India's journey to Viksit Bharat needs a fiscal rethink to drive sustainable growth.

In brief

- Aim for a zero-revenue deficit for both the GoI and states, implying elimination of government dissavings and boost the nominal saving rate to 33.5% of GDP.

- Combine a 33.5% nominal savings rate with 2% net foreign capital inflows to achieve total investible resources in nominal terms at 35.5% translating into real terms at 38.5% of GDP.

- Achieve a 7% real GDP growth with real investible resources at 38.5% of GDP combined with an incremental capital-output ratio (ICOR) of 5.5.

As India progresses towards a Viksit (developed economy) status, there is a need to recast the current fiscal responsibility framework (FRF), which evolved over a period from 2002 to 2010. The major milestones in the evolution of this framework occurred with the enactment of the Fiscal Responsibility and Budget Management Act (FRBMA) by Government of India (GoI) in 2003 and the submission of the report of the 12th Finance Commission (FC12) in 2004, after which most states enacted their Fiscal Responsibility Legislations (FRLs). In 2018, the FRBMA underwent revisions, setting a target for the general government (GG) debt at 60% of GDP, and that for the GoI at 40% and by implication that for state governments at 20%.

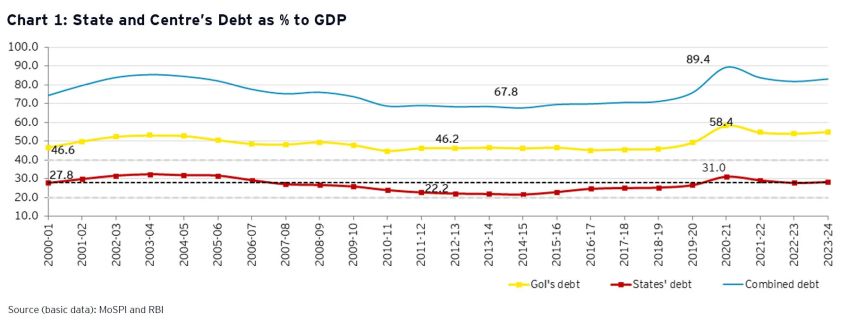

Government debt profiles

General government debt-to-GDP ratio, which had fallen to a trough of 67.8% in FY2015, rose to 89.4% in the COVID year of FY2021. In that year, the GoI's debt-GDP ratio had increased to 58.4% while the state debt-GDP ratio had increased to 31% (Chart 1). These levels are well above the debt-GDP targets set by the FC12 as well as the GoI's FRBMA (2018). It is also notable that while the deterioration in the level of debt took just one to two years, the downward adjustment is taking a much longer time. Even as the debt-GDP ratio is brought down by the GoI and the state governments, there is also a need to reconsider the FRF.

Why the GoI should consider revising the FRBM Act

The 2018 FRBMA amendment is characterized by a number of issues. This amendment envisaged a 40:20 split of the total government debt-to-GDP ratio between the central and state governments, while implicitly giving both a symmetrical fiscal deficit of 3% of GDP. This is an inconsistent combination as long as the underlying nominal GDP growth is the same for the GoI and the aggregate of states1. Further, this amendment gave up the target for achieving revenue account balance which was the primary feature of the 2003 FRBMA.

As the Indian economy progresses, it is important to recast its fiscal responsibility targets in the respective legislations of GoI and the state governments with the following features: (a) the target for keeping revenue account in balance or surplus should be brought back, (b) targets for fiscal deficit and debt relative to GDP should be symmetric between GoI and states at 30% and 3% respectively assuming an underlying nominal GDP growth of 11%. Further, the GoI may be provided with a flexibility up to +/- 2% points of GDP in the fiscal deficit target for macro stabilization (i.e. a range of 1% to 5% of GDP). During slowdown years it may be increased up to 5% of GDP. However, in subsequent years, when the economy has normalized it should be brought down suitably so as to keep an average fiscal deficit level of 3% of GDP. In case the crisis is much bigger, such as the Covid crisis, suitable variation in GoI's and states' fiscal deficit beyond the above range may be considered by an appropriate body such as a fiscal council which may be constituted either only to deal with that crisis or on a more permanent basis.

Linking revenue deficits to government dissavings and potential growth

Simply put, government dissavings, or revenue deficit is excess of government's revenue/operational expenditures over its revenues receipts from tax and non-tax sources. The recasting of FRF has to be placed in the broader perspective of India's potential GDP growth. It is the availability of domestic savings supplemented by net inflow of foreign capital that provides the investible resources which combined with ICOR determines India's potential growth.

As the first step, the fiscal deficit to GDP ratio is derived from the saving-investment profile of the economy. In particular, the supply of surplus savings emanates from the household (HH) sector in the form of household financial (HHF) savings which is then absorbed by three deficit sectors where investment demand is in excess of their own savings namely government sector (GG), non-government public sector (NGP), that is excluding administrative departments, and private corporate sector (PC). The net supply of investible resources is the sum of HHF savings and net inflow of foreign capital. Fiscal deficit constitutes the first claim on this supply of investible resources. Once fiscal deficit is specified, the balance becomes available for the remaining sectors.

Chart 2 shows that in a multi-country context, considering average per capita GDP during 2017-19, India's saving rate should have been 20.1% of GDP if India were to be placed on the trend line. However, India's actual nominal saving rate2 was 29.5% implying that India enjoys a demographic dividend3-cum-cultural premium of 9.4% points.

This is what explains India's ability to reach and sustain the position of a global growth leader at present. Assuming that this premium is maintained even as India reaches a higher per capita GDP level of US$14,0054 (natural log of this is 9.5), consistent with a developed country status, India should have a nominal saving rate of 33.5% at the time of becoming Viksit.

In order to convert the nominal saving rate (as a % of GDP) of 33.5% into real investment rate, two steps are involved:

- First, augmenting nominal saving rate by the addition of net-inflow of capital from abroad estimated at 2% of GDP, which gives a nominal investment rate of 35.5%.

- Second, to derive the real investment rate, a premium of approximately 3% of GDP arising on account of differential deflators for investment goods vis-à-vis consumption goods needs to be added leading to a potential real investment rate of 38.5% for Viksit Bharat.

If an incremental capital-output ratio (ICOR) of 5.5 is applied, it will yield a potential real GDP growth rate of 7%.

It is also useful to decompose the aggregate nominal saving rate of 33.5% into its sectoral composition and also link it to government's draft on available sectoral surplus savings.

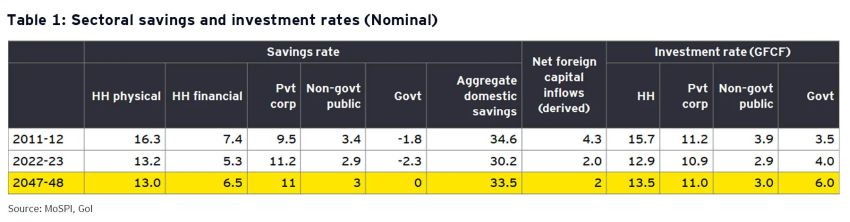

Table 1 shows the profile of sectoral saving-investment rates (as % of GDP) from FY2012 onwards. In FY2023, HHF savings at 5.3% of GDP have fallen tangibly below the historical average. This may, however, be temporary. By FY2048, a level of HHF saving rate of 6.5% may be enough. Any shortfall in this may have to be made up by government's reliance on external financing. Given the current saving profile of PC and NGP, an aggregate nominal saving rate of 33.5% requires government dissaving to be zero.

Going by the trend in sectoral investment profile in recent years5, the composition of overall nominal gross fixed capital formation (GFCF) of 33.5% of GDP (Table 2) in FY2048 will be made up by investments by HH6 at 13.5%, PC at 11.0%, NGP at 3% and GG at 6%. Its real counterpart may be estimated at 36.5%7. Adding to this change in stocks and valuables of 2% of GDP, real gross capital formation (GCF) may be estimated at 38.5%. Thus, for India to reach a Viksit status by FY2048, the only change that we envisage is eliminating government dissaving, linked to reducing revenue deficit target to zero and increasing GG investment rate to 6.0% of GDP in nominal terms.

Recasting debt and fiscal deficit targets

The above data shows why the overall fiscal responsibility framework of the GoI needs to be recast to facilitate India's progress towards a developed nation. GoI and states' revenue accounts need to be brought in balance or surplus which may also be facilitated by a progressively increasing tax-GDP ratio from its present level. Further, the debt and fiscal deficit targets for the GoI and the aggregate of states should be made symmetric. Correspondingly, the aggregate debt and fiscal deficit of 60% and 6% should be divided equally between the GoI and the states at 30% and 3% each. These targets are drawn up with an underlying nominal GDP growth of 11% which may be broken up into a real GDP growth of 7% and an IPD-based inflation of close to 3.5%.

Footnotes

1. Srivastava, D.K., Bharadwaj, M., Kapur, T., & Trehan, R. (2021).Covid's Economic Impact: Should India Recast its Fiscal and Monetary Policy Frameworks?: Journal of International Economics and Finance. 1(1), 63-81

2. Gross National Savings rate

3. Srivastava, D.K., Bharadwaj, M., Kapur, T., Trehan, R. (2023). India's Economy in the Twenty-First Century: Role of State-Differentiated Demographic Dividend. In: Srivastava, D.K., Shanmugam, K.R. (eds) India's Contemporary Macroeconomic Themes. India Studies in Business and Economics. Springer, Singapore. https://doi.org/10.1007/978-981-99-5728-6_3

4. For details, refer to in-focus section of EY Economy Watch December 2024 edition.

5. In recent years, PC sector saving rate at 10% plus exceeded its investment rate. Given this trend, its investment rate may be increased to about 11%. For NGP, saving and investment rates also broadly match. If these relativities continue, then GG fiscal deficit would be almost entirely financed by HHF savings.

6. HH investment include investments in physical and financial assets

7. For details, see infocus section of EY Economy Watch, December 2024 edition

Originally published 23 Dec 2024

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.