- within Corporate/Commercial Law topic(s)

- in United States

- with readers working within the Law Firm industries

- within Corporate/Commercial Law, Government, Public Sector, Media, Telecoms, IT and Entertainment topic(s)

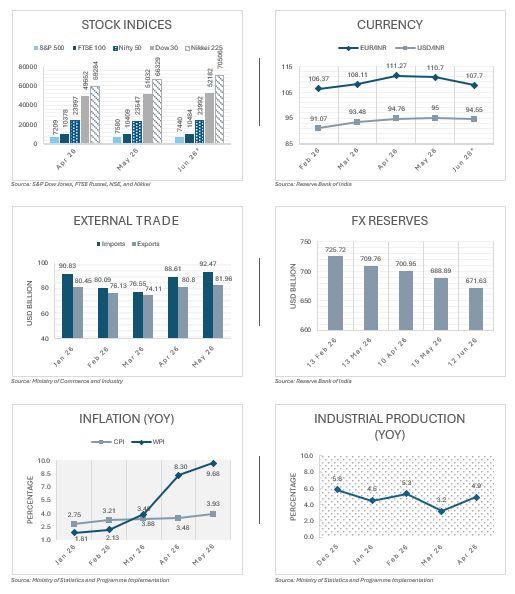

Indian economy | June 2026

Snapshot of key indicators

As per the latest available data for June 2026

SEBI brings major Index Providers under direct regulatory oversight

SEBI Circular on Significant Indices under the SEBI (Index Providers) Regulations, 2024

Even as investments into capital markets have grown rapidly over the past decade, the Index Providers (IPs) whose decisions influence crores of investors have effectively remained outside Securities and Exchange Board of India (SEBI)'s regulatory oversight, despite the existing broader legal framework under the SEBI (Index Providers) Regulations, 2024 (IP Regulations). With the recent Circular, SEBI has sought to address this gap by introducing the concept of 'Significant Indices'.

Key features

- Definition of a Significant Index: An index qualifies as a Significant Index if the daily average cumulative Assets Under Management (AUM) of mutual fund schemes tracking it exceeds INR 20,000 crore for each of the previous 6 consecutive months. Reviews are conducted biannually, assessed at the end of June and December each year. Notably, the moment an index is identified as being a significant one, it is kept in the list till its AUM does not fall below the prescribed limit for 3 consecutive years.

- Formally identified indices: In terms of AUM data from July to December 2025, SEBI has released the initial list of 48 Significant Indices in the categories of equity, debt, and hybrid. This list includes major indices such as Nifty 50, BSE Sensex, Nifty Bank, Nifty 100, Nifty 200, Nifty 500, BSE 100, BSE 200, BSE 500, BSE Healthcare, Nifty Infrastructure, and others.

- Mandatory registration within 6 months: The providers managing the Significant Indices (presently, NSE Indices Ltd, BSE Index Services Pvt Ltd, and CRISIL) will be required to file the application for registration with SEBI in accordance with Regulation 4 of the IP Regulations by November 5, 2026, without which they will not be able to continue their services.

- Registration requirements: The criteria for registration as IPs under the IP Regulations are as follows:

- Incorporation as a company under the Companies Act, 2013

- Net worth of at least INR 25 crore

- Sufficient infrastructure in terms of systems, manpower, and internal controls

- The satisfaction of SEBI's requirements regarding fit and proper character, and financial standing on the part of the applicant, its promoters, and directors

- Conformity to the International Organisation of Securities Commissions (IOSCO) Principles for Financial Benchmarks, to be proved by an independent auditor's report

- Separate legal entity requirement: In case a firm which is already registered with SEBI in another capacity, such as a stock exchange or a credit rating agency, is also providing Significant Indices from one of its internal divisions, it is required to create a distinct entity for performing the task of IP by May 5, 2028. Such ring-fencing of structure takes care of potential conflict of interest between index construction and other regulated activities under the same roof.

- For NSE Indices and BSE Index Services, which already operate as distinct subsidiaries of their parent exchanges, the structural question is more straightforward. For CRISIL, which combines credit rating, research, and index provision under a broader entity umbrella, the 2-year carve-out timeline is more operationally material and will require legal and structural planning in the near term.

- Reserve Bank of India (RBI) exemption: The IPs are not required to be registered with SEBI in case all the Significant Indices notified by them have been notified as Significant Benchmarks or Authorised Benchmarks under the RBI. Even if a single Significant Index is not registered with the RBI, the IP will be required to register with SEBI. Any index, which is subsequently notified by the RBI as a Significant Benchmark, will be exempt from the IP Regulations even though it is present in SEBI’s list of Significant Indices.

- Grievance redressal: The SEBI redressal mechanisms in relation to Significant Indices would apply only to registered IPs. For investors, where an index calculation error, a contested methodology change, or a non-transparent corporate action treatment affects investor returns, SEBI's complaint mechanism against registered providers offers a structured avenue for redressal for the first time.

India expands foreign individual participation in listed companies

Foreign Exchange Management (Non-Debt Instruments) (Third Amendment) Rules, 2026

On June 12, 2026, the Ministry of Finance amended the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 (NDI Rules), significantly expanding the investor base for Indian capital markets by permitting foreign individuals resident outside India – not just Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) – to invest in listed Indian companies through recognised stock exchanges (Amendment).

Key amendments

- Expansion of eligible investors: The Amendment replaces references to ‘an NRI or OCI' with the broader category of 'an individual person resident outside India, including an NRI or an OCI.'

- Trading of listed securities: Subject to the limits and conditions prescribed under Schedule III of the NDI Rules, such individuals may now purchase and sell equity instruments of listed Indian companies on a repatriation basis through recognised stock exchanges in India, through a branch designated by an Authorised Dealer for that purpose.

- Transfer of securities: Eligible foreign individuals holding equity instruments or units on a repatriation basis may transfer such holdings by way of sale or gift to another person resident outside India, subject to applicable sectoral conditions and approvals.

- Government approval requirements: Prior Government approval will be required where an investment or transfer results in ownership or control of a listed Indian company passing to entities or citizens of a country sharing a land border with India, or where the beneficial owner is a citizen of such a country. The term 'beneficial owner' has been aligned with the definition under the Prevention of Money Laundering Act, 2002.

- Clarification of investment limits: Schedule III now provides that an individual foreign investor's holding must remain below 10% of the paid-up equity capital of a listed Indian company. The aggregate holding of all such foreign individuals under this route cannot exceed 24%, unless otherwise permitted.

- Reclassification as Foreign Direct Investment (FDI) upon breach: Where an investor's holding exceeds the prescribed threshold and is not divested within the stipulated period, the entire investment may be reclassified as FDI, aligning the treatment of such breaches with the framework applicable to foreign portfolio investors.

The Amendment represents a significant liberalisation of India's foreign investment regime by opening the listed equity market to a broader class of foreign individual investors. By moving beyond the earlier NRI and OCI framework, the Government has expanded avenues for global retail participation in Indian capital markets while preserving existing safeguards relating to ownership, control, and national security.

While the revised framework is expected to improve market accessibility and deepen foreign investor participation, listed companies, intermediaries, and investors will need to closely monitor investment thresholds, sectoral restrictions and beneficial ownership requirements to ensure continued compliance under the Amendment.

Supreme Court proposes AI governance framework for Courts

Draft Regulations for Use of Artificial Intelligence in Courts, 2026

The Supreme Court of India’s AI Committee released the Draft Regulations for Use of Artificial Intelligence (AI) in Courts, 2026, marking a significant step towards establishing a formal governance framework for the adoption, deployment, and oversight of artificial intelligence within the Indian judicial system.

Key proposals

- Regulation 4 | Human oversight remains mandatory: AI systems may only function in an assistive capacity. The authority to determine questions of law, fact, and justice will remain exclusively with judicial officers, who will retain ultimate responsibility for all decisions.

- Regulation 19 | Permitted use of AI in Courts: Subject to appropriate approvals and oversight, AI may be used for case management, scheduling, legal research, precedent retrieval, citation verification, document summarisation, transcription, translation, accessibility services, record management, and litigant-facing chatbots.

- Regulation 20 | Prohibition on high-risk AI applications: The Draft Regulations prohibit AI-driven adjudication, judicial outcome prediction, sentencing recommendations, risk scoring of litigants or accused persons, behavioural profiling, surveillance activities, and the use of opaque or unexplainable AI systems in matters affecting rights or personal liberty.

- Regulation 43 | Mandatory disclosure of AI-generated content: One of the most significant proposals relates to the use of generative AI by litigants and legal representatives. Any document, pleading, evidence or submission prepared using AI tools must be disclosed to the Court.

- Chapter IV | Dedicated AI governance structure: The framework proposes the establishment of a permanent Apex Body at the Supreme Court level, AI Committees in the Supreme Court and High Courts, dedicated AI Secretariats and a Centre of Research and Excellence on Artificial Intelligence (CoRE-AI).

- Chapter V | Audits and transparency requirements: AI systems would be subject to technical and ethical impact assessments prior to deployment and periodic legal, technical, and ethical audits thereafter. Courts would maintain AI Registers and publish annual transparency reports.

- Regulations 10 and 48 | Data protection and cybersecurity safeguards: AI deployments must comply with the Digital Personal Data Protection Act, 2023, the Information Technology Act, 2000, and privacy-by-design principles. The framework mandates cybersecurity audits, access controls, anonymisation measures, and incident reporting obligations.

- Regulation 46 | Regulation of private AI entities: Private entities providing AI solutions to Courts would be subject to extensive compliance obligations. All agreements entered into with private entities for AI-related services must include provisions on data protection, audit rights, incident reporting, model transparency, explainability, cybersecurity safeguards, and liability allocation. Vendors would also be restricted from retraining or fine-tuning AI models using Court data without prior approval. Where AI tools are developed using judicial data or Court resources, Courts would retain ownership rights or receive a perpetual royalty-free licence over the resulting tools and outputs.

RBI introduces a formal acquisition finance framework for banks

Reserve Bank of India (Commercial Banks – Credit Facilities) Amendment Directions, 2026 (Revised)

The Reserve Bank of India (RBI) has revised the framework governing acquisition finance, loans against securities, bridge finance and lending to Capital Market Intermediaries (CMIs), superseding the earlier amendment issued on February 13, 2026 (with effect from July 1, 2026), or an earlier date if adopted by a bank in entirety (Amendment). The framework seeks to facilitate strategic acquisition financing while introducing enhanced prudential safeguards relating to leverage, capital market exposure and risk management.

Key changes

- Expanded definitional framework: The Amendment introduces and refines key concepts including acquisition finance, bridge finance, CMIs, cash and cash equivalents, eligible securities, Loan-to-Value (LTV), margin, and control, providing greater regulatory clarity.

- Broader acquisition finance framework: Acquisition finance is now linked to the acquisition of control, including through mergers and amalgamations, and may also include refinancing of target debt where integral to the acquisition transaction.

- Expanded acquisition structures: Banks may provide acquisition finance for direct acquisitions, acquisitions through subsidiaries or SPVs, and acquisitions of domestic or foreign non-financial target companies, subject to prescribed eligibility conditions. This provides Indian corporates with an additional domestic financing avenue and reduces dependence on offshore funding structures and alternative credit providers.

- Enhanced borrower eligibility criteria: Acquisition finance may be extended only to financially strong acquirers meeting specified net worth, profitability and, in the case of unlisted entities, credit rating requirements.

- Funding and leverage safeguards: Bank financing is capped at 75% of the acquisition value, with the balance required to be funded through specified sources of own funds and subject to a post-acquisition consolidated debt-to-equity ratio of 3:1.

- Control acquisition requirements: Acquisition finance may be utilised for acquiring control through equity shares, compulsorily convertible preference shares, or compulsorily convertible debentures, with acquisition required to be completed within 12 months from first disbursal.

- Related party and security restrictions: Acquisition finance is generally prohibited for related party transactions and is subject to prescribed security creation, corporate guarantee, and subordination requirements.

- Refinancing of acquisition debt: The framework expressly permits refinancing of acquisition debt after completion of the acquisition, subject to prescribed prudential safeguards, and end-use restrictions.

- Integrated framework for loans against eligible securities: A consolidated regime has been introduced governing lending against listed securities, debt instruments, mutual funds, Exchange-Traded Funds (ETFs), Real Estate Investment Trusts (REITs), and Infrastructure Investment Trusts (InvITs), together with prescribed LTV limits and prudential safeguards.

- Revised limits for individual borrowers: Loans against eligible securities and Initial Public Offer (IPO)/Follow-on Public Offer (FPO)/Employee Stock Option Plan (ESOP) financing are now subject to banking-system-wide prudential limits and margin requirements.

- Dedicated framework for capital market intermediaries: The Amendment introduces a separate framework governing lending to CMIs, including brokers, clearing members, custodians, and market makers. This enhances risk management and oversight of capital market-related exposures while ensuring continued availability of credit for legitimate business purposes.

- Restrictions on proprietary trading exposures: Banks are generally prohibited from financing acquisition of securities by CMIs for proprietary trading purposes, except in limited specified circumstances.

- Enhanced collateral and risk management requirements: Lending to CMIs is subject to prescribed collateral coverage, haircut requirements, exposure limits, and ongoing monitoring obligations.

- Strengthened governance framework: Banks are required to adopt Board-approved policies governing acquisition finance, bridge finance, loans against securities, and exposures to CMIs.

- Transition framework: Existing facilities may continue until maturity, while fresh facilities and renewals must comply with the Amendment from the date of adoption or implementation.

The Amendment marks a significant evolution in India's acquisition financing landscape by introducing a formal framework for bank-funded acquisition finance. It is expected to strengthen the M&A ecosystem, particularly in the mid-market segment, while expanding access to domestic financing and reducing reliance on alternative funding sources.

Certain provisions may, however, pose practical challenges. The restrictive definition of ‘own funds’ and the exclusion of transactions involving non-financial targets with financial-sector subsidiaries or joint ventures may limit flexibility in deal structuring. The requirement to acquire control within 12 months from first disbursal may also be difficult in transactions involving multiple approvals or complex cross-border elements. In addition, implementation of the refinancing provisions and enhanced collateral, valuation and monitoring requirements may require further regulatory guidance and stronger internal compliance frameworks, with the framework's ultimate impact depending on banks' participation and underwriting appetite.

SEBI expands permissible borrowing utilisation for highly leveraged InvITs

Circular amending the SEBI (Infrastructure Investment Trusts) Regulations, 2014

The Securities and Exchange Board of India (SEBI) has operationalised the March 2026 amendments by permitting Infrastructure Investment Trusts (InvITs) with net borrowings exceeding 49% of asset value (within the overall 70% leverage limit) to utilise fresh borrowings not only for acquisition and development of infrastructure assets, but also for:

- Capital expenditure, including capacity expansion, asset upgrades and efficiency improvements

- Major maintenance expenditure under concession arrangements

- Refinancing of eligible acquisition or development debt (limited to outstanding principal).

Market implications

- While the amendment appears incremental, it addresses a practical constraint in the InvIT financing framework. Mature infrastructure assets require periodic capital expenditure, major maintenance, and active liability management throughout their operating life. Restricting fresh borrowings solely to acquisitions often compelled InvITs to fund these requirements from internal accruals, affecting capital allocation and distribution policies.

- The revised framework is likely to be particularly relevant for road-sector InvITs, where concession agreements require significant periodic maintenance expenditure. By permitting debt funding for such obligations, SEBI has recognised the operational realities of infrastructure ownership rather than treating all post-acquisition expenditure as routine operating costs. The refinancing flexibility may also facilitate more efficient liability management as InvITs replace higher-cost legacy borrowings in a changing interest-rate environment.

- For lenders, however, the expanded end-use of borrowings will require greater emphasis on monitoring rather than merely extending credit. Financing documentation, disbursement conditions, and end-use verification mechanisms will assume greater importance, particularly for capital expenditure, maintenance, and refinancing transactions. Existing security structures and inter-creditor arrangements may also require review to ensure continued compliance with concession requirements and financing covenants.

RBI modernises the regulatory framework for authorised forex dealers

The Reserve Bank of India (RBI) has recently notified the consolidated regulatory regime governing Authorised Dealers (ADs), Full-Fledged Money Changers (FFMCs) and Forex Correspondents (FxCs), superseding the earlier fragmented authorisation framework (AP Regulations).

These Regulations significantly modernise India's foreign exchange authorisation framework by consolidating previously fragmented requirements into a single regulatory regime. The framework provides greater clarity on eligibility, permitted activities, governance and compliance obligations, while introducing streamlined authorisation procedures and an appeal mechanism.

Key changes

- Comprehensive authorisation framework: No person may act as an authorised person without obtaining authorisation from the RBI, and all fresh applications are required to be submitted through the Platform for Regulatory Application, Validation And Authorisation (PRAVAAH) portal.

- Revised categorisation of ADs: The AP Regulations provide for 3 categories of ADs (AD Category-I, AD Category-II and AD Category-III), each with distinct eligibility criteria and permitted activities.

- Expanded activities: AD Category-II entities may now undertake all non-trade current account transactions permissible under FEMA (other than gifts and donations) and foreign trade transactions up to INR 25 lakh per transaction.

- Introduction of AD Category-III: A new category (AD-III) has been introduced for entities undertaking foreign exchange activities incidental to their principal business or intending to offer innovative products and services involving foreign exchange transactions.

- Revised eligibility criteria: The AP Regulations prescribe eligibility conditions relating to corporate form, object clauses, net worth, financial services experience and fit-and-proper requirements for promoters, directors and key managerial personnel.

- Enhanced governance requirements: At least 50% of the directors and key managerial personnel of an applicant are required to possess qualifications and experience in the financial services industry.

- Directorate of Enforcement clearance framework: Applicants under investigation by the Directorate of Enforcement may continue to seek authorisation subject to prescribed no-objection certificate and declaration requirements.

- Net worth and turnover thresholds: The AP Regulations introduce minimum net worth requirements and ongoing annual forex turnover thresholds for specified categories of authorised persons.

- Validity and continuity of authorisation: Authorisations shall remain valid until revoked or surrendered, with authorisations granted to banks and Non-Banking Financial Companies (NBFCs) remaining co-terminus with their banking licence or certificate of registration.

- Enhanced compliance obligations: Authorised persons are required to comply with prescribed reporting, commencement of business, fit-and-proper and change-in-control requirements on an ongoing basis.

- Appeal mechanism: Applicants whose applications are rejected and authorised persons whose authorisations are revoked may appeal to the designated appellate authority within the prescribed timelines.

- Forex Correspondent framework: AD Category-I and AD Category-II entities may appoint FxCs under a principal-agent model for undertaking specified money-changing and remittance-related activities.

- Strengthened oversight of FxCs: The AP Regulations impose governance, reporting, outsourcing, customer protection, and operational oversight obligations on principals engaging FxCs.

- Phase-out of franchisee model: Fresh franchisee arrangements are prohibited and existing franchisee arrangements are required to be discontinued within 2 years from the commencement of the AP Regulations, with an option to transition into the FxC framework.

While these Regulations are an important step towards modernising India's foreign exchange authorisation framework, the enhanced governance, fit-and-proper, reporting and turnover requirements may increase compliance costs, particularly for smaller and newer market participants. The transition from the franchisee model to the FxC framework may also require operational and contractual restructuring by existing participants. Further clarity may be beneficial regarding the interaction of the AP Regulations with other RBI-regulated cross-border payment frameworks and the authorisation of innovative foreign exchange products under the AD Category-III regime. The overall impact of the framework will depend on its practical implementation and market adoption.

CSR regime aligned with the Social Stock Exchange framework through ZCZP recognition

Companies (Corporate Social Responsibility Policy) Amendment Rules, 2026

Though the Securities and Exchange Board of India (SEBI) had provided a structure for Zero Coupon Zero Principal (ZCZP) instrument issuances, corporate boards seeking to provide for and support registered Non-Profit Organisations (NPOs) through India’s Social Stock Exchange (SSE) faced uncertainty as to whether investments in ZCZP instruments could be considered as Corporate Social Responsibility (CSR) expenditure under the Companies Act, 2013 (Act).

To ensure the treatment of investments in ZCZP instruments issued by eligible NPOs on the SSE as valid CSR expenditure, the Ministry of Corporate Affairs (MCA) has amended the Act and the underlying CSR Rules, 2014, aligning the company law and capital markets frameworks.

Key changes

- Statutory recognition: Clause xiii has been introduced under Schedule VII, pertaining to Section 135 of the Act, providing for ‘subscription to ZCZP instruments on the SSE’ as a legitimate CSR activity.

- New definitions of NPO and ZCZP instrument: The definition of NPO under Regulation 292A(e) of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018, has been adopted. This includes charitable trusts, societies, Section 8 companies, and all other organisations that work for social welfare. Any future SEBI changes to NPO eligibility will automatically flow into the CSR regime, ensuring continued regulatory consistency. A ZCZP instrument has been defined as a security issued by an NPO registered on the SSE segment of any recognised stock exchange.

- Amended implementation process: Rule 4A has been introduced to outline the practical process for implementing CSR through ZCZP instruments. Further, Rules 4(5) and 4(6) – which exclude employee-only benefit activities from qualifying as CSR and prescribe limits on CSR capacity-building expenditure, respectively – have been made applicable to maintain the same governance procedures.

Conditions and limits on implementing CSR through ZCZP instruments under Rule 4A

- Investment cap and time-bound utilisation: The maximum percentage of the firm’s annual CSR expense spent on acquiring instruments through ZCZP is limited to 10%. This is to ensure that the SSE option does not act as an alternative to traditional CSR expenditures, but only as a complementary form. In addition, the NPO must complete the funding within 3 financial years following issuance of the instrument.

- Clawback of unspent funds and accountability: Rule 4A(3)(b) states that on the completion of the listing of a ZCZP instrument, whether through project completion, delisting, or otherwise, all funds not utilised by the NPO shall be transferred to a Schedule VII fund, and a compliance report will be made out to SEBI. This is done to ensure that all undeployed CSR funds are maintained within the CSR ecosystem.

- Impact assessment exemption with continued disclosure obligations: Organisations that subscribe to ZCZP funds are not required to undertake independent impact assessment, based on Rule 7, due to existing requirements by the NPO for disclosing, reporting, and auditing the utilisation of funds. Nevertheless, ZCZP spending is required to be reported in the Board's Report, Annual CSR Report, and Form CSR-2 filed with the Registrar of Companies (ROC).

Recent reforms have enhanced the attractiveness of ZCZP instruments by lowering the minimum application size to INR 1000 while retaining the minimum issue size of INR 50 lakh. Although over 100 NPOs had been listed on the SSE by early 2026, fundraising remained limited due to the absence of CSR recognition. Given that CSR expenditure reached INR 34,909 crore in FY 2023-24, the new framework allowing up to 10% of CSR funds to be deployed through ZCZP instruments could unlock more than INR 3,500 crore annually for the sector.

Though the exemption from the requirement of an independent impact assessment will ease the compliance process, corporations will still have the responsibility of conducting due diligence in confirming the registration of the NPO for the SSE, looking at the fundraising document and confirming that the project conforms with Schedule VII. The SSE option seems to suit only the bigger, well-governed NPOs, which can provide SEBI's information needs, and the restriction on the percentage implies that it will not become a dominant option for CSR activity.

IBBI strengthens creditor participation and transparency under the CIRP framework

IBBI (Insolvency Resolution Process for Corporate Persons) (Amendment) Regulations, 2026

The Insolvency and Bankruptcy Board of India (IBBI) has notified amendments to the IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations) to strengthen creditor participation, improve transparency in insolvency proceedings, refine valuation processes, and enhance accountability in resolution outcomes.

Key amendments

- Regulation 16-E | Non-banking creditors in the Committee of Creditors (CoC)

- If creditors other than banks or public financial institutions hold more than 66% of the voting power in the CoC, then the Resolution Professional (RP) will have to invite the 5 largest unrelated operational creditors to CoC meetings, including the 3 largest Government creditors/statutory authorities (like tax departments) based on the amount owed.

- These invited creditors can attend and observe but cannot vote.

- Any comments or observations they give must be written in the meeting minutes.

- Regulation 28-A | Transfer of guarantor’s assets

- If a creditor has already taken possession of a guarantor’s asset (personal or corporate), the RP can propose to include that asset in the insolvency process of the corporate debtor.

- The proposal should include a description of the asset, along with the estimated value by a registered valuer, as well as consent or approval for transfer from the creditor/guarantor’s creditor.

- If the CoC approves the transfer, then the RP will have to disclose it in the Information Memorandum, and ensure the resolution plan explains how proceeds will be distributed.

- Regulation 28-B | When the Corporate Debtor (CD) is a corporate guarantor: If the corporate debtor is a corporate guarantor, i.e., it gave a guarantee for another company, its RP will have to coordinate with the RP of the main debtor, the company for which the guarantee was given, about asset transfer.

- Regulation 31-B | Insolvency costs and assessment report

- The RP will have to present all Corporate Insolvency Resolution Process (CIRP) costs incurred till the first CoC meeting, along with the reasons for those costs, for CoC approval.

- After the first meeting, all CIRP costs will require prior CoC approval.

- The RP will also have to prepare a Going Concern Assessment Report (GCAR) covering expected income, expenses, cash flows, working capital needs, and risks if the business continues or stops.

- In the first meeting, the CoC will review the report and decide whether to continue the CD’s operations, as well as the scope and duration of such operations.

- At each meeting, the RP will have to:

- Show estimated income, expenses, and cash flow till next meeting

- Get approval for future costs

- Show actual costs v. previously approved estimates

- Regulation 39 | Approval of resolution plan: The CoC will have to record its decision and reasons on:

- Is each resolution plan practical and workable?

- How much money are creditors likely to actually recover under the plan compared with fair value and liquidation value?

- Was enough effort made to get the best possible plan or not?

- Regulation 40-E | Dissolution of the CD

- The CoC, with 66% approval, may seek dissolution of the CD during CIRP if the assets are too low to fund the CIRP/liquidation costs and cannot be realistically sold in liquidation.

- When intimating the Adjudicating Authority, the RP must include an explanation showing that continuing the CIRP or starting liquidation will not be economically beneficial.

- Regulation 40-F | Restoration of CIRP

- The CoC may request the restoration of CIRP before a liquidation order is passed, along with reasons and a proposed timeline for its completion.

- Regulation 40-E | Dissolution of the CD

- The CoC, with 66% approval, may seek dissolution of the CD during CIRP if the assets are too low to fund the CIRP/liquidation costs and cannot be realistically sold in liquidation.

- When intimating the Adjudicating Authority, the RP must include an explanation showing that continuing the CIRP or starting liquidation will not be economically beneficial.

- Regulation 40-F | Restoration of CIRP

- The CoC may request the restoration of CIRP before a liquidation order is passed, along with reasons and a proposed timeline for its completion.

Can housing societies be treated as promoters under RERA?

Shri Sai Vishram Co-operative Housing Society Ltd v. Ninad Padmakar Paralkar

The Bombay High Court has recently clarified that a cooperative housing society may be classified as a ‘promoter’ under the Real Estate (Regulation and Development) Act, 2016 (RERA) where it derives substantial commercial benefits from a redevelopment project.1

The dispute arose from a redevelopment project in Thane where the original developer failed to complete construction and was subsequently replaced by a new developer. Under the revised redevelopment arrangement, the housing society (Society) was entitled to a 50% share of the constructed area along with a corpus fund of INR 3 crore. When the project stalled and homebuyers did not receive possession, several allottees approached MahaRERA seeking refunds with interest. The Society argued that it had no contractual relationship with the affected purchasers, who had originally booked flats with the erstwhile developer, and therefore could not be held liable for their claims.

The Court upheld the findings of MahaRERA and the Maharashtra Real Estate Appellate Tribunal, holding that the Society’s role extended well beyond that of a passive landowner. In assessing promoter status, the Court looked at the overall commercial arrangement rather than the labels used in the agreements, and noted that the Society had actively facilitated the redevelopment, participated in transitioning the project to the new developer, and stood to gain significant commercial benefits through area sharing and monetary consideration. Given this direct economic interest in the project, the Court concluded that the Society fell within RERA’s broad definition of a ‘promoter’ and could be held jointly and severally liable alongside the developer for obligations owed to homebuyers.

The ruling ensures that entities benefiting commercially from a project cannot avoid accountability when things go wrong, and housing societies involved in profit-sharing or area-sharing arrangements may face promoter-level obligations under RERA.

Footnotes

1 Writ Petition No. 2221 of 2025

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.