FINANCIAL REPORTING – THE SHAPE OF THINGS TO COME

Three new proposed accounting standards from the Accounting Standards Board (ASB) are set to change the face of UK financial reporting.

The ASB has for many years said that UK GAAP was not sustainable in the long term. In October 2010 the ASB issued two exposure drafts – one outlining the reporting frameworks that might apply across all UK entities, and the other setting out the proposed standard to be used by the majority of UK preparers.

The ASB received a significant volume of responses with the majority suggesting, among other things, that the proposals to extend full IFRS to entities falling within a new definition of publicly accountable were unnecessarily onerous and that the proposed new UK standard (tentatively named the Financial Reporting Standard for Medium-sized Entities (FRSME)) was too restrictive.

Since the comment period on the original exposure drafts closed, the ASB has put considerable time into refining and reshaping their original suggestions. At the end of January they issued three new exposure drafts containing their revised proposals.

- FRED 46 'Application of Financial Reporting Requirements' (draft FRS 100)

- FRED 47 'Reduced Disclosure Framework' (draft FRS 101)

- FRED 48 'The Financial Reporting Standard applicable in the UK and Republic of Ireland' (draft FRS 102)

Here we look at the proposed shape of future financial reporting as set out in FRED 46. The other two FREDs are considered elsewhere in this newsletter in "UK GAAP – Take 2" and "Reducing the disclosure burden".

The ASB has dropped its suggestion of extending the requirement to apply full EU-adopted IFRS to a wider group than that currently required to do so. Those entities that are eligible to apply the Financial Reporting Standard for Smaller Entities (FRSSE) will be able to continue to use that standard, which will remain virtually unchanged for the time being. All other entities will apply the new 'Financial Reporting Standard applicable in the UK and Republic of Ireland' (referred to hereafter as the 'proposed Financial Reporting Standard').

There are a number of financial institutions that would have met the previously proposed definition of public accountability, but which will now be eligible to use the proposed Financial Reporting Standard. In recognition of the importance of financial instruments to such entities, they will be required explicitly to make additional disclosures based on those in IFRS 7 'Financial instruments – disclosures'.

As discussed further in the later article "Reducing the Disclosure Burden", subsidiaries and parents preparing their financial statements in accordance with EU adopted IFRS will be permitted to take advantage of a number of disclosure exemptions not currently available to them.

When the ASB issued its original proposals it was intended that the additional requirements of public benefit entities (PBEs) would be met through an 'add-on' standard. However, most respondents to the relevant exposure draft (FRED 45) found its interaction with the new accounting standard difficult to understand. The requirements of PBEs have therefore been subsumed into the proposed Financial Reporting Standard.

The ASB is suggesting that the new requirements be mandatory for periods ending on or after 1 January 2015. Early adoption will be permitted for periods that begin on or after the date the final standards are issued.

|

Smith & Williamson commentary There is considerable good news in the revised proposals and it seems that the ASB has really listened to the views of its constituents. The extension of adoption of full IFRS would have been costly for many entities, who would probably not have gained any real benefit as a consequence. We are therefore pleased to see this suggestion removed. The final standards could be issued before the end of the year and early adoption might therefore be possible by 1 January 2013. However, there are some legal matters that still need to be addressed. Among the most significant will be changing the law to permit companies the option to revert from full IFRS to UK GAAP in wider circumstances than the current, very restrictive, provisions. |

UK GAAP – TAKE 2

The ASB's first proposals for an accounting standard to replace current UK GAAP resulted in nearly 300 responses.

The proposed standard, the FRSME, was based on the International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) with minimal amendment. As a consequence many accounting choices offered by current UK GAAP were not permitted and other aspects of established accounting practice were not addressed.

The ASB has taken into account the comments received and in January it issued its revised proposals in the form of FRED 48 'The Financial Reporting Standard applicable in the UK and Republic of Ireland' (draft FRS 102) (the 'proposed Financial Reporting Standard'). While the revised proposed standard is still based on the IFRS for SMEs, the ASB has included a number of accounting options already permitted by current UK GAAP as well as additional guidance in a number of areas.

Accounting policy choices reinstated

Among the accounting policy choices that were not permitted by the proposed FRSME, but which now look set to be retained in the proposed Financial Reporting Standard, are the ability to revalue fixed assets and, where certain criteria are met, to capitalise development and borrowing costs.

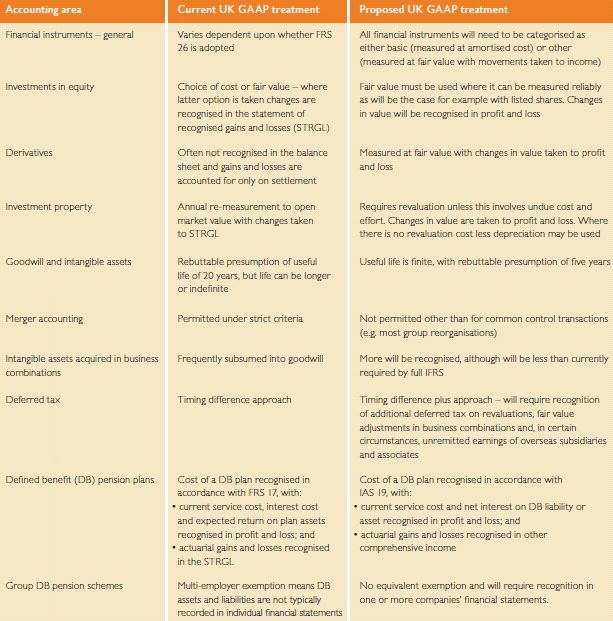

Key differences to current UK GAAP

While there will be much that is familiar to UK preparers, there will be some areas of significant change which will have an effect on the reported results and financial position of many entities. The major differences are considered in the table opposite.

Reduced disclosures for subsidiaries and parent companies

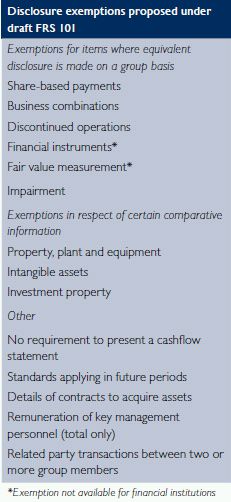

Certain disclosure exemptions will be available in the financial statements of subsidiaries and parent companies applying the proposed Financial Reporting Standard. The exemptions will be available where the relevant financial statements are included in consolidated accounts that give a true and fair view and are publicly available. These exemptions, and the circumstances in which they may be taken, mirror the concessions offered to such entities applying IFRS as discussed in the later article "Reducing the Disclosure Burden".

Public benefit entities

The ASB had originally suggested a separate, supplementary, standard containing guidance specific to PBEs. It has, however, now determined that it would be preferable to include the guidance within the proposed Financial Reporting Standard and the additional requirements have therefore been integrated but are separately identified as applying to PBEs.

When might it all change?

An application date of periods beginning on or after 1 January 2015 is being proposed. Early application will be permitted for periods beginning on or after the date the final standard is issued, but for PBEs required to follow a SORP they will only be able to adopt early if the relevant SORP has also been updated to reflect the new requirements.

|

Smith & Williamson commentary While many of the unpopular restrictions have now been lifted, resulting in a standard that in many ways feels closer to UK GAAP, both preparers and users of financial statements should be aware of the extent to which a number of areas will change. For many preparers, financial instruments will prove to be the most challenging area of the new requirements. Early consideration will need to be given as to how financial instruments will be categorised. Many entities will find themselves with instruments that do not meet the definition of basic, and therefore could be required to incur the cost and effort of obtaining fair value calculations. Reported results will also be affected by the associated volatility that will be introduced into earnings. |

REDUCING THE DISCLOSURE BURDEN

UK groups that are either required to or choose to prepare their financial statements in accordance with IFRS have often elected to present the individual company and subsidiary accounts in accordance with UK GAAP.

There are a number of reasons why companies may have chosen UK GAAP in these circumstances. However, many have found that the absence of any available disclosure exemptions in IFRS resulted in a time and cost burden that outweighed the possible savings from using a consistent set of accounting standards across the group.

Recognising that it would be more cost effective if companies only had to maintain accounting records in accordance with one reporting framework, the ASB has proposed disclosure exemptions that will apply to a large proportion of subsidiaries and parent entities.

Under FRED 47 'Reduced disclosure framework' (draft FRS 101), 'qualifying entities' will be able to take certain exemptions from the disclosure requirements contained in EU-adopted IFRS. The definition of a qualifying entity is straightforward, being a member of a group that prepares publicly available financial statements, which give a true and fair view, and in which the entity is consolidated.

The following additional conditions will need to be met before the exemptions can be taken.

- Shareholders in the entity will need to be notified in writing and not object to the exemptions being taken.

- The financial statements must otherwise apply the recognition, measurement and disclosure requirements of IFRS but formats of primary statements will need to comply with the Companies Act 2006.

- The financial statements will need to disclose the relevant standard and paragraph number of the exemptions taken and the name of the parent in which the entity is consolidated together with where the parent's financial statements could be obtained from.

The available exemptions are set out in the table below.

It is currently proposed that the new standard will apply for periods beginning on or after 1 January 2015, with early application permitted for periods that begin on or after the date the final standard is issued.

|

Smith & Williamson commentary We are pleased to see proposals that will make it easier for consistency to be achieved across groups. The option will however still exist for subsidiary and parent accounts to be prepared in accordance with the new Financial Reporting Standard applicable in the UK and Republic of Ireland. The new standard will continue to have some differences from IFRS but will also contain an equivalent reduced disclosure framework. How a company's accounting policies affects tax and distributable profit may still, however, turn out to be the deciding factor in determining which accounting framework to follow rather than the extent and nature of disclosure required. Entities planning to use the proposed exemptions will also have to be mindful of one complicating factor. While the measurement, recognition and disclosure in the financial statements will be in accordance with IFRS, the financial statements will also need to comply with the Companies Act and therefore the primary statement formats required by company law not IAS 1. |

REVENUE RECOGNITION – REVISED PROPOSALS ISSUED

The development of a new standard for revenue recognition was discussed in the summer 2011 edition of Financial reporting. Since then the IASB has issued a revised exposure draft in response to feedback received on their original proposals.

The IASB decided to revise its proposals after receiving over a thousand comment letters on the original exposure draft (ED), many of which expressed concern that it was not clear how to apply the proposed core principles in practice, particularly to contracts for services and construction contracts.

Proposals in the revised ED

The core principle set out in the revised ED is consistent with the original ED, that "an entity shall recognise revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled to in exchange for those goods and services".

The ED outlines the five steps any entity needs to consider in order to recognise revenue.

Step 1: Identify the contract with a customer.

Step 2: Identify the separate performance obligations in the contract.

Step 3: Determine the transaction price.

Step 4: Allocate the transaction price to the performance obligations.

Step 5: Recognise revenue when a performance obligation is satisfied.

For many companies, step 5 will be the most important in determining the amount of revenue to be recognised in each accounting period.

|

Smith & Williamson commentary For many contracts, such as straightforward retail transactions, the proposals will have little, if any, effect on the timing and amount of revenue recognised. However, in other circumstances, for example long-term service contracts, contracts that contain multiple deliverables (e.g. mobile phone contracts) or contracts for services, the proposed new standard could result in changes to both the timing and amount of revenue recognised. |

Revenue should be recognised when an entity satisfies its performance obligations by transferring control of the goods or service to the customer. If control is clearly transferred at a point in time, for example in a retail transaction when the customer pays for and obtains custody of the item, revenue should be recognised at that point. If control is obtained over a period of time, then revenue should be recognised over that period of time.

The proposals in the original ED would have prohibited the recognition of revenue over time for many construction and service contracts where the asset created by the seller's performance (i.e. the work in progress) is not controlled by the customer until the end of the contract.

However the focus on requiring control before revenue can be recognised over time has been amended in the revised ED. Revenue can be recognised even if the customer does not have control of the work in progress provided that the work in progress does not have an alternative use to the seller and certain other criteria are met (including a right to payment for partial completion). This will mean that more transactions will be accounted for over time than would have been the case under the original ED.

Presentation

A key change from the original ED and from current practice is the proposed treatment of credit losses. The revised ED requires the amount of any expected credit losses and any subsequent adjustments (i.e. any bad and doubtful debt expense) to be presented in a separate line item within the statement of comprehensive income adjacent to the revenue line.

Disclosure

The revised ED proposes a more comprehensive set of disclosures that require both qualitative and quantitative information about revenue and cashflows arising from contracts with customers. Apart from some minor amendments and clarifications, these disclosure requirements have remained unchanged from the original ED.

Effective date

The comment period for the revised ED ended on 13 March and it is possible that the final standard will be issued by the end of 2012. The IASB will not make a final decision on the effective date of the new standard until it has received and reviewed all comments. However, it has indicated that the earliest date by which the new standard will be mandatorily effective is for periods beginning on or after 1 January 2015.

|

Smith & Williamson commentary Although the new standard may not apply yet, it will be retrospective and the impact on some companies could be significant. For entities in the service sector in particular it may be advisable to consider the proposals in the revised ED and understand how the requirements could change the company's accounting policies for revenue recognition. |

IAS 19 (REVISED) – EMPLOYEE BENEFITS

Recent revisions to IAS 19 may have a significant effect on the financial statements of IFRS preparers with defined benefit (DB) pension schemes.

While the changes to the standard include a number of clarifications and updated disclosure requirements, here we concentrate on the changes most likely to affect how schemes are accounted for in the employer's financial statements. The revised standard applies for periods beginning on or after 1 January 2013.

Recognising movements in DB related assets and liabilities

IAS 19 (2011) has a simplified approach to recognising movements in pension assets and liabilities. The only items to be recorded in profit or loss for the year will be service cost and 'net interest'. Including net interest is a change from the existing treatment whereby both the discount rate on fund liabilities and the expected return on plan assets are recognised in profit or loss for the year. Net interest is calculated by applying the discount rate specified by the standard to the net pension asset or liability. The return on plan assets is often higher than the discount rate (for example when the scheme assets include equities or property). Consequently, the previous version of IAS 19 would have resulted in a lower total profit and loss charge (or higher total profit and loss credit) than would be the case under IAS 19 (2011).

All other remeasurements of the DB pension asset or liability will be included in other comprehensive income (OCI).

|

Smith & Williamson commentary A majority of DB pension schemes will be at least in part invested in equities and property. Therefore many entities may find that adopting IAS 19 (2011) results in decreased profits and earnings per share, a situation that could also have an effect on loan covenants. |

The elimination of reporting options, including the corridor method

Prior to the 2011 revisions, IAS 19 allowed a choice of methods for recognising actuarial gains and losses, including:

- immediate recognition via other comprehensive income

- immediate recognition via profit or loss for the year

- the corridor method (an approach which essentially allowed for the deferred recognition of a portion of actuarial gains and losses via profit or loss).

The existence of choice means there can be significant variation in the amounts reported by different preparers having similar economic circumstances. In particular, preparers applying the corridor method could potentially recognise a different pension scheme asset or liability to that recognised if either of the immediate recognition options were taken. The IASB consider that the lack of comparability arising from such a range of options is undesirable and, as a result, IAS 19 (2011) only allows one option – the immediate recognition of actuarial gains and losses via OCI. Amounts recognised in OCI under the revised standard will not be subsequently reclassified into profit or loss for the year.

|

Smith & Williamson commentary Under the previous version of IAS 19, the majority of UK preparers utilised the approach of immediately recognising actuarial gains and losses in OCI. Many UK preparers will, therefore, find that their existing accounting policy with regard to actuarial gains and losses is consistent with the revised standard. However, any entities that previously applied the corridor method will be significantly affected by the revisions as they will be subject to increased balance sheet volatility and may be faced with the immediate recognition of previously deferred amounts. Entities that currently recognise all actuarial gains and losses in profit and loss will not be as severely affected, but will still face a change in accounting. For the affected entities, the switch to recognising all actuarial gains and losses in OCI will mean that profit or loss for the year, and any associated earnings per share figures, will no longer include volatile actuarial profits and losses. |

FINANCIAL REPORTING ROUND-UP

Changes in disclosure of auditor remuneration

The Companies Act requirements in respect of disclosure of auditor remuneration are set to change for all UK companies (whether UK GAAP or IFRS preparers) for periods beginning on or after 1 October 2011. The changes relate primarily to the presentation and classification of the different categories of fees paid to auditors for non-audit services.

In order to assist companies in determining which services fall into which of the new disclosure categories the ICAEW has issued guidance in a technical release TECH 04/11 FRF "Disclosure of Auditor Remuneration". This guidance in available on their website (www.icaew.co.uk).

The new disclosure requirements can be adopted early.

Responding to increased country and currency risk

Prompted by the current economic uncertainties facing a number of countries around the world, the UK Financial Reporting Council (FRC) has published an update for directors of companies listed on the London stock exchange to assist them in responding to increased country and currency risk in their annual and half-yearly financial reports. The update aims to draw together a number of the more significant issues for directors to consider, including the impact of events on impairment testing, going concern assessments and the extent of appropriate disclosure.

While the update is aimed at directors of listed companies, its content will also be relevant to many other UK companies whose businesses have been affected by the ongoing unrest in the Middle East and recent events in the eurozone and who are required to report risks and uncertainties in accordance with the Companies Act.

The full text of the FRC's guidance can be found on their website at www.frc.org.uk/publications/pub2693.html.

Reporting on compliance with the Governance Code

For listed companies with a December year end, the annual report for the year ended 31 December 2011 will be the first annual report in which the company reports on its compliance with the UK corporate Governance Code (Governance Code) as opposed to the Combined Code. The Governance Code replaced the Combined Code for periods beginning on or after 29 June 2010 and applies to all fully listed companies with a premium (formerly primary) listing of equity shares in the UK.

While the Governance Code is very similar to the Combined Code there are a number of new provisions and disclosures which will require consideration when companies are drafting their corporate governance statement for inclusion in their annual report.

ON THE HORIZON

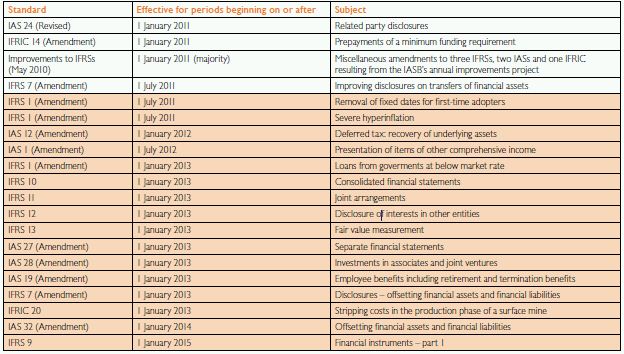

The table below summarises the effective dates for new and revised IFRS and IFRIC interpretations. Those that are shaded have not yet been endorsed by the EU and the effective date will be contingent on successful endorsement.

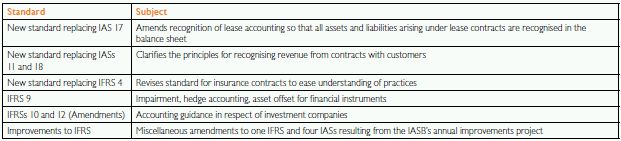

In addition, the following standards may be published by the IASB before the end of 2012. Standard title, effective date and EU endorsement will be confirmed following publication.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.