- within Tax, Real Estate and Construction, Food, Drugs, Healthcare and Life Sciences topic(s)

- with readers working within the Law Firm industries

The Central Board of Excise and Customs (CBEC) vide Circular No. 46/2017-Cus dated 24 November 2017 (Circular) has clarified that the sale / transfer of goods lying in a Customs Bonded Warehouse (in-bond transfer) would attract (i) the integrated goods and services tax (IGST) at the time of transfer; and (ii) customs duty comprising of basic customs duty and IGST at the time of removal of such goods from the warehouse. The relevant extract from the clarification is set out below:

"It may be noted that as per sub-section (2) of section 7 of the IGST Act, any supply of imported goods which takes place before they cross the customs frontiers of India, shall be treated as an inter-State supply. Thus, such a transaction of sale/transfer will be subject to IGST under the IGST Act. The value of such supply shall be determined in terms of section 15 of the CGST Act read with section 20 of the IGST Act and the rules made thereunder, without prejudice to the fact that customs duty (which includes BCD and applicable IGST payable under the Customs Tariff Act) will be levied and collected at the ex-bond stage.

Thus, in respect of goods stored in a customs bonded warehouse, there is a possibility that certain cases may involve an additional taxable event, if a transfer of ownership of warehoused goods takes place between the importer and another person, before clearance of the goods, whether for home consumption or for export."

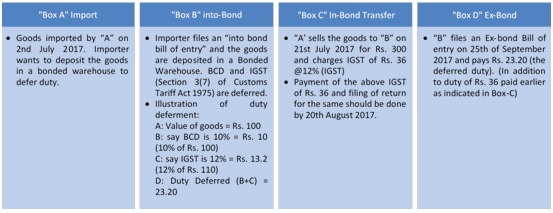

To remove any doubt, the circular provides for the following illustration:

In simpler terms, imported goods procured under in-bond transfer would be subjected to double taxation, first under IGST Act, 2017 and thereafter, under the Customs Act, 1962.

Comment

The importer making in-bond transfer would not be eligible to claim any input tax credit as IGST paid on the ex-bond bill of entry would be filed by the customer. Importers making in-bond transfer of bonded goods are now saddled with additional IGST liability, and tax authorities will proceed to recover the same from the importer if not already paid on in-bond transfer of goods made on or after 1 July 2017.

The Circular takes a position completely contrary to what the CBEC has clarified on taxability of high sea sale transactions in the recent past. For the ease of reference, the CBEC Circular No. 33/2017 dated 1 August 2017 is set out below:

- high sea sales of imported goods are akin to inter-state transactions and subject to IGST;

- IGST on high sea sale(s) transactions of imported goods (whether one or multiple) shall be levied and collected only at the time of importation;

- IGST on imported goods is to be levied under section 3(12) of the Customs Tariff Act, 1975.

Since In-bond transfer of imported goods are akin to high sea sales transactions, it should be treated equally. Even legal provisions under the IGST Act don't warrant such interpretation. We believe that this circular has been issued without due appreciation of legal provisions under the goods and services and customs law and the double taxation of such transactions is going to be highly litigated in the coming days.

The content of this document do not necessarily reflect the views/position of Khaitan & Co but remain solely those of the author(s). For any further queries or follow up please contact Khaitan & Co at legalalerts@khaitanco.com