors. While each company's position will be unique, questions to ask may include the following.

- What would happen if a major customer was lost?

- What if suppliers started to offer less credit and customers take longer to pay?

- What if interest rates increase?

Both UK GAAP and IFRS also require companies to review assets for impairment whenever there is an indicator that it may exist. IFRS also requires at least an annual review of the carrying value of goodwill. While the economic downturn is not in itself an indicator of the existence of impairment, it does contribute to the probability that other indicators are present.

Whether applying UK GAAP or IFRS, impairment will most probably be measured by reference to value in use, requiring the preparation of detailed cashflow projections. Similar considerations apply to those in respect of demonstrating the applicability of the going concern basis – the projections need to be as realistic as possible when predicting the underlying performance of the relevant business. Unfortunately, for many the past is unlikely to be an indicator of what is to come in the future.

Getting The Disclosure Right

The balance between meeting the disclosure requirements in legislation and accounting standards, and not providing more information than necessary about the financial position of a business has always been a difficult thing to achieve. The requirements of the Companies Act for a 'fair and balanced' review of the performance of a company mean that it is unlikely, in the current environment, that what was said last year will be appropriate this year. Thought also needs to be given to which key performance indicators are currently relevant – again these may well have changed since last year. Principal risks and uncertainties will come into sharper focus. It should, however, be remembered that the directors' report also provides an opportunity to explain further material figures in the financial statements – for example impairment and other provisions.

|

Smith & Williamson Commentary The requirements in the Companies Act apply to all but the smallest of companies and directors will need to revisit their reports to ensure they are appropriate. |

IFRS

DISTRIBUTIONS OF NON-CASH ASSETS

The distribution of non-cash assets takes many forms and clarity surrounding the accounting treatment was urgently needed.

It is not unusual for companies to make distributions of non-cash assets to shareholders. Such distributions can take many forms ranging from arrangements to demerge businesses, to agreements to offer a non-cash alternative for a cash dividend. However, accounting standards did not deal with how to treat such distributions and significant diversity had arisen in practice, with many preparers accounting for non-cash distributions at the book value of the asset. To address the issue, in late 2008 the International Financial Reporting Interpretations Committee (IFRIC) issued a new interpretation: IFRIC 17 'Distributions of Non-cash Assets to Owners'.

IFRIC 17 concludes that all distributions of non-cash assets should be recognised at the fair value of the assets given up. When the non-cash asset surrendered has a carrying amount which is lower than the fair value then the difference will need to be credited to the income statement at the point when the distribution is settled and the non-cash asset is derecognised.

However, there is a potential complexity for UK preparers where the dividend is approved by shareholders in one period but settled in a subsequent period. In the UK once a final dividend is approved by shareholders, a liability must be recognised. IFRIC 17 requires that this liability should be recognised at the fair value of the non-cash asset given up.

Therefore, some companies could find themselves in the position of recognising a liability to make a distribution at fair value in a different period to that in which they recognise the related gain on the asset to be distributed.

Entities must apply IFRIC 17 prospectively for periods beginning on or after 1 July 2009, earlier application is allowed provided that revised IFRS 3 and IAS 27 are also adopted at the same time.

|

Smith & Williamson Commentary It is vital that IFRS results in reasonably consistent accounting approaches across different countries and industries, and the IFRIC has addressed an area where divergent accounting practices were apparently starting to develop. However, many preparers and users may struggle to understand the concept of recognising an income statement gain when assets are given up, a position that is exacerbated by the potential complication referred to above which splits distribution and gain across two periods. Careful planning may therefore be needed to ensure sufficient distributable profits exist to cover such distributions. |

2009 – A YEAR OF CHANGE

With many companies around the world adopting IFRS for the first time in 2005, the IASB recognised that there was a need for a period of stability before any new standards were introduced.

While development of both new standards and amendments to existing standards continued, in 2006 the IASB announced that none would have mandatory application dates before 1 January 2009. Although it seemed a long way into the future, now it is here and preparers of financial statements find themselves facing a significant level of change.

Most of the standards have been covered in previous editions of the Financial Reporting newsletter, but here we provide a brief summary of the changes that are likely to be of most significance. Unless otherwise noted, all of the new and amended standards apply for periods beginning on or after 1 January 2009.

All Change For Primary Statements

As discussed in Financial reporting October 2008 newsletter, the primary statements are now as follows.

- Statement of financial position (previously the balance sheet). Use of the new name is not mandatory, but it is the term that is now being used in all new standards.

- Statement of comprehensive income (a combination of the income statement and statement of recognised income and expense (SORIE)).

- Statement of cashflows (previously the cashflow statement).

- Statement of changes in equity.

The format of the statement of financial position and statement of cashflows remain unchanged, but the statement of comprehensive income is different, particularly for those who did not previously present a SORIE. The statement of comprehensive income combines both profit and loss items and items of 'other comprehensive income' such as revaluations and foreign exchange. There is a choice of presenting either one statement or two consecutive statements – one showing profit and loss items and one recording other comprehensive income.

In certain circumstances, it will be necessary to disclose a third statement of financial position at the beginning of the comparative period – namely where there is retrospective application of a new standard or retrospective restatement or reclassification of previously recorded items.

A New Approach To Business Combinations And Accounting For Minority Interests

The revised versions of IFRS 3 'Business combinations' and IAS 27 'Consolidated and separate financial statements' apply for periods beginning on or after 1 July 2009, and re-write the accounting rules in a number of key areas.

- Acquisition costs such as legal and professional costs will need to be written off to income rather than included in the calculation of goodwill.

- Contingent consideration should be measured at fair value at the date of acquisition and subsequent revisions to the estimate of fair value will in most circumstances be reported in the income statement rather than as adjustments to goodwill.

- Intangible assets include non-contractual customer relationships.

- Minority interests are re-named non-controlling interests and on acquisition may be measured either at fair value or as a proportionate share of net assets.

- Acquisition accounting is only applied once – at the date control passes. Subsequent changes in non-controlling interests are accounted for within equity.

The revised standards were covered in more detail in the spring 2008 Financial reporting newsletter.

A Management Approach To Segmental Reporting

IFRS 8 'Operating segments' moves away from the existing model for segmental reporting to one which requires disclosure by reference to the information used by 'the chief operating decision maker' (CODM) when monitoring the company's performance. The CODM does not have to be one person and if, as is often the case, key decisions are made by the board of directors, the board will collectively be the CODM.

General disclosure is required of the factors used to identify the entity's reportable segments and the types of products and services from which each segment derives its revenue. For each reportable segment, disclosure is required of profit or loss and total assets. The focus on information used by management means that the numbers may not be IFRS based figures at all and a reconciliation of each material item to the entity's reported figures is therefore also required.

There are also certain entity wide disclosures that need to be made in respect of revenue and non-current assets. The most challenging of these is likely to be that relating to reliance on major customers – while the customer or customers do not have to be named this is still likely to prove a sensitive disclosure for many.

Other Changes

- The option in IAS 23 to expense borrowing costs is removed, with capitalisation being required in all relevant cases.

- IAS 38 'Intangible assets' is amended to clarify that expenditure incurred to provide future economic benefits but that does not give rise to an intangible or other asset, must be expensed as incurred. For example, the cost of a mail order catalogue will be expensed when the entity has access thereto (i.e. when it is printed).

- IAS 40 'Investment properties' now permits property under development or construction to be accounted for as investment property.

|

Smith & Williamson Commentary All reporting entities will be affected by at least one of the changes (IAS 1) and for many it will be more than one. In re-writing and amending the standards the IASB has also in some cases changed underlying principles of accounting that have been in place for many years. Coming to terms with such an unprecedented series of amendments will not be an easy task and, combined with the effects of the current economic crisis, could be a further burden on already stretched finance functions. Getting an early understanding of how the changes may impact and seeking professional advice where necessary will be key to a smooth financial reporting season. |

MORE CHANGES FOR SHARE-BASED PAYMENT ACCOUNTING

Accounting for share-based payments is one of the more complex areas of financial reporting and in providing clarification on certain provisions of IFRS 2, the IASB has created further challenges for many who make use of such arrangements.

The IASB published an amendment to IFRS 2 'Share-based payments' in January last year that comes into effect for periods beginning on or after 1 January 2009. Unlike most amendments however it has retrospective application and those with share-based payment arrangements need to consider carefully its possible implications. The ASB has made an equivalent amendment to FRS 20.

The amendment seeks to address inconsistencies that have resulted from the differing treatments adopted by preparers in accounting for share-based payment arrangements that include a condition in the original terms of the award which is neither a service condition nor a performance condition. For example, the requirement for an employee to contribute a monthly deduction from his/her salary under a Save As You Earn (SAYE) scheme.

The original wording of IFRS 2 defined vesting conditions as including service conditions and performance conditions. The standard was silent as to whether other conditions could fall within this definition. The amendment clarifies that vesting conditions comprise only service conditions and performance conditions (the latter might be either market or non-market based conditions). It is these conditions that determine whether or not the company receives the services that entitle the counterparty (for example the employee in an employee share-based payment arrangement) to receive the award.

The amendment also introduces a new term – non-vesting conditions. Non-vesting conditions are defined as being other conditions which must be satisfied for the counterparty to be entitled to the award. Examples include the requirement for the company to keep the plan open, non-compete provisions or transfer restrictions that apply after vesting. Most significantly, the requirement for an employee to save during the vesting period (such as in a SAYE scheme) is a nonvesting condition. It is this implication of the amendment which is likely to have the greatest impact on companies in the UK.

Non-vesting conditions are required to be treated in a similar way to market performance conditions when calculating the grant date fair value of the sharebased payment. Therefore, all non-vesting conditions need to be taken into account when valuing share-based payments under IFRS 2. It is important to note that when reflecting the non-vesting conditions in the fair value at grant date, the company should assume that the probability of its continuation of the plan is 100%, i.e. the fair value of the options should not be reduced to allow for the possibility that the company might withdraw from the plan before the options vest.

In contrast, when considering an arrangement such as a SAYE scheme, the grant date fair value must reflect an estimate of how many employees will stop saving and hence give up their options before they vest. This is a separate assessment from any estimate regarding employee turnover.

Where the options granted do not vest because of a failure to meet a non-vesting condition, the accounting treatment depends on whether the failure was within the control of the company or the counterparty, or whether it was outside the control of either party.

A failure to satisfy a non-vesting condition that is within the control of either the company or the counterparty is accounted for as a cancellation. This means that the part of the cost in respect of the shares or options which has not yet been recognised is accelerated and recognised immediately. So, for example, the accounting treatment of options which fail to vest because the employee withdraws from the scheme by stopping their monthly SAYE contributions, is consistent with that required in the situation where the company cancels the scheme.

Failure to satisfy a non-vesting condition that is beyond the control of either party, such as the performance of an external financial index that is not related to the company's share price, does not give rise to a cancellation. Instead the treatment is similar to that required when there is failure to meet a market performance condition i.e. the grant date fair value continues to be spread over the vesting period.

There are two areas which need to be considered on adoption of the amendments.

- The fair value of options awarded in the past may need to be revised to reflect the effect of non-vesting conditions in the grant date fair value.

- The accounting treatment of options which have not vested in the past as a result of a failure (either by the company or the counterparty) of a non-vesting condition will need to be revisited to ensure the treatment is compliant with IFRS 2 amended.

Any adjustment required to the IFRS 2 expense, recognised in previous years as a result of these two situations, will need to be accounted for as a prior year adjustment.

|

Smith & Williamson Commentary Given the amendments are retrospective, there is probably little to be gained from not adopting the revised standard early. Companies that prepare their accounts in accordance with IFRS as endorsed in the EU can also start using the amended standard immediately as the amendments were endorsed by the EC in December 2008. The amendments will be of particular importance to companies offering SAYE schemes to their employees. Given the current economic downturn more employees may decide not to continue to participate, stop their monthly contributions and opt instead to keep the cash. Under the amended standard this will trigger an acceleration of their share-based payment expense and has the potential to impact reported profits significantly for companies with a large workforce. In addition, certain conditions that were previously regarded as vesting may now be non-vesting requiring the valuation of the share-based payment to be re-visited. Valuation of such conditions may not however be straightforward. |

UK GAAP

INCREASING THE DISCLOSURE OF RELATED PARTY TRANSACTIONS

The ASB has recently issued a revised version of FRS 8 – Related party disclosures.

Although at first glance the changes arising from the revisions to the standard appear trivial, upon further consideration it is apparent that the changes to the exemptions available to preparers of financial statements are potentially significant in respect of companies that are parts of a group.

The revisions arise as a consequence of changes in European law that have been incorporated in the Companies Act 2006. The legal changes result in a definition of related parties in company law, the same as that used in IAS 24, the international standard on related party disclosures. Although the ASB is ultimately planning to replace FRS 8 with a new related party standard which is consistent with IAS 24, they have been delayed as the IASB is currently revising IAS 24.

The changes will affect parent companies as the unrevised version of FRS 8 provided an exemption from parent companies making separate disclosure of related party transactions when, as is usual in the UK, the individual financial statements of the parent were being presented alongside consolidated financial statements. This exemption is no longer available and as a result parent companies will now have to disclose all related party transactions other than those with their 100% owned subsidiaries.

The exemptions relating to the individual financial statements of subsidiary undertakings have also changed. The unrevised version of FRS 8 provided an exemption from subsidiary undertakings disclosing related party transactions with other members of the group provided that the reporting subsidiary was 90% or more controlled by the group. This exemption has been removed and replaced with a far more restrictive exemption which only excuses subsidiaries from disclosing related party transactions with other members of the group, where both the reporting subsidiary and any subsidiaries transacted with are 100% owned within the group.

The revised version of FRS 8 must be applied for accounting periods beginning on or after 6 April 2008. Earlier application is not permitted. In the first year of application a limited exemption from providing corresponding amounts is available for the financial statements of subsidiaries in certain circumstances.

|

Smith & Williamson Commentary While the changes to FRS 8 may initially appear to be limited, the potential effect on the disclosure required by members of a group is significant. The application of the new more restricted exemptions from disclosure can be complicated and care will be needed to ensure that all the required disclosures are included in the individual financial statements of the parent and its subsidiaries. |

FINANCIAL REPORTING ROUND-UP

We consider IFRIC interpretation 18, the impact of the IFRS improvements project discussed in our autumn 2008 newsletter on UK accounting standards as well as the final changes coming into force under the Companies Act 2006.

IFRIC 18 'Transfers Of Assets From Customers'

IFRIC 18 provides clarification of the requirements under IFRS for agreements in which an entity receives an item of property, plant or equipment that must then be used for the supply of goods or services. Alternatively, in some circumstances, the entity may receive cash from the customer to use in acquiring or constructing an item of property, plant or equipment in order to supply the goods or services.

The key areas dealt with in the interpretation include revenue recognition, asset recognition and measurement, identification of separately identifiable services and accounting for transfers of cash from customers. While most likely to be applicable in the utilities industry e.g. water, gas, electricity, the principles could also be relevant in certain circumstances for other entities. The interpretation applies to the transfer of assets received on or after 1 July 2009.

Improvements To Financial Reporting Standards

A number of amendments recently issued by the ASB mainly reflect the changes to IFRS based standards, as a result of the IASB's annual improvements project. The opportunity has also been taken to make some minor editorial changes to UK standards. None of the amendments are of particular significance but for companies applying any of the following standards they should make themselves aware of the changes – the amendments are available on the ASB's website.

- FRS 7 – Fair values in acquisition accounting

- FRS 17 – Retirement benefits

- FRS 21 – Events after the balance sheet date

- FRS 24 – Financial reporting in hyperinflationary economies

- FRS 25 – Financial instruments – presentation

- FRS 26 – Financial instruments – recognition and measurement

- FRS 29 – Financial instruments – disclosures

While not all amendments have the same application date, none are mandatory if they occur earlier than periods beginning on or after 1 January 2009.

Companies Act 2006

The majority of the accounting and auditing provisions of the Companies Act 2006 come into effect for periods beginning on or after 6 April 2008.

These changes covered in our March 2008 newsletter include the following:

- new company and group size limits

- increased audit exemption thresholds

- reduction in filing deadlines

- removal of the exemption from preparing group accounts for medium-sized groups

- audit reports signed by the senior statutory auditor on behalf of the firm.

The final tranche of changes resulting from the Companies Act 2006 will come into effect from 1 October 2009. These changes relate to a company's share capital; removing the requirement for there to be authorised share capital and also further restricting the use of the share premium account.

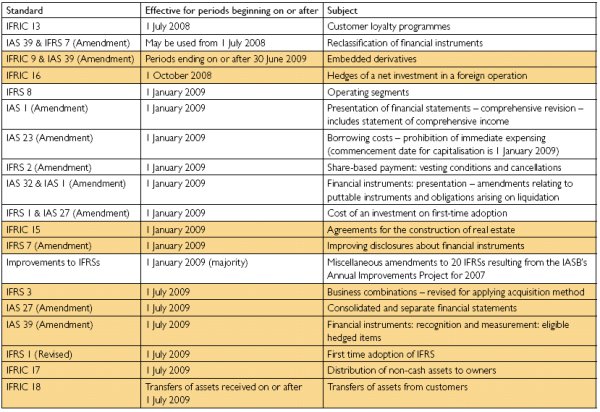

ON THE HORIZON

The table below summarises the effective dates for new and revised IFRS and IFRIC interpretations. Those that are shaded have not yet been endorsed by the EU and the effective date will be contingent on successful endorsement.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.