In this document, Deloitte presents a brief overview of tax and customs concessions applicable to foreign investment in Uzbekistan.

As the taxation system in Uzbekistan is subject to frequent changes, we recommend using this overview for general purposes only. We will be glad to discuss any tax-related issues you may have in more detail.

Foreign investments

To attract direct foreign investment, Uzbekistan operates a system of various tax and customs concessions. Tax concessions extend to specific industries or areas, for example, when registering a company in one of the industrial zones. Deloitte helps investors chose the best business model for operations in Uzbekistan and to analyse the best options for business development.

Investment in specific industries

Presidential Edict № УП-3594 dated 11 April 2005 provides tax concessions to production companies in the chemical and petro-chemical, engineering, light, food, alternative energy and other industries.

Qualifying companies are exempt from:

- corporate profits tax;

- property tax;

- tax on improvements and the development of social infrastructure;

- obligatory contributions to the National Road Fund;

- the integrated tax payment for micro-firms and small businesses;

The tax concessions in question are awarded based on investment amounts and apply for between 3 and 7 years, provided:

1. the companies in question are represented in all towns and rural areas of the country, except for Tashkent and Tashkent Oblast;

2. foreign investors make private direct investments without state grants;

3. foreign participants' interest in share capital should be at least 33%;

4. foreign investments are made in freely convertible currency or in the form of new and modern production equipment;

5. at least 50% of income generated as a result of application of the concessions is reinvested for further company development.

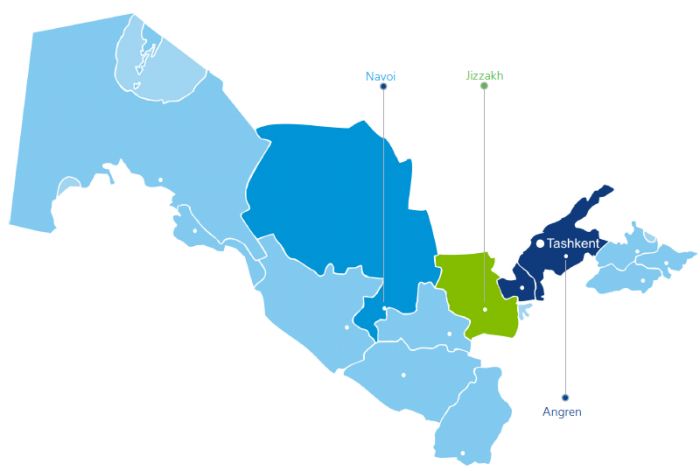

Investment in specific economic zones

Special concessions have been approved for the development of specific regions of Uzbekistan. The following Special Economic Zones have been created:

- Navoi Free Industrial and Economic Zone1

- Angren Special Industrial Zone2

- Jizzakh Special Industrial Zone3

Subject to the value of foreign investment, companies are eligible for concessions of varying duration on:

- land tax

- property tax

- corporate profits tax

tax on improvements and the development of social infrastructure and others

As an additional stimulus, special rules for making payments in foreign currency have been introduced for companies registered in the above zones.

Companies are entitled not to apply items of tax law that worsen their tax position.

In addition to the general concessions applicable in all zones, special concessions apply in specific zones.

At your request, we can prepare more detailed information on current tax and customs concessions, registration conditions and foreign company operations in Uzbekistan for specific companies and activities.

Footnotes

1 Presidential Edict №УП-4059 dated 2 December 2008 On the Creation of a Free Industrial and Economic Zone in Navoi Oblast

2 Presidental Edict №УП-4436 dated 13 April 2012 On the Creation of the Angren Special Industrial Zone

3 Presidential Edict №УП-4516 dated 18 March 2013 On the Creation of the Jizzakh Special Indsutrial Zone

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.