- within Tax, Privacy, Litigation and Mediation & Arbitration topic(s)

- with Inhouse Counsel

- in India

- with readers working within the Accounting & Consultancy, Banking & Credit and Law Firm industries

|

Note on statutory references: The Income Tax Act, 1961 has been replaced by the Income Tax Act, 2025 (in force 1 April 2026), and the Income Tax Rules, 1962 have been succeeded by the Income Tax Rules, 2026. The substantive provisions and rules referenced in this article — including Sections 90, 96, 144C, 144BA, 197, 245R and 245W, and Rules 10D, 10U and 44G — are carried forward in materially identical terms in the new legislation and rules. For clarity and ease of cross-reference, citations throughout this article are to the 1961 Act and 1962 Rules. The analysis applies without modification to the corresponding provisions of the 2025 Act and 2026 Rules.

|

Executive Summary

Tiger Global has reset the standard for treaty entitlement in India. For international practitioners and in-house counsel advising on India-facing structures — whether cross-border holding arrangements, MNC intercompany flows, EPC projects, or PE fund structures — the judgment's holdings on substance, JAAR, and TRC sufficiency are immediately relevant regardless of where the client is based.

The Tiger Global decision alarmed international practitioners. The dual amendments of 31 March 2026 have answered one part of that alarm. Grandfathering for pre-April 2017 investments is restored, and a clarificatory retrospectivity argument gives taxpayers in pending proceedings a legitimate basis to contend that Tiger Global's grandfathering holding should not govern their cases. But the judgment's holdings on substance, JAAR, TRC sufficiency, and arrangement-level analysis from inception remain fully operative. For practitioners advising on India-facing structures, the amendment fixes the headline, not the substance. This article maps what remains dangerous, identifies the open questions Tiger Global left unsettled, including the Section 90(2A) argument the Court never addressed and the PPT/LOB sequencing question that is live for every treaty with a comprehensive anti-abuse framework, and sets out what practitioners must do at each intervention point across the lifecycle of a cross-border structure. For taxpayers under treaties with full PPT or LOB clauses who can genuinely satisfy those tests, the article's central finding is that Tiger Global changes little substantively, but the documentation and sequencing strategy to protect that position must be built now.

Section 1 — What Tiger Global Did and Why It Alarmed Everyone

It began with a $16 billion deal. In 2018, Walmart acquired Flipkart in one of India's largest technology transactions. Among the sellers were three Mauritius-incorporated entities of the Tiger Global group, holding shares in Flipkart Singapore since 2011, before India's GAAR came into force, with valid Tax Residency Certificates, in a structure unremarkable by the standards of its time.

On 15 January 2026, the Supreme Court dismantled it entirely.

In Authority for Advance Rulings v. Tiger Global International II Holdings (Civil Appeal Nos. 262–264 of 2026), Justices R. Mahadevan and J.B. Pardiwala held that the Mauritius entities were not entitled to treaty protection.

Any multinational with a treaty-based India structure, any PE or VC fund with pre-2017 India investments held through Mauritius or Singapore, and any EPC contractor with an offshore supply component routed through a treaty jurisdiction is affected by what the Court held, and equally by what it left open.

While the alarm that followed is justified in part, the judgment's reach is frequently overstated.

A. What the Court held — five propositions

First, on TRC sufficiency: Sections 90(4) and 90(5) read together require more than a certificate of residence. Circular 789's conclusive treatment does not survive the subsequent statutory amendments.

Second, on Section 90(2A): The Court confirmed definitively that notwithstanding Section 90(2)'s beneficial treatment rule, Chapter X-A applies even if not beneficial. Critically, what the Court did not address (for it was neither raised nor argued by either party) is whether Section 90(2A) is triggered at all where an assessee claims treaty entitlement without invoking Section 90(2), standing instead directly on the treaty as notified under Section 90(1). It is the author's view that Tiger Global's silence on this distinct question may, to that limited extent, be characterised as sub silentio, with the consequence that the specific issue remains open for adjudication, consistent with the Supreme Court's own jurisprudence in Municipal Corporation of Delhi v. Gurnam Kaur (1989) 1 SCC 101. This is not an argument that Tiger Global was wrongly decided. It is the narrower proposition that a question not raised and not addressed has not been settled, and remains available to be tested directly.

Third, on grandfathering: Rule 10U(2) was held to override Rule 10U(1)(d). This holding has since been addressed by legislative correction, discussed in Section 2.

Fourth, on JAAR: The Court confirmed that Judicial Anti-Avoidance Rules (uncodified principles of substance-over-form) operate independently of statutory GAAR and without the Section 144BA Approving Panel process. However, the practical implications of this proposition are frequently overstated. In the AAR context, where no Chapter X-A machinery applies, the Court sustained JAAR as the appropriate tool for the Section 245R(2) threshold analysis. In a regular assessment proceeding, the position is more nuanced: where Revenue never invoked GAAR through Section 144BA, JAAR cannot fill that gap on Revenue's appeal; appellate courts cannot make Revenue's case for it. However, where it is the assessee who appeals, a court may dismiss on JAAR grounds independently of the basis on which the lower forum decided, upholding the result without being bound by the reasoning below.

Fifth, on double non-taxation: The Court treated it as one contextual factor in a holistic analysis, not as a standalone rule. Its tension with Azadi Bachao's position that even exempt entities are liable to tax for treaty purposes remains unresolved.

B. What the Court did not hold — and what to expect next

Tiger Global did not address treaties with detailed PPT or LOB clauses. The India–Mauritius treaty at the relevant time had neither. The 2016 Protocol inserted only a narrow Article 27A LOB applicable to the transitional capital gains window between 1 April 2017 and 31 March 2019, not a treaty-wide anti-abuse provision. The judgment accordingly left the sequencing question entirely open: whether, in treaties with comprehensive negotiated PPT or LOB clauses, treaty entitlement must first be tested through those provisions alone, with GAAR invocable only if the taxpayer fails that treaty's own anti-abuse test; or whether GAAR can bypass a treaty's anti-abuse framework entirely, regardless of how comprehensive that framework is. That question is live and undecided for India's treaties that do carry robust PPT or LOB provisions, including the India–US DTAA, and is distinct from anything Tiger Global settled.

Nor did the Court hold that JAAR applies universally across all proceedings, as the analysis of Proposition 4 above makes clear.

The author had anticipated, prior to the judgment, that the government would issue a correction, one that as subsequently materialised sits in tension with its own litigation stance before the Supreme Court. In the author's view, a clarificatory circular or notification addressing the interaction between GAAR and treaties containing full PPT or LOB clauses, parallel to the grandfathering correction, is now likely and necessary. Until it arrives, the sequencing argument retains significant value.

The tools to deploy that argument, and every other available defence across the lifecycle of a cross-border structure, are the subject of what follows.

For a detailed analysis of the pre-Tiger Global framework, both sides' arguments, the judgment's doctrinal shifts, and strategic considerations including the sequencing question and MAP, and notably for an anticipation of the legislative correction that followed, see the author's earlier article: "Tiger Global Ruling: Does GAAR Override Tax Treaties and What Is the Way Forward?" published on Mondaq on 5 February 2026.

Section 2 — The Government's Correction — And Its Limits

Within six weeks of the judgment, the government acted. On 31 March 2026, CBDT issued two notifications simultaneously: (i) Notification No. 54/2026 amending Rule 10U of the Income Tax Rules 1962, effective that day, and (ii) Notification No. 55/2026 amending Rule 128 of the Income Tax Rules 2026, effective 1 April 2026. Both make the same substantive correction, in structural tension with the government's own litigation stance before the Supreme Court. GAAR applies to arrangements yielding tax benefits on or after 1 April 2017, except for income from transfer of investments made before that date. The amendments structurally foreclose the Tiger Global reading going forward.

The amendments are prospective on their face and taxpayers caught in the window between 2017 and 31 March 2026 obtain no direct relief. There is, however, a reasonable basis to argue that the amendments are clarificatory rather than substantive, correcting a drafting defect to restore what Parliament always intended. Clarificatory amendments operate retrospectively as a matter of settled principle, declaring what the law always was rather than changing it. On that basis, taxpayers with pending proceedings can legitimately contend that Tiger Global's grandfathering holding should not govern their cases.

Section 3 — The Remaining Sting

The dual amendments restored grandfathering. Everything else Tiger Global decided remains fully operative. For most cross-border structures, it is the everything else that matters.

The most immediate concern arises from the Court's confirmation that JAAR may operate without the procedural safeguards associated with statutory GAAR. That proposition, however, is not unbounded. In a regular assessment proceeding, Revenue must invoke GAAR through Section 144BA; JAAR does not operate as a substitute. The exposure instead arises at the AAR threshold and at the appellate stage, where a court dismissing an assessee's appeal may sustain the outcome on JAAR grounds independently of the reasoning below. It would therefore be an overstatement to suggest that every cross-border payment is now subject to substance scrutiny without procedural constraint, but the exposure in specific forums and appellate contexts is both real and material.

The second remaining problem is the permanent reduction of TRC from conclusive to merely necessary. The evidentiary burden on a foreign entity claiming treaty benefits has materially risen. Documentation that was sufficient before Tiger Global is no longer sufficient after it. What sufficiency now requires is a question without a clear answer; which is itself part of the problem.

The third is the shift to arrangement-level analysis from inception. Tiger Global moved the enquiry from the transaction (Vodafone's approach) to the entire arrangement from the moment of structuring. Structures that appeared unassailable at entry may be examined at exit through a retrospective lens that did not exist when they were built.

On the fourth point, the tension between Tiger Global's taxability-in-residence-state observation and Azadi Bachao's settled position on liable-to-tax: the Court treated this as one contextual factor in a holistic analysis, not a freestanding rule. Its recency, combined with the three problems above, adds to an already complex documentation and substance burden. Taken together, they make the case for seeking certainty through structured routes. Those routes are the subject of what follows.

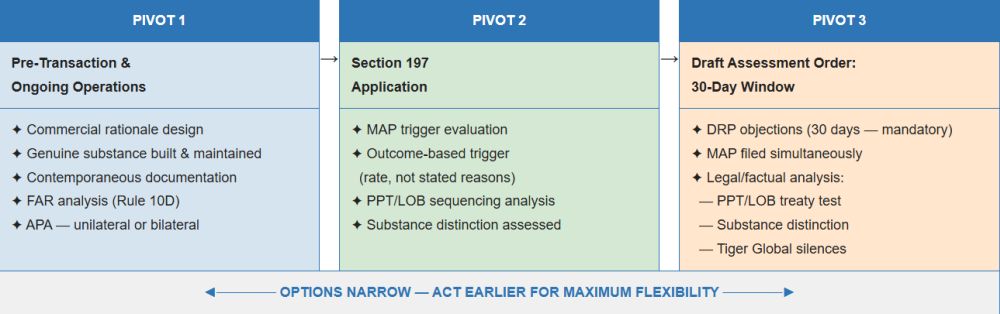

Section 4 — Lifecycle Management of Tiger Global Risk: Three Pivots, Three Tools

Tiger Global risk does not begin when a notice arrives. It accumulates across the lifecycle of a cross-border structure, from the commercial decisions made at inception, through the ongoing substance of the entity's operations, to the moment Revenue first asserts a position. Three intervention points exist, each representing a narrowing window of available options. The earlier the action, the wider the choices. By the time the last pivot, the draft assessment order, arrives, the AO has formed his view and the taxpayer is defending a position rather than building one.

Pivot 1 covers what must be done before any Revenue authority is involved, both at the moment of structuring and in the ongoing life of the entity. Pivots 2 and 3 address the two moments at which Revenue first formally enters the picture and the response options that remain available at each.

DIAGRAM 1 — Lifecycle of Tiger Global Risk: Three Pivots

A. Pivot 1 — Pre-Transaction and During the Life Cycle of the Structure

The documentation and substance framework that follows applies regardless of treaty type, though its primary legal function differs. In treaties with full PPT or LOB clauses, it serves first as the evidentiary foundation for satisfying the treaty's own anti-abuse test, supporting the sequencing argument that GAAR should not apply independently where that test is met. If the sequencing argument fails, the same material addresses the GAAR standard under Section 96(1). In treaties without such clauses, it goes directly to that GAAR standard. The file built correctly under Pivot 1 addresses both simultaneously.

Tiger Global's arrangement-level analysis from inception makes the entire lifecycle relevant, from the moment of structuring through to exit. The appropriate response is not documentation alone. It is genuine commercial design, genuine substance, and a contemporaneous record of both.

At the structuring stage, the commercial rationale for the structure must be genuine and primary. Section 96(1) defines an impermissible avoidance arrangement by reference to whether the main purpose or one of the main purposes is to obtain a tax benefit. Tax efficiency as one consequence does not make a structure impermissible. Vulnerability arises where tax benefit is the sole or dominant purpose with no independent commercial rationale. That rationale (regulatory pooling, ring-fencing, regional management, investor diversification) should be recorded in founding documents and legal opinions created at the time of structuring, not reconstructed after a notice arrives.

After structuring, substance must be built and maintained as an operational reality. Substance is a question of fact determined holistically. There is no fixed checklist. Factors that have been relevant in decided cases include employees performing real functions in the treaty jurisdiction, board meetings actually held there, and decision-making genuinely independent of a third-country parent. These are illustrative, not exhaustive. What matters is that the entity's commercial reality matches its legal form, and that contemporaneous documentation (board minutes, employment records, service delivery evidence) exists to prove it without inferential reconstruction.

For MNCs with management fee, royalty, or financing flows, transfer pricing FAR documentation and an APA serve a specific additional purpose. A thorough FAR analysis creates a contemporaneous record of functional reality that makes Revenue's subsequent recharacterisation of the same arrangement as lacking substance internally contradictory. An APA, whether unilateral or bilateral, is binding on all Indian Revenue authorities and creates a documented record of their prior acceptance of the arrangement's functional reality. A bilateral APA additionally strengthens the MAP position if a bilateral dispute subsequently arises.

B. Pivot 2 — Section 197 Application: The Most Overlooked Trigger

Tiger Global did not begin with a draft assessment order. Before the Flipkart transaction was consummated, the Mauritius entities applied under Section 197 of the Income Tax Act 1961 for nil withholding certificates.

Where the AO denies a nil certificate or issues a certificate at a rate inconsistent with treaty entitlement, whether expressly on the ground of substance concerns, TRC insufficiency, or control exercised from a third country, or by implication from the rate applied, that outcome is a Revenue action that results or will result in taxation not in accordance with the applicable DTAA. Rule 44G(1) of the Income Tax Rules 1962, substituted w.e.f. 6 May 2020 by Notification G.S.R. 282(E), provides that a taxpayer may make a MAP application where such an action results or will result in taxation not in accordance with the relevant DTAA. The practitioner should not wait for the AO to articulate express grounds. Where the rate applied is inconsistent with treaty entitlement, regardless of whether reasons are given, MAP evaluation should begin immediately.

Initiating MAP at the Section 197 denial stage is the earliest and most open bilateral engagement available. At this stage, Revenue's position has been asserted but not yet elaborated through a full assessment. The competent authorities of both states can engage on the treaty interpretation question, including whether the applicable treaty's own anti-abuse framework, such as a PPT or LOB clause, has been properly applied and, where satisfied, whether GAAR can be independently invoked, before a domestic assessment formalises and entrenches Revenue's view. The problem at this stage is easier to address than after a detailed assessment order has been issued.

One important qualification must be stated clearly. MAP initiated at the Section 197 stage is not mechanically available in all cases or on all arguments. MAP has its greatest practical value where the case is genuinely distinguishable: a treaty with PPT or LOB whose GAAR interaction Tiger Global never addressed, genuine substance that differs from the absent-substance patterns Tiger Global targeted, or double taxation requiring correlative relief. Identifying those distinctions precisely is the first task.

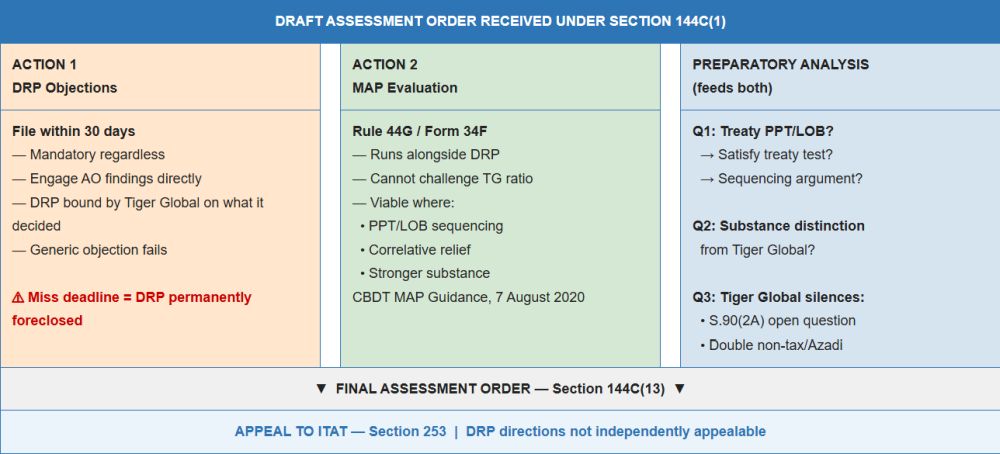

C. Pivot 3 — Draft Assessment Order Under Section 144C(1): The Last Window

For a foreign company (an eligible assessee under Section 144C(b)(ii)), the AO cannot pass a final assessment order directly. Section 144C(1) mandates a draft order first. The assessee has 30 days under Section 144C(2) to file objections before the Dispute Resolution Panel. If none are filed, the AO passes the final order on the draft itself, and DRP is permanently foreclosed. If filed, the DRP issues binding directions within nine months under Section 144C(5) and the AO passes the final order within one month under Section 144C(13). Appeal to ITAT lies against the final order. DRP directions are not independently appealable.

DIAGRAM 2 — The 30-Day Window: Two Parallel Actions

Two things must happen in parallel within that window.

DRP objections must be filed within 30 days regardless. The objection must directly engage the AO's specific factual findings, not merely assert error. The DRP is bound by Tiger Global on what it decided. A generic objection will not succeed. A precisely targeted objection on Tiger Global's silences and on treaty-specific arguments, however, is not foreclosed.

MAP must be evaluated simultaneously. If not initiated at the Section 197 stage, the draft order is itself the MAP trigger under Rule 44G. MAP and DRP proceed simultaneously; filing one does not require withdrawing the other. The CBDT MAP Guidance of 7 August 2020 confirms this coexistence. MAP cannot challenge Tiger Global's ratio and is valuable only where genuine distinctions exist: the PPT/LOB sequencing argument, correlative relief, or materially stronger substance.

A practitioner might ask why advance rulings are absent. The Board for Advance Rulings, which replaced the AAR from 1 September 2021, comprises two Chief Commissioners with no judicial member and issues non-binding rulings appealable by both sides to the High Court under Section 245W. More fundamentally, BAR will apply Tiger Global as binding law on substance, JAAR, and TRC sufficiency. APA, FAR documentation, and MAP are the practical substitutes for the certainty advance rulings once provided.

Structured legal and factual analysis feeding both the DRP objection and MAP application will be required. In this analysis, three questions must be answered with precision. For taxpayers under treaties without PPT or LOB clauses, all three questions carry equal weight. For taxpayers under treaties with comprehensive PPT or LOB clauses who can genuinely satisfy those tests, Question 1 (the sequencing argument) is the primary ground; Questions 2 and 3 are supporting arguments deployed if the sequencing argument fails or is not accepted at the DRP stage.

First: does the treaty contain a PPT or LOB clause and does the taxpayer genuinely satisfy it? Tiger Global did not address this because the India–Mauritius treaty at the relevant time had no PPT and no general LOB clause. That silence is the space available in treaties that do have comprehensive anti-abuse provisions, but only for a taxpayer who can genuinely pass the treaty's own test. The sequencing argument has principled legal grounding independent of Tiger Global's silence. Although India has not ratified the Vienna Convention on the Law of Treaties 1969, in Ram Jethmalani v. Union of India (2011) 8 SCC 1 the Supreme Court recognised Articles 31–33 as reflecting customary international law applicable in the Indian treaty interpretation context. Where a treaty contains its own PPT or LOB, that provision is the agreed bilateral anti-abuse standard. A domestic rule that bypasses it without engagement sits uneasily with that obligation.

Second: is the substance profile materially distinguishable from Tiger Global? The enquiry is holistic, not a checklist. Tiger Global involved absent substance: no employees, no operational expenditure, third-country control. A taxpayer with genuine employees, independent board governance, and documented commercial reality starts from a materially stronger position. Where substance is genuine, the DRP objection argues Tiger Global established no general rule against intermediary structures. It addressed the specific pathology of wholly absent substance. Where substance is absent or nominal, the MAP and sequencing arguments become proportionally more important.

Third: what did Tiger Global not decide beyond the treaty and substance questions? Two silences remain relevant. The Section 90(2A) open question, namely whether it reaches an assessee standing on the treaty under Section 90(1) without invoking Section 90(2) at all, was not raised, not argued, and not decided, and may have the character of a sub-silentio decision per Municipal Corporation of Delhi v. Gurnam Kaur (1989) 1 SCC 101. This should be identified precisely in the DRP objection as a question the Supreme Court left open. The tension between Tiger Global's taxability-in-residence-state observation and Azadi Bachao's settled position on liable-to-tax also remains unresolved. It is better held in reserve than pressed as a primary ground at this stage, given that the Court treated it as one contextual factor rather than a freestanding rule.

Conclusion

The amendment closed the grandfathering controversy, and does so retrospectively for pending proceedings on the clarificatory amendment argument. Everything else remains open. For taxpayers under treaties with comprehensive PPT or LOB clauses who can genuinely satisfy those tests, Tiger Global changes little substantively. The sequencing argument is the primary defence, and the documentation built under Pivot 1 serves double duty: satisfying the treaty's own anti-abuse test first, addressing GAAR under Section 96(1) if the sequencing argument fails. For treaties without such clauses, that same documentation goes directly to GAAR. The practitioner's immediate priorities are universal regardless of treaty type: audit existing structures for contemporaneous commercial rationale documentation and FAR analysis now; at any Section 197 denial, evaluate MAP immediately without waiting for reasons to be stated; at the draft assessment order, file DRP objections within 30 days without exception and evaluate MAP simultaneously, building the objection on Tiger Global's silences and treaty-specific arguments rather than generic error assertions. The Section 90(2A) open question and the PPT/LOB sequencing argument are live and belong in every DRP objection and MAP application where the facts support them.

The consequence is not that treaty protection has disappeared, but that it must now be actively demonstrated rather than presumed.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]