Nexdigm is a privately held, independent global organization that helps companies across geographies meet the needs of a dynamic business environment. Our focus on problem-solving, supported by our multifunctional expertise enables us to provide customized solutions for our clients.

within Employment and HR, Family and Matrimonial, Media, Telecoms, IT and Entertainment topic(s)

The GST Council has been proactively taking up representations

made by various industry stakeholders to remove hardships and

increase compliance. Rulings by Authority for Advance Rulings (AAR)

have also begun providing clarity and direction on various

ambiguous provisions. With this, the GST regime could stabilize in

the coming months. Furthermore, the decision to simplify

compliances in the last GST Council meeting should also hasten this

process.

Top Trends

E-Way Bill on the intra-state

movement of goods to be implemented across all remaining states by

3 June 2018.

A centralized depository of rulings

passed by AARs across all states to be created on the GST

Council's website.

Few key points that businesses should

ensure while finalizing their balance sheets: Reconcile sales

according to books of accounts with GSTR-1 and GSTR-3B.

Input tax credit according to books

match with electronic credit ledger on the GST portal.

Input tax credit claimed matches with

GSTR-2A.

Certain functionalities have been

added to the GST portal:

Taxpayers can make Input Tax Credit

(ITC) reversal under one head without affecting the other head,

e.g., reverse only CGST/SGST without affecting the other.

Exporters claiming a refund of

accumulated ITC would now be required to provide invoice-wise

details of shipping bill, Export General Manifest (EGM), Bank

Realisation Certificate (BRC) /Foreign Inward Remittance

Certificate (FIRC), etc. while filing the refund application. A

template has been provided for this purpose.

Judicial Pronouncements

Issue

Ruling

SKP

Comments

Whether hotel

accommodation and restaurant services provided to the employees and

guests of SEZ units, be treated as a supply of goods and services

to such SEZ units, and therefore, zero-rated?

[AAR, Karnataka]

Under Section 12(3)(b) of the IGST Act, 2017, the place of

supply of services by way of lodging accommodation by a hotel,

should be the location at which the immovable property (hotel) is

located, i.e., outside SEZ in this case.

Furthermore, under Section 12(4) of the IGST Act, 2017, the

place of supply of restaurant and catering services should be the

location where the services are actually performed, i.e., outside

SEZ in this case.

The services are not part of authorized operations of SEZ, as

required under CGST Rules, 2017.

Under Section 16(1) of the IGST Act, 2017 supply of services to

an SEZ unit is to be treated as 'zero-rated supply.'

Furthermore, 'accommodation services' are covered in

uniform list of services as default authorized services for an SEZ

unit, as conveyed by the Ministry of Commerce & Industry dated

2 January 2018.

It is a well-settled principle of law that a specific provision

shall prevail over a general provision.

In view of the above, there is a possibility that the decision

of the AAR could be subject to reconsideration at higher appellate

courts.

Whether a supply of UPS

along with battery can be treated as composite supply?

[AAR, West Bengal]

A standalone UPS and a battery can be separately supplied in

retail set up.

The contract for the supply of a combination of UPS and

battery, if not built as a composite machine, is not

indivisible.

The said goods are not naturally bundled and cannot be treated

as a composite supply.

The said supply should be considered as mixed supply as they

are supplied under a single contract at a combined single

price.

The AAR has placed importance on whether the products are

'naturally bundled.'

The applicant admitted that UPS and the battery were being sold

separately as well. The AAR pointed out that the products are

capable of being supplied as part of separate contracts and hence

cannot be considered as composite supply.

Businesses involved in supplying more than one product bundled

together should carefully evaluate whether their supply constitutes

a mixed or composite supply.

Whether supply of

turnkey Engineering, Procurement and Construction (EPC) contract in

case of a solar power plant, wherein both goods and services are

supplied, should be construed as a composite supply or a works

contract?

[AAR, Maharashtra]

In a turnkey contract, the contractor is expected to perform

all activities from engineering to commissioning.

Furthermore, on examining the various clauses of the agreement,

it can be seen that the liability of the contractor doesn't end

with the procurement of materials but extends till successful

commissioning of the system, like in a 'works

contract.'

Viewing the principles laid down by the Supreme Court in

various cases in light of the facts of the present case makes it

clear that there is an inherent element of permanency to the solar

power plant, and hence it is classifiable as immovable

property.

Consequently, the said contract would be classified as a

'works contract' under Section 2(119) of the CGST Act,

2017, as it results in the creation of immovable property.

The AAR examined the substance of the contract entered into by

the parties as opposed to the drafting of the contract as

constituting a separate supply of goods and services. The AAR ruled

that the invoicing pattern, the language of the agreement, etc. is

secondary to the substance of the transaction being

undertaken.

In view of this ruling, the question whether a transaction

qualifies as a works contract/results in the creation of immovable

property has acquired further importance under GST regime.

Whether liquidation

damages should be subjected to GST?

[AAR, Maharashtra]

Liquidated damages would be subject to GST as the same are

towards the tolerance of the delay caused by the contractor which

will be covered as a 'supply of services' under clause (e)

of Para 5 of the Schedule II to the CGST Act, 2017.

Even though such liquidated damages are presented in the form

of a deduction from the payments to be made to the contractor, they

are the income of the applicant/contractee towards the supply of

service.

The revenue authorities have considered liquidated damages as

consideration towards the supply of service of 'tolerance'

of non-performance/delayed performance under the erstwhile service

tax law as well.

However, whether a clause for liquidated damages is for

tolerance of an act or actually inserted to act as a deterrence for

non-performance/delayed performance is open to interpretation.

In view of the above, this ruling by the AAR is bound to open a

Pandora's Box in terms of taxability under GST of similar

transactions.

It is to be noted that an Advance Ruling is binding only on

the applicant who had sought it and the concerned jurisdictional

authority, i.e., an Advance Ruling is specific to an applicant and

shall not be applicable to other taxpayers facing similar

issues.

However, the above mentioned Advance Rulings provides

clarity about the issues being faced and provide persuasive value

in matters before the tax authorities.

Upcoming GST Due Dates

Form

Applicable

to

Period

Due

Date

GSTR-1 (monthly)

Taxpayers with annual

aggregate turnover more than INR 15 million

May 2018

10 June 2018

GSTR-3B

All registered

taxpayers

May 2018

20 June 2018

GSTR-5

Non-resident taxable

persons

May 2018

20 June 2018

GSTR 5A

Online Information and

Database Access or Retrieval (OIDAR)

May 2018

20 June 2018

GST TRAN-2

Taxpayers not registered

under pre-GST regime willing to claim transitional credit

Six tax periods for

which the scheme is applicable

30 June 2018

OTHER KEY ASPECTS

GST from a Macro Perspective

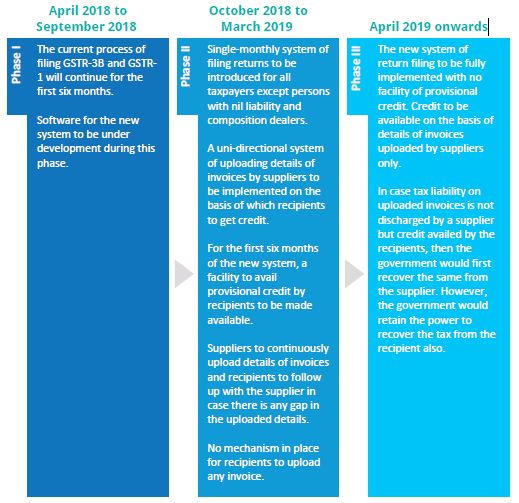

Return filing process

The GST Council in its 27th meeting held on 4 May 2018 has

approved the simplified returns filing system which is bound to be

implemented in a phased manner as follows:

Revenue collections

The GST revenue exceeded the INR 1 trillion threshold for the

first time in April 2018 with gross GST collections standing at INR

1.03 trillion. The gross GST revenue for the month of May 2018 has

dropped to INR 0.94 trillion. However, this is more than t e

average gross GST revenue for the period of July 2017 to March 2018

which stood at INR 0.89 trillion.

e-Way Bill

Post the smooth rollout of the e-Way Bill system for inter-state

movement of goods, the government is gradually implementing the

system for intra-state movement of goods in the following

manner:

e-Way Bill – A snapshot

More than 22.6 million e-Way Bills generated

in May 2018 (up to 21 May 2018).

More than 50 million e-Way Bills generated

till date.

On an average 2 million e-Way Bills are being

generated every day.

State-wise GST officers have been appointed to resolve e-Way

Bill related grievances.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.