The Test for NCA Applicability

The National Credit Act No. 34 of 2005 ("the NCA" or "Act") has had a significant impact on transactions involving deferred payment and interest in South Africa.

However, it has almost become trite law to refer to the interpretive challenges that arise out of the poor drafting, while at the same time praising it's good intentions. See, for example, Nedbank Ltd and Others v The National Credit Regulator and Another (662/2009, 500/2010) [2011] ZASCA 35 (28 March 2011) at 2.

The purpose of this article is to give a broad understanding of when the NCA applies to a transaction.

The applicability of the Act to a transaction can have far-reaching consequences as the NCA is extensive in its consumer protection. It places many obligations and restrictions on the credit provider whose transaction is subject to the Act and conversely provides many benefits to the consumer in such a transaction.

To determine the applicability of the NCA to any particular transaction involves answering a two-fold enquiry drawn from the provisions of Section 4 of the Act:

- Does the Consumer in the agreement fall within the NCA (Section 4)?

- Does the transaction fall within the definition of credit agreement as set out in Section 8?

The construction of Section 4 is such that if the answer to the first question is negative, then there is no need to proceed to the second question. But if it is positive, then the transaction still has to clear the hurdle of the second question to fall within the ambit of the Act.

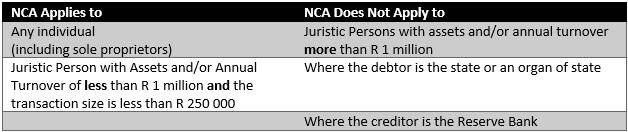

Section 4(1) of the NCA, states :

"Subject to sections 5 and 6, this Act applies to every credit agreement between parties dealing at arm's length and made within, or having an effect within, the Republic, except a credit agreement in terms of which the consumer is-

(i) a juristic person whose asset value or annual turnover, together with the combined asset value or annual turnover of all related juristic persons, at the time the agreement is made, equals or exceeds the threshold value determined by the Minister in terms of section 7( 1);

(ii) the state; or

(iii) an organ of state;

(b) a large agreement, as described in section 9(4), in terms of which the consumer is a juristic person whose asset value or annual turnover is, at the time the agreement is made, below the threshold value determined by the Minister in terms of section 7(1); "

As at the date of this article the threshold is an annual turn-over or asset value exceeding R 1 million in terms of Section 7(1)(a) as read with Government Gazette GG 28893 of 1 June 2006, Schedule 2. While a large agreement is R 250 000 or over in terms of Section 7(1)(b) as read with Government Gazette GG 28893 of 1 June 2006, Schedule 3(2).

When dealing with juristic persons and the NCA it is important to note that:

- the NCA definition of juristic person is not the common South African legal definition of juristic person. It extends beyond incorporated entities to include partnerships, associations or other unincorporated bodies of persons and trusts if there are three or more individual trustees or the trustee is itself a juristic person.

- Section 6 of the NCA excludes the application of numerous provisions of the Act to juristic persons, importantly the sections governing the charging of interest and the reckless lending provisions.

In broad terms, the following applies to the first question:

What is a Credit Agreement?

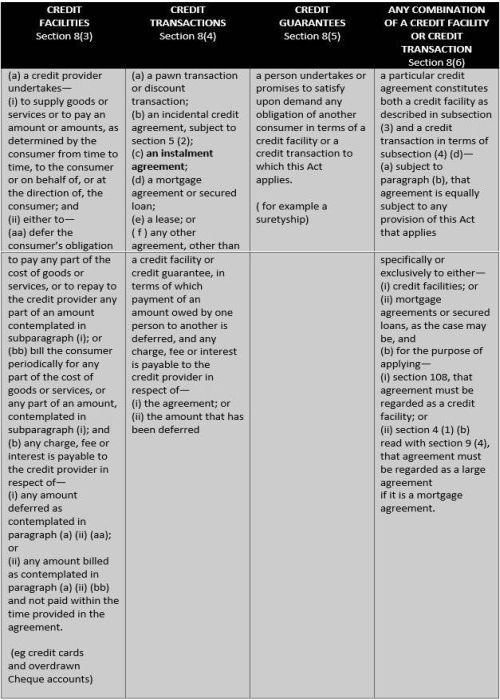

Section 8 of the NCA defines what credit agreements are and separates the definition into four categories.

Also note that Section 8(2) of the Act excludes insurance policies, leases of immovable property and stokvel agreements from the ambit of the NCA.

Credit Facility

When the Act was initially introduced, there was some confusion with the potential overlap in the definition of credit facilities and incidental credit agreements. Fortunately, the court in JMV Textiles (Pty) Ltd v De Chalain Spareinvest 14 CC and Others (15136/09) [2010] ZAKZDHC 34 at 14, clarified what a credit facility is with examples:

"...the proper starting point is to identify the type of transactions contemplated in sub-sect (a). They are of two types. The first is the supply of goods or services at the consumer's request and either the deferment of the obligation to pay the price or periodic billing of part of the amount. The second is the payment by the credit provider of amounts to either the consumer or third parties at the consumer's request, where the obligation to repay is deferred or is the subject of periodic billing in respect of part of the amount. The former aptly describes the position with store charge cards or accounts and the latter the position with credit cards. In the case of a store card the customer is allowed to buy goods up to a determined limit, payment is deferred to the end of the month and the customer is billed monthly. A fee may be charged for the right to use the card and if the full balance is not paid monthly interest is chargeable on the shortfall. The customer decides how much to pay each month subject to paying a stipulated minimum amount such as 10% of the amount owing. With a credit card the position is similar save that the card provider pays amounts to persons from whom the cardholder buys goods or obtains services and may also disburse cash to the cardholder. Repayment is deferred and the monthly billing results in interest being levied if the full amount is not paid, as the customer is free to do subject to making a minimum payment. In some cases a fee is charged for the right to use the card. All of this is part and parcel of the agreement under which the card is issued."

Credit Transactions

While credit facilities is a broad definition, that of credit transactions is made up of several separate definitions for each of the specific transactions, which are defined in Section 1.

The definitions of the various credit transactions (excluding incidental credit agreements, which will be dealt with later) are:

There have been issues with these definitions, such as the lease of movable property being contray to the normal commercial and legal understanding of lease in which ownership does not pass at the end of the agreement. Besides this, definitions such as mortgage agreement have been amended and there is also questions over the overlapping definition of discount transactions and incidental credit agreements, which could have serious implications.

Incidental Credit Agreements

This type of credit transaction is a very important one as in terms of Section 5 of the NCA many of the more onerous provisions of the Act are excluded from application to Incidental Credit Agreements. These include:

- Pre-agreement disclosures

- The form and content of the agreements

- Unlawful agreements and unlawful provisions in agreements

- Reckless credit granting

- Registration requirements

- Marketing practices

- Surrender of goods

- The consumer cooling-off right; and

- The dispute settlement mechanisms of the NCA

The definition of incidental credit is defined under Section 1 as:

"...an agreement, irrespective of its form, in terms of which an account was tendered for goods or services that have been provided to the consumer, or goods or services that are to be provided to a consumer over a period of time, and either or both of the following conditions apply:

(a) a fee, charge or interest became payable when payment of an amount charged in terms of that account was not made on or before a determined period or date; or

(b) two prices were quoted for settlement of the account, the lower price being applicable if the account is paid on or before a determined date, and the higher price being applicable due to the account not having been paid by that date;"

So for example if one were to take a supplier of goods or services who engages in the common practice of allowing their customers to pay their account 30 days from date of statement. The purpose of such a deferment of payment is not to benefit such a supplier with interest or deferred payment charges but merely a way to facilitate commercial convenience. However one of the challenges that such a supplier encounters with such deferred payment is customers who exceed the payment terms. As a result some of these suppliers will use one or both of the "carrot and stick" motivational approaches to ensuring timely payment – the stick being charging interest on overdue accounts and the carrot being giving an "early settlement discount" on the purchase price if the customer pays before the due date. These are the types of transactions which are intended to fall within the definition of incidental credit agreements.

As to when such an incidental credit agreement comes into being is defined in Section 5(2) which reads as follows:

"The parties to an incidental credit agreement are deemed to have been made that agreement on the date that is 20 business days after –

(a) the supplier of the goods or services that are subject of that account, first charges a late payment fee or interest in respect of that account; or

(b) a pre-determined higher price for full settlement of the account first becomes applicable,

unless the consumer has fully paid the settlement value before that date."

Three Categories of NCA Impact on Transactions

To understand the impact of the NCA on transactions, the writer divides transactions into three broad categories of impact:

- Transactions that fall outside the NCA (no impact)

- Incidental Credit Agreements ( limited impact under Section 5)

- "Full-blown" Credit agreements (full impact in terms of the provisions of the Act)

For a credit provider who does not wish to be burdened by the application of the NCA to their transactions, these categories are a descending order of preference. Therefore many credit providers try to ensure they construct transactions which fall outside of the NCA definition of credit agreement or argue that their existing transactions are not credit agreements. However, for credit providers who wish to benefit financially from the business of deferred payment, the chances are that they will have to be content with full compliance with the NCA.

Credit Guarantee

The most important form of credit guarantee is suretyship.

Section 4(2)(c) provides:

"this Act applies to a credit guarantee only to the extent that the Act applies to a credit facility or credit transaction in respect of which the credit guarantee is granted"

What in effect this subsection is saying is the that the suretyship, being an accessory agreement, follows the main agreement (Da Silva v Slip Knot Investments (661/2009) [2010] ZASCA 174 (2 December 2010)). So therefore if :

- the main agreement falls outside the NCA, the suretyship will too;

- if the main agreement is an incidental credit agreement, then the suretyship will be too; and

- if the main agreement is a "full-blown" credit agreement, then the suretyship will be as well.

Conclusion

All credit providers or suppliers operating within South Africa should be fully aware of the impact of the NCA on the transactions in which they allow any form of deferred payment, charge interest or charges. They should contract in a manner which does not unintentionally compromise themselves and be aware of alternative methods of transacting.

The NCA with it's poor drafting and the resultant ambiguty can be challenging and therefore requires a sound knowledge of it's application to transactions.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.