As the world's digital pathways multiply and thicken—and even begin, perhaps in some ways, to rival the world's road networks—any sector slow to start using them is increasingly conspicuous. Thus, the real estate sector, or more broadly alternative investments. Where is the industry overhaul, the massive sweep of technology? Elsewhere, fintech companies are building digital ledgers to settle transactions, healthtech companies are 3D-printing knee bones, and much more—but alternative investment firms have been largely shielded from this wave. In this article, leaning on the results of a recent survey carried out in this area, I'll discuss why this might be and when it might change.

Slow burn

In one sense, it would be ludicrous to suppose that proptech could spread as swiftly as e-payment apps or such things, simply because the latter rely on a pocket-sized device that people generally replace every two or three years, whereas buildings, well—the one I'm sitting in right now was built in 2014 and shouldn't need replacing for a good five or six decades. So when it comes to, for example, smart hubs using radio waves to interconnect a house's appliances, these are not easily implemented without invasive renovation. Another barrier is that such networks are not yet really standardised across manufacturers in the same way apps are on smartphones.

So the Internet-of-Things side of proptech will follow the truncated pace of building construction, which is fair. But there are business-side stumbling blocks too. According to a recent KPMG and CREATE-Research survey, margins are mostly healthy for real estate companies which lessens the appetite for risky innovating. The same survey uncovered some other themes of hesitation amongst decision-makers too: many are more focused on keeping immediate investment returns buoyant than on getting inventive in their garages, and the crisis of ten years ago is still reverberating in the form of risk aversion. Quite simply, the industry is still collectively comfortable—it's still risker to be the first mole poking your head out of the ground. But time will alter that: at some point, the riskier move will be to cling to the tattered old business models, down in the mole hole, built on aged technology.

Thus, the remaining question is: when exactly will that transition point come? Nobody can put it down to a date and time, but these do seem to be ripening times. The same survey cited above concluded that, of 125 alternative investment firms analysed spanning 19 countries, the vast majority are underutilising existing digital tools.

Absolute innovation disrupts absolutely

We have established the relatively uncontentious point that inventive technologists are lining up waiting for the alternative investment industry's embrace. Getting into less certain waters, I want to also discuss how this disruption might happen.

A year ago it looked like fintech startups were in a position to uproot established companies entirely, sliding into the alternative investment space with fresh, unbeatable business models and the spoils of futurism. Now, however, as the entire fintech scene continues to mature, that looks less likely. (Also because, for the time being, there is no alternative investment mass market for them to conquer). Indeed, only 22% of respondents in our survey—largely managers of mid-sized funds—espoused this view, whereas twice as many managers (44%) favoured the view that what's being disrupted is methodology rather than whole companies. In other words, alternative investment funds are collaborating, more than competing, with fintechs, using them to digitise parts of their value chains. And the fintechs benefit too, from the industry experience and big client lists.

How thick, how fast?

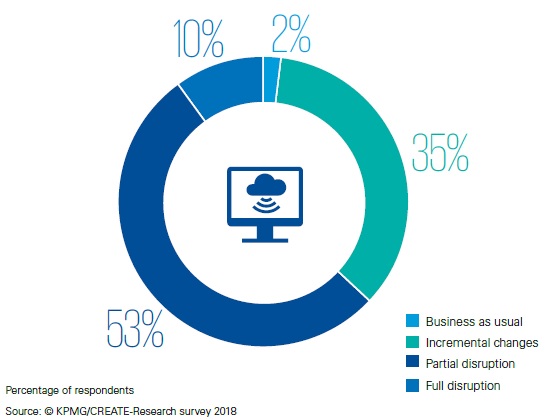

As perhaps befits a group of people known for managing risks and maintaining secure returns, the majority of alternative fund managers see digital disruption as happening either partially (53%) or incrementally (35%). Only 10% feel that they're on a dark roadway staring at the headlights of absolute change.

Figure 1. Which scenario summarises your view on the impact of digitisation on the alternative investment industry over the next 10 years?

That the bulk of alternative managers opted for this middle ground could also suggest that they're waiting for, if not actively seeking, a way into the innovation frenzy. To that end, my team and I have prepared a to-do list for managers in such a position:

- Evaluate what fintechs are doing, and determine the feasibility of developing new, digitalised ideas and tools in a legacy environment.

- Choose where (if anywhere) in-house tools should be built, and for other processes seek strategic partnerships with best-of-breed third-party administrators.

- Hire (or at least start eyeballing) computer scientists, data specialists, and other technologists who will need to work alongside portfolio managers, risk specialists, and client service teams.

- Revamp internal regulatory measures (as these change quickly and, in a digital context, gain complexity)—without killing off the culture of employee creativity.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.