- within Family and Matrimonial, Strategy and Privacy topic(s)

- with readers working within the Law Firm industries

DIRECT TAX

Some of the major proposals in the Finance Bill, 2016 (Bill) are discussed below:

TAX RATES

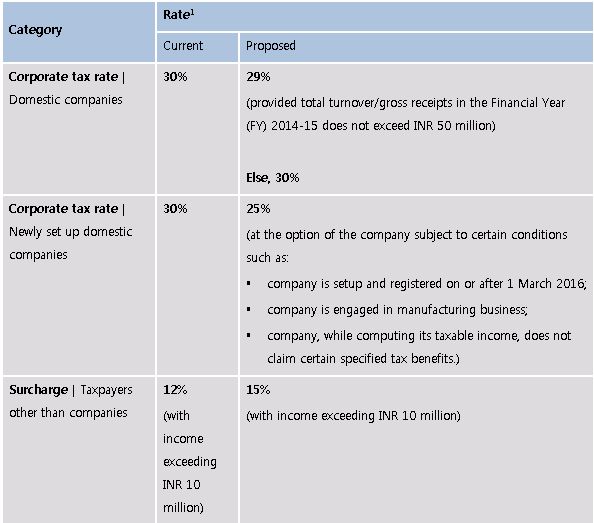

In line with the phased reduction in corporate tax rate, as announced by the Finance Minister (FM) last year, the Bill proposes to reduce the corporate tax rate from 30% to 29% for certain small domestic companies.

The corporate tax rate and rates of surcharge are proposed to be changed as follows:

The revised rates are proposed to be effective for FY 2016-17.

There are no changes with respect to the following:

- slab rates for resident individuals;

- corporate tax rate applicable to foreign companies;

- the rate of surcharge applicable to domestic companies and foreign companies;

- the rate of education and higher education cess applicable to all taxpayers;

- there are no changes in the Dividend Distribution Tax (DDT) rates; and

- the rate of Minimum Alternate Tax (MAT) and Alternate Minimum Tax (AMT).

DIVIDENDS OVER INR 1 MILLION TAXABLE FOR NON-CORPORATE RESIDENT TAXPAYERS

Currently, dividends are subject to a DDT of 15% in the hands of the company and are tax exempt in the hands of the shareholders of the company (irrespective of whether they are resident or non-resident).

The Bill proposes that dividends received by resident taxpayer being either an individual, Hindu Undivided Family or a firm in excess of INR 1 million will be taxed at the rate of 10% in the hands of the recipient on a gross basis.

This amendment is proposed to be effective from FY 2016-17 onwards.

STT INCREASED WHERE OPTION NOT EXERCISED

Currently, the rate of securities transaction tax (STT) on the sale of an option in securities where the option has not been exercised is 0.017% of the option premium.

The Bill proposes to increase this rate to 0.05%.

This amendment is proposed to be effective from 1 June 2016.

CLARIFICATION REGARDING THE TAX RATE ON SALE OF SHARES OF A PRIVATE LIMITED COMPANY

Currently, in case of non-resident taxpayers long term capital gains (LTCG) from transfer of 'securities' are taxed at the rate of 10%. The term 'securities' has been assigned the same meaning as ascribed to it under the Securities Contracts (Regulations) Act, 1956 (SCRA).

Under SCRA, in certain rulings the courts have held that shares of a private limited company are not 'securities'. Consequently, the applicability of the concessional tax rate of 10% to LTCG from transfer of shares of a private limited company was a grey area. Resultantly such gains are considered as taxable at the higher rate of 20%.

This result was unintended and hence, to address this, the Bill has extended the concessional tax rate of 10% on LTCG arising from transfer of shares of a company in which the public are not substantially interested (essentially a closely held company, including a private company), in addition to 'unlisted securities'.

This amendment is proposed to be effective from FY 2016-17.

This amendment is a welcome move and would put to rest the controversy surrounding the taxability of gains from the sale of shares of private limited companies.

Further, the FM in his budget speech had proposed that shares of unlisted companies will be treated as long term capital asset if they are held for a period of more than two years as against three years under the existing provisions of the Income-tax Act 1961 (IT Act). However, the Bill is silent on this aspect.

This seems to be an unintentional miss and may be included at the time of enactment of the Bill.

PAVING THE WAY FOR REDUCTION IN CORPORATE TAX

In line with the announcement made last year to reduce corporate tax rate in a calibrated manner coupled with withdrawal of investment and profit linked deductions and exemptions, the Bill proposes withdrawal of certain deductions and exemptions. Some of the major provisions are as under:

- sunset clause proposed such that no profit linked deductions will be available to units in Special Economic Zones (SEZs) where the SEZ units start their operations after 1 April 2020;

- no deduction would be available in relation to development, operation and maintenance of an infrastructure facility, development of SEZs and production of mineral and natural gas if the specified activities start after 1 April 2017;

- the weighted deduction of 150% of expenditure on eligible projects and skill development projects is proposed to be reduced to 100% from 1 April 2020;

- weighted deduction for expenditure on scientific research to be reduced to 150% from 175% and 200% (in certain cases) from 1 April 2017 and further reduced to 100% from 1 April 2020;

- accelerated depreciation restricted to 40% in a FY as against 100% which can be claimed currently for certain block of assets.

There are other weighted deductions also which are being phased out or reduced only to the amount of expenditure incurred by the year 2020.

As set out in the Tax Rates section of this newsflash, there are corresponding reductions in corporate tax rates to some extent. However, the full 1% reduction for all companies which was expected has not been proposed and it is a miss.

GO START A VENTURE!

TAX HOLIDAY FOR START-UPS

The Bill proposes to introduce various provisions for promoting investments into start-ups in India. An 'eligible start-up' would be eligible for a 100% tax holiday on its profits from an 'eligible business' for a period of any three consecutive years out of the initial 5 year period.

An eligible start-up is a 'company' which is incorporated on or after 1 April 2016 but before 1 April 2019, whose turnover does not exceed INR 250 million in a year and which holds a certificate of eligible business from the Inter-Ministerial Board of Certification. Further, an 'eligible business' would be a business which involves innovation, development, deployment or commercialisation of new products, processes or services driven by technology or intellectual property.

This amendment is proposed to be effective from FY 2016-17 onwards.

BENEFITS EXTENDED TO INVESTORS

Currently the law provides an exemption from LTCG arising to individuals and Hindu Undivided Family (HUF) from transfer of residential property (i.e. house or plot of land) if the amount of such gains are invested in equity shares of certain eligible companies.

The Bill proposes to extend the benefit of this exemption to investments made into equity shares of eligible start-ups as well.

Further, the Bill proposes to provide a scheme for exemption from LTCG if such gains are invested in the units of a fund, which will be notified by the Government of India (Government). However, this benefit would only be allowed for investments up to INR 5 million during a financial year.

These amendments are proposed to be effective for FY 2016-17 and onwards.

MAT: BIG WIN FOR FOREIGN COMPANIES

GOVERNMENT SETTLES MAT ISSUE FOR FOREIGN COMPANIES

Currently, the IT Act specifies that, in case of a company, MAT at the rate of 18.5% on book profit is applicable, if the tax payable on the total income of such company as computed under the IT Act is less than 18.5% of its adjusted book profits. The Finance Act, 2015, clarified that certain incomes arising to foreign companies are not subject to MAT, which begged the question – whether MAT was applicable on such income for previous years.

Ongoing tax controversies relate to whether foreign companies including Foreign Portfolio Investors (FPIs, erstwhile Foreign Institutional Investors) who do not have any place of business in India are subject to MAT for periods prior to 2015. To address the plummeting foreign investment, the Government constituted a High Level Committee to review the issue of applicability of MAT on FPIs. Thereafter, accepting the recommendations of the aforesaid Committee, the Government clarified that for the period commencing from 1 April 2001, foreign companies and FPIs are not subject to MAT so long as they do not have a place of business in India (either under the relevant Double Taxation Avoidance Agreement (DTAA) or the IT Act).

In order to codify the above developments, the Bill proposes that a foreign company shall not be subject to MAT where:

- the country of residence of the foreign company has entered into a DTAA with India, and such company does not have a permanent establishment (PE) in India in terms of the DTAA; or

- the country of residence of the foreign company has not entered into a DTAA with India, then such company is not required to seek registration in India under any applicable law.

This amendment is proposed to be retrospectively effective from FY 2000-01 onwards.

This puts to rest the controversy created by the issuance of notices by the tax department to many FIIs who earned income upon sale of their investments several years ago. This should help establish faith in the Government's commitment not to rake up controversies.

TAKING LEAPS TOWARDS BEPS OBJECTIVE

In pursuance of its commitment to introduce measures to curb Base Erosion and Profit Shifting (BEPS), India has adopted some of the recommendations of the Organisation for Economic Co-operation and Development (OECD) BEPS Action Plans. The Bill proposes to incorporate within the domestic tax laws, certain proposals from the BEPS recommendations, such as taxation of digital economy, transfer pricing documentation and Country-by-Country (CbC) reporting, for increased transparency and accountability in the taxation regime.

TAXATION OF DIGITAL ECONOMY (EQUALISATION LEVY)

Currently, domestic tax laws do not contain specific provisions for the taxation of transactions in the digital economy. The Bill proposes to introduce an 'Equalisation Levy' of 6% in respect of certain specified services involving payments greater than INR 0.1 million in the online marketing and advertising arena rendered by non-residents who do not have a PE in India (Service Provider). This levy is in the form of a withholding obligation on the payer.

These provisions are introduced as a separate chapter in the Bill, and not as a part of the IT Act. Currently, the Bill proposes to apply this levy only on B2B transactions between the Service Provider and:

- a resident, carrying on any business or profession in India; or

- a non-resident having a PE in India, being the service recipient.

The provisions of the Bill are proposed to not apply to transactions where a non-resident having a PE in India acts as a service provider, or where the transaction is not for the purpose of carrying out any business or profession. The former would be covered under the normal provisions of the IT Act. The Bill has also specified timelines for the deposit of this levy by the payer, failure to comply with which would attract penal provisions. This is defendable on proving reasonable cause for the non-deposit of the levy.

Interestingly, this equalisation levy is proposed to be introduced as a separate code, complete with the procedural aspects of its administration including its application, penalties, appeals and resolution of disputes. The provisions of the IT Act are not made applicable to the code, except as specifically provided. For instance, to address the issue of double taxation, it is proposed that an exemption from inclusion in total income under Section 10 of the IT Act be provided for such payment where the equalisation levy has been deducted. Further, where such a levy is not deducted by the payer, he will not be able to claim a deduction of expense for payments made for the specified services. Since, these provisions are not a part of the IT Act, provisions under Sections 90, 195, 197 of the IT Act are inapplicable, i.e. the payee may not take benefit of any reduced withholding obligations under any DTAA, or approach the tax authorities for a lower or nil withholding tax certificate etc. It is however, unclear whether the compliance requirements for payments to a non-resident will be applicable in such transactions.

This proposal is India's first step towards addressing tax leakage arising out of the lack of a statutory basis to tax digital economy transactions in concurrence with BEPS. One may expect to see a full-fledged code dealing with the taxation of digital economy transactions for services beyond the realm of advertising and marketing being introduced as is clear from the fact that the Bill provides that further services will be notified later.

These provisions will become effective upon notification from the Central Government.

TAXATION OF INCOME FROM 'PATENTS'

Currently, domestic tax laws do not contain any special regime for the taxation of patents. The Bill proposes to tax the income of any eligible taxpayer derived from royalties at the rate of 10% on a gross basis. The eligibility to claim this concessional rate of taxation is available to those taxpayers who are resident in India, and are the true and first inventors of the patents registered under the Patents Act, 1970 for the use of which they are receiving royalties.

Consistent with the 'nexus approach' under Action 5 of the BEPS recommendations, which confers the right to tax on that jurisdiction, where substantial research and development (R&D) activities are carried out, and with an aim to promote India as an R&D hub, this concessional regime of taxation of income derived from royalties, has been introduced. It is hoped that this would promote India as a centre for R&D and promote innovation.

This amendment is proposed to be effective from FY 2016-17 onwards.

CbC REPORTING

Consistent with the Action Plan 13 of the BEPS Report, and with an aim to develop rules relating to transfer pricing documentation, to enhance transparency of tax administration, CbC reporting has been introduced. The Bill proposes to ensure a robust transfer pricing analysis by mandating the maintenance of specified documents in specified forms being:

- a master file containing standardised information relevant for all multinational enterprises (MNE) group members;

- a local file referring specifically to material transactions of the local taxpayer; and

- a CbC report containing certain information relating to the global allocation of the MNE's income and taxes paid together with certain indicators of the location of economic activity within the MNE group.

The CbC report has to be submitted annually by the parent entity of an international group for each tax jurisdiction in which they do business, to the prescribed authority in its country of residence. The Bill proposes to impose the reporting regime on MNEs meeting a monetary threshold for consolidated group revenues of INR 50 billion approximately.

Separately, the Bill also proposes to impose the reporting obligation on the entities in India which belong to an international group, where the jurisdiction of the parent entity does not have an agreement for the exchange of CbC reporting or such country does not exchange such information with India. The Bill proposes to levy a penalty for failure and delay of CbC reporting, and the furnishing of inaccurate particulars in the CbC reports. However, a defendable claim for non-levy of penalty can be made on offering reasonable cause.

Given that India already has an aggressive transfer pricing regime, the introduction of CbC reporting consistent with the BEPS measures is a positive step towards accountability and transparency in structuring of transactions among MNE group entities, which will also be helpful in tackling any aggressive structuring for tax avoidance.

This amendment is proposed to be effective from FY 2016-17 onwards.

TAX INCENTIVES: TO HAVE AND TO HOLD

INTERNATIONAL FINANCIAL SERVICES CENTRE

The Government has shown its commitment to promote the development of International Financial Services Centres (IFSCs) into world class financial services hubs. It aims to do so by proposing some tax friendly measures in the IT Act with regard to capital gains tax, STT, MAT and DDT on the income of a unit located in the IFSC (where its income is earned in convertible foreign exchange).

The IT Act provides an exemption from payment of tax on LTCG arising from transfer of equity shares on which STT has been paid. Further, despite a corporate taxpayer not being subject to LTCG tax on sale of securities on a stock exchange, where STT is paid, it is required to pay MAT at the rate of 18.5%. Also, companies are required to pay DDT for distribution of profits to shareholders.

With a view to achieve the objectives for development of IFSCs, the Bill proposes the following provisions:

- exemption from tax on LTCG arising from transactions undertaken on a recognised stock exchange located in any IFSC and where the consideration is paid or payable in foreign currency, even if STT has not been paid on such transactions;

- corresponding amendments under the STT Act to exclude such transactions from the purview of STT and from the levy of commodities transaction tax; and

- where the income of a company located

in an IFSC is derived solely in convertible foreign exchange then:

- MAT will be levied at the rate of 9% compared to 18.5% in case of other companies in India; and

- dividends declared by such company out of its current income on or after 1 April 2017 will not attract DDT either in the hands of the company or the recipient of dividends.

IFSC has been assigned the same meaning as provided under the Special Economic Zones Act, 2005. The above amendment is proposed to be effective from FY 2016-17.

These are significant tax proposals, indicating the seriousness of the Government in promoting IFSCs in India.

COMPANIES TO BENEFIT FROM GRACE PERIOD ALLOWED BETWEEN ACQUISITION AND INSTALLATION OF NEW ASSET

Currently, the IT Act specifies that, manufacturing companies may avail an investment allowance at the rate of 15% on investments made in new assets such as plant and machinery exceeding INR 250 million so long as the acquisition and installation of the asset is undertaken in the same year.

The Bill proposes to do away with the requirement that the asset should be acquired and installed in the same year. The Bill proposes to allow companies to avail the allowance so long as the assets are installed on or before 31 March 2017. Further, the deduction shall be allowed in the year of installation (of the new asset).

The introduction of the grace period for installation signifies that the Government is in sync with ground issues faced by the manufacturing sector and is a welcome move.

This amendment is proposed to be made retrospectively effective from FY 2015-16 onwards.

RUPEE DENOMINATED BONDS

Recently, the Reserve Bank of India has permitted Indian companies to issue rupee denominated bonds outside India as a measure to enable them to raise funds from outside India.

Taking cognisance of the fact that the non-resident investor in such bonds bears the risk of currency fluctuation, the Bill proposes that if there is any appreciation (gains) of rupee between the date of issue of bond and date of redemption against the foreign currency in which the investment is made, the same shall be excluded from the total sales consideration for the purposes of computing the capital gains. The amendment is proposed to be effective from FY 2016-17.

Whilst this is a welcome provision, the Bill is silent on extending concessional withholding tax of 5% on the interest coupon on such bonds, as clarified in the press release issued by the Government on 29 October 2015. It is hoped that this is an unintended lapse and will be rectified by way of amendment to the Bill.

INCENTIVISING HOUSING FOR ALL

The Bill seeks to allow taxpayers engaged in the business of developing and building housing projects a 100% deduction of the profits subject to the following principal conditions:

- The housing project is approved by the competent authority before 31 March 2019 and is completed within 3 years from the date of such approval;

- The project plot is a minimum of 1000 sq. mtrs where the project is in the vicinity of metros (2000 sq. mtrs otherwise); and

- Once a residential unit is allotted to an individual, no other unit will be allotted to the spouse or minor children of the individual in the same project.

An additional deduction for interest paid to the extent of INR 0.05 million has been proposed for first home buyers to give a boost to the real estate sector. This is in line with the Government's commitment to provide affordable housing for all and is proposed to be effective for FY 2016-17 and onwards.

ECONOMIC ACTIVITIES UNDERTAKEN IN STRATEGIC SECTORS: NO TAX FOR NON-RESIDENT

Currently, the IT Act specifies source rules of taxation whereby income arising to a non-resident through or from a 'business connection' in India is taxed in India. Essentially, a non-resident's 'real and intimate' economic nexus with India allows India to tax income arising from such connection.

The Bill proposes to introduce tax exemption in two sectors from such levy, both targeted to boost economic activity in India – viz. storage and sale of crude oil in a facility in India and the mere display of rough diamonds in a special notified zone.

The Bill proposes to exempt a foreign company's income on account of storage and sale of crude oil in a facility in India so long as (i) the Government is either party to the contractual agreement to store and sell crude oil or has approved of such agreement and (ii) the foreign company along with the agreement has been notified by the Government.

Similarly, income arising to foreign companies engaged in the business of mining diamonds that merely display uncut or un-assorted diamonds in any notified special zone in India shall not be deemed to accrue or arise in India. In the absence of such a specific provision, merely displaying the diamonds without undertaking a sale may establish a business connection in India and consequently may trigger Indian tax incidence.

The above exemptions are certainly a shot in the arm for foreign companies as well as accord the twin benefit of furthering India's interest to maintain and build reserves for crude oil which would help stabilise prices for Indian oil companies.

Though the Memorandum provides that the amendment is proposed to be effective retrospectively from FY 2015-16 onwards, the Bill is silent on the same. It is expected that foreign companies shall, unlike other times, welcome this beneficial retrospective change.

To continue reading this article, please click here.

Footnote

1 Please note that the rates mentioned in the document are exclusive of applicable surcharge and education cess.

The content of this document do not necessarily reflect the views/position of Khaitan & Co but remain solely those of the author(s). For any further queries or follow up please contact Khaitan & Co at legalalerts@khaitanco.com