- within Intellectual Property topic(s)

- with Inhouse Counsel

- in United Kingdom

- with readers working within the Chemicals industries

Freedom-to-operate (FTO) used to be the analysis a life-science company commissioned before a product launch or a sale. Public funders have moved it to the top of the list — and where they have led, private capital is following.

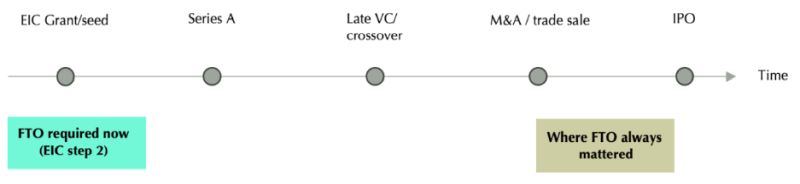

Freedom-to-operate used to sit late in a life-science company’s product timeline. You raised funding on the strength of your own patent positions, advanced the programme, and commissioned a serious FTO opinion shortly before a product launch, a trade sale, or an initial public offering made third-party infringement risk concrete. Diligence on the buy side priced that risk; the company itself often deferred it. That sequence has inverted, and the clearest signal comes from the public funders that sit at the very start of the journey, especially in life science which is highly dependent on incoming capital.

Figure 1 – Freedom-to-operate scrutiny has shifted from product launch or the end of the lifecycle to the grant and seed stage.

What the EIC actually requires

Since 2021, the European Innovation Council has asked EIC Accelerator applicants to upload a freedom-to-operate analysis with the EIC Step 2 application. Where the applicant has no FTO analysis, the requirement does not disappear — it converts into a mandatory short note, of at most two pages, which must outline the freedom-to-operate position with as much supporting information as the company can give; only where FTO is genuinely irrelevant, as for some pure software applications, will a simple statement suffice. For a therapeutics or platform-biology company, none of those carve-outs apply: the FTO analysis is expected, and it is read by the council.

It is read because the EIC Accelerator is not only a grant, but rather couples the grant with an equity investment made through the EIC Fund, and on that investment the European Investment Bank acts as the Fund’s investment advisor, carrying out the due diligence that supports the investment decision. In other words, the FTO is not uploaded into a void. It enters a genuine investment due diligence process run by a development bank’s investment officers, on the same logic a venture investor would apply, and it forms part of the path to sign-off for the development bank as for the venture investor.

Figure 2 — The FTO analysis sits inside the EIC blended-finance sign-off path, not alongside it.

The EIC FTO checkpoint is a leading indicator, not a quirk

It would be a mistake to read the EIC requirement as an outlier; merely one programme’s paperwork. This requirement is simply the visible tip of a much broader repricing of early-stage IP risk. A public deep-tech funder that puts FTO into its sign-off path at seed stage is doing what sophisticated private capital has been moving toward independently: refusing to treat the company’s strong patent position as evidence of its freedom to operate, because the two are different issues.

Owning a patent tells others that they may not copy you; it tells you nothing about whether your product infringes a claim someone else already holds. Venture investors, crossover funds and strategic acquirers increasingly want that second issue addressed early,

What a funder-grade FTO has to be

The trap is trying to satisfy the requirement by submitting a document that uses the phrase “freedom to operate” without doing the work or presenting the analysis. A two-page note that asserts the company is “not aware of any blocking patents” is worse than nothing: it signals to a professional diligence team that the company has not even bothered to look properly. A funder-grade FTO (and, increasingly, an investor-grade one) does the following:

- Define the commercial product, its features and the territorium that matter

- Identify in-force third-party claims that actually read on it

- Assess infringement risk claim-by-claim, not patent-by patent

- Test the validity of any blocking right you would otherwise respect

- Map the design-arounds, licences or challenges available

- State a reasoned conclusion – not a bare assertion of “freedom”

The difference that separates a credible FTO from a comfort letter is that it works claim-by-claim, not patent-by-patent. Infringement comes down to a question of a single claim of a single patent read against a specific product in a specific territory; a search that lists patents without construing their claims against what the company will actually make and sell has not assessed freedom to operate at all. And the correct approach does not stop at identifying risk: it pairs each genuine blocking right with the realistic response: a design-around, a licence, an invalidity position, or a reasoned position that the claim in fact does not read on the product. A funder, like an acquirer, is reassured far more by a clear-eyed account of two manageable risks than by a document that claims to have found none.

What founders and boards should do now:

- Treat FTO as a fundraising deliverable, not just a pre-launch one. If a public funder such as EIC wants it at Step 2, the odds are that your next private round will want it too. Consider and prepare the FTO analysis before you need it, while there is still time to act on what it finds.

- Commission the FTO early enough to change the answer. An FTO run at the seed stage can still steer claim drafting, design-arounds and licensing-in. If run only at the term-sheet stage, it can only confirm freedom or block the next steps.

- Make the FTO claim-level and product-specific. Tie the analysis to the commercial product and the territories that matter, and construe the blocking claims against it. A list of patents is not an FTO.

- Resist the bare two-page reassurance. Where the EIC permits a short note, use it to summarise real work, not to substitute for it. The note is read by people who can tell the difference and will act accordingly.

- Keep the FTO and the diligence record up to date. The same analysis will be asked for again at the next round, in M&A and at IPO, and also at market launch. Maintained from the seed stage, it becomes an asset in every later deal rather than an urgent problem at a late stage

The take-home message

Freedom-to-operate has moved upstream and is not moving back. The EIC has put it into the sign-off path at its earliest funding stage; the EIB applies rigorous investment diligence to it; and private capital is converging on the same expectations from the opposite direction. For a life-science company, the implication is simple and slightly uncomfortable: The FTO is no longer something you initiate when the deal or launch is in sight, but something your serious counterpart now expects you to have produced already. The companies that realise that and build a maintained, claim-level FTO from seed stage turn a recurring diligence demand into a standing advantage. The ones, however, that treat FTO as a box to tick at Step 2 will meet it again, less forgivingly, at every gate thereafter.

References

European Innovation Council — official sources

EIC Accelerator — application requirements, including the freedom-to-operate analysis at Step 2 (and the short FTO note where none exists). European Innovation Council, European Commission. eic.ec.europa.eu — EIC Accelerator

EIC Accelerator — Frequently Asked Questions (freedom-to-operate analysis required since 2021; ≤2-page note where unavailable; statement where FTO is not relevant). eic.ec.europa.eu — Accelerator FAQs

EIC Fund and blended finance — equity investments through the EIC Fund, with the European Investment Bank acting as the Fund’s investment advisor and carrying out eic.ec.europa.eu — about the EIC Fund

EIC Work Programme (current year) — the legal basis defining the EIC Accelerator application and award process.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]