In the past one year, the impact of Covid-19 pandemic has been severely stressful on the Indian economy. There is no doubt that the insolvency procedure under the Insolvency and Bankruptcy Code is one of the major hit regions. To combat with this predicted low fall in the economy, one of the initiatives by the Government is introduction of Pre-Pack Insolvency Resolution for MSME sector under the Insolvency and Bankruptcy Code. The basic idea behind the making of Pre-Pack Insolvency is to save the time period taken in the whole resolution process, consensual restructuring and save judges from the burden of cases. In June, 2020 the Government of India had formed a subcommittee of the Insolvency Law Committee to provide the framework of pre- pack insolvency under the basic Insolvency and Bankruptcy Code structure and the Ordinance for the same was recently promulgated by the Government of India in the month of April, 2021 i.e. the Insolvency and Bankruptcy (Amendment) Ordinance, 2021. THE PPIRP is for the Micro, Small and Medium Enterprises (MSMEs) whose default is not more than INR 1 crore. According to the revised definition of MSMEs, the captial investment in the Micro Enterprises shall not be more than 1 crore and the turnover shall not be more than 5 crores. For Small Enterprises, the capital investment shall not be more than 10 crores and turnover shall not be more than 50 crores and for Medium Enterprises, the capital investment shall not be more than 50 crores and the turnover shall be less than or equal to 250 crores. The revised definition of the MSME sector, therefore, covers almost 70% of the Indian Industries.

A Pre-Pack is a kind of resolution of the debt of a distressed company through an agreement between secured creditors and investors instead of public bidding process. Pre-Pack gives chance to mutually negotiate the terms of restructuring and the involvement of the tribunal/ adjudication authority can be at the final stage for implementation of the Base Resolution Plan. So, it is hybrid in nature as it opens up space for negotiation and cooperation of the restructure plan between the financial creditors and corporate debtors and at the same time, does not even lose the essence of court/tribunal intervention in implementing that plan. The approval of 66% of financial creditors is needed for a Resolution Plan to be submitted to the Adjudicating Authority for approval.

Even though the Pre Pack Insolvency Resolution Process ('PPIRP') is part of the Insolvency and Bankruptcy Code, the difference in its resolution process and that of Corporate Insolvency Resolution Process(CIRP) are numerous. Some of them are:

- In the Pre-Packaged Insolvency, only the Corporate Debtor can initiate the PPIRP1while on the other hand the CIRP can be initiated by the Corporate Debtor, a Financial Creditor or an Operational Creditor.

- The maximum time limit for completion of PPIRP is 120 days2 where as in the case of CIRP it is 270 days i.e. 180+90 days and 330 days in special cases.

- The minimum threshold value of default amount for filing an application for PPIRP is Rs. 10 Lakhs while for CIRP, as of now is Rs. 1 crore.

- Before the initiation of PPIRP, the Corporate Debtor has to present the base resolution plan to the financial creditors.3 In CIRP, there is no such process.

- After the commencement of PPIRP, the Resolution Professional has to submit the resolution plan approved by the Committee of Creditors to the Adjudicating Authority within 90 days.4 In CIRP, there is no timeline as such from the insolvency commencement date though the process needs to be completed within 180 days.

- During the PPIRP, the existing management handles the affairs of the Corporate Debtor5 and in case of the CIRP, the management and control of the Corporate Debtor is in the hands of the Resolution Professional.

Major amendments made by the Insolvency and Bankruptcy (Amendment) Ordinance, 2021

- Definitions

- Section 5 (2A): "Base Resolution Plan" means a resolution plan provided by the Corporate Debtor under sub section 4 of Section 54A.

- Section 5 (23A): "Preliminary Information" memorandum submitted by the Corporate Debtor under clause (b) of sub-section (l) of Section 54G

- Section 5 (23B): "Pre-Packaged Insolvency Date" means the date of admission of application for initiating the pre-packaged insolvency resolution process by the Adjudicating Authority.

- Section 5 (23D): "pre packaged insolvency resolution process period" includes the period from the date of acceptance of application for initiation of the PPIRP till the order passed by Adjudicating Authority for acceptance / rejection of the plan.

- Section 11A: Preference of disposal of application under Section 54C and under Section 7 or 9 or 10 of IBC.

- Section 67A: creates an offence for penalizing an officer of the Corporate Debtor who manages the Corporate Debtor during PPIRP with intent to defraud its creditors.

- Section 77A: provides for punishment for offences related to the PPIRP.

- A new Chapter III A has been added comprising of Section 54A to Section 54P. It describes about the whole scheme of Pre-Packaged Insolvency Resolution Process including how the PPIRP is initiated, duties and powers of Resolution Professional before and during the PPIRP, management of affairs, committee of creditors, consideration and approval of the Resolution Plan, further appeal, termination of PPIRP etc.

- Further, the IBBI has notified the IBBI (Pre-Packaged Insolvency Resolution Process) Regulations, 2021.

Pre-requisites before initiation of PPIRP [Section 54A (2)]

- The Corporate Debtor should not have undergone PPIRP in the last or completed CIRP in the last three years

- The Corporate Debtor shouldn't be already undergoing CIRP or no liquidation order has been passed under Section 33 against the Corporate Debtor

- The Corporate Debtor should be eligible under Section 29A of IBC to submit a Resolution Plan

- 66% of the unrelated financial creditors should approve the appointment of the Resolution Professional and the proposal

- Partners or Directors of Corporate Debtor shall make declaration in terms of Section 54A(2)(f).

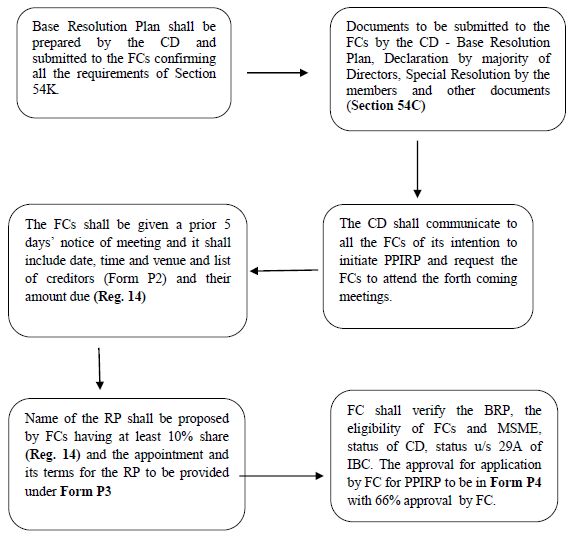

FLOW CHART EXPLAINING THE PROCESS TO BE FOLLOWED BY THE CORPORATE DEBTOR BEFORE THE INITIATION OF PPIRP

Before making an application for initiation of PPIRP to the Adjudicating Authority, the Corporate Debtor/Applicant through the Resolution professional shall serve a copy of application to the IBBI including the list of Financial Creditors, list of Operational Creditors, Approval of FCs for appointment of Resolution Professional as per Form P3 and written consent of RP as per Form P1, Declaration of majority of Directors in Form P6, Copy of Special Resolution of members etc.6

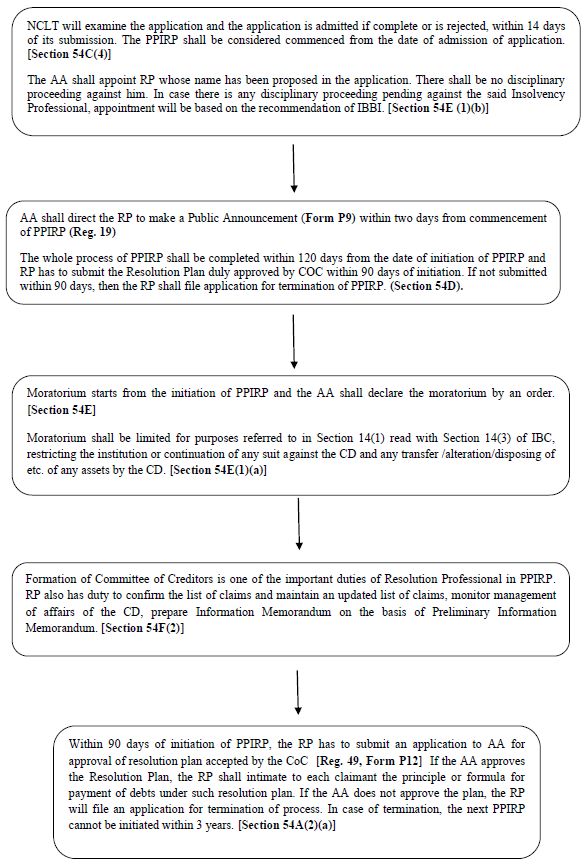

FLOWCHART EXPLAINING THE PROCESS FOR ADMISSION OF APPLICATION BY ADJUDICATING AUTHORITY (NCLT) FOR COMMENCEMENT OF PPIRP

Benefits of PPIRP

- PPIRP takes less time than CIRP

- Cost effective: As less time is taken and many steps taken towards resolution before going to the Adjudicating Authority, money spent is also less comparatively.

- Management of the Corporate debtor remains in the hands of the Board of Directors of the Corporate Debtor. Therefore, the operation of CD is run smoothly.

- There is less judicial interference in the PPIRP.

PPIRP should be treated as a welcome step and a value addition to the Insolvency and Bankruptcy laws of India. With MSMEs being the most affected sector due to the pandemic condition, PPIRP intends to solve various difficulties of the MSMEs and we hope to attain positive results from it. For PPIRP to become successful, the approach of MSMEs in accepting it as a way to resolve insolvency is most crucial.

Footnotes

1. Section 54A (1) of the Insolvency and Bankruptcy Code.

2. Section 54D (1) of the Insolvency and Bankruptcy Code.

3. Section 54A (4) (c) of the Insolvency and Bankruptcy Code

4. Section 54D (2) of the Insolvency and Bankruptcy Code

5. Section 54H of the Insolvency and Bankruptcy Code

6. Section 54B(1)(b) of The Insolvency and Bankruptcy Code.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.