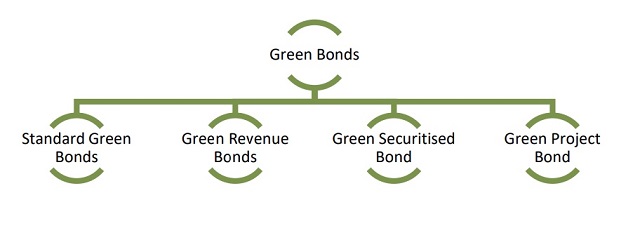

WHAT ARE GREEN BONDS?

A Green Bond is a fixed-income debt instrument, like a regular bond, which is specifically earmarked for financing 'green' projects such as renewable energy projects, clean transportation projects, water management projects etc. It encourages sustainability and has numerous goals - from climate change mitigation to energy efficiency, the prevention of pollution, etc.1 As per the Green Bonds Principles (Voluntary Guidelines for Issuing Green Bonds) (GBP) issued by the International Capital Markets Association, Green Bonds include the following bonds:

GBP recognises "green projects" to include any project in relation to (i) renewable energy; (ii) energy efficiency; (iii) pollution control; (iv) green buildings and real estate; (v) refurbished goods; and (vi) sustainable water management systems. Any entity issuing a Green Bond is also strongly encouraged to (i) provide clear indications to prospective investors of the sustainability objectives and environmental perils associated with the instrument; and (ii) maintain transparent and accurate records of fund allocation and fund usage, to facilitate impact assessment and end-uses of green bond proceeds. Additionally, the investors shall also be informed of the allocated and unallocated net proceeds during the stages of fund disbursement and usage.

GREEN BONDS AND THE INDIAN MARKET

The Green Bond market in India has achieved various milestones since 2015, when Yes Bank issued India's first ever Green Bond.

A large number of corporations in the renewable energy sector have cashed on this opportunity to raise capital and attract foreign investment.

In August 2016, the National Thermal Power Corporation (NTPC) became the first Indian corporate entity to list the first green masala bond on London Stock Exchange2 .

In 2018, the State Bank of India raised USD 650 million by way of Green Bonds to fund sustainable and eco - friendly projects.

In the first half of 2019, India became the second largest Green Bond market after the People's Republic of China, having executed green bond transactions worth USD 10.3 billion.

In order to encourage and multiply environmentally sustainable investments, became a part of the International Platform on Sustainable Finance (IPSF) in 2019. The IPSF aims at scaling up the mobilisation of private capital toward environmentally sustainable projects3 .

India is amongst the first few countries in the world to have laid down a statutory framework to regulate Green Bonds.

REGULATORY FRAMEWORK

Indian regulators have played an active role in this regard and have been successful in foreseeing the growth and impact of Green Bonds in the Indian market.

In 2017, SEBI issued the Disclosure Requirements for Issuance and Listing of Green Debt Securities (Disclosure Requirements)4 , in which green debt securities have been specifically defined. SEBI, via the Disclosure Requirements, calls on the issuer of the green bond (a debt security instrument) to make certain disclosures, including –

- a statement on the environmental objectives of the issuance;

- details of the procedures to be employed for tracking the deployment of the proceeds of the issue; and

- details of the project and/or assets for which the issuer proposes to utilise the proceeds of these green debt securities.

The Reserve Bank of India (RBI), on April 23, 2021 joined the Central Banks and Supervisors Network for Greening the Financial System (NGFS) as a member, to benefit from the membership of NGFS by learning from and contributing to global efforts on Green Finance.

In addition to the above, the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 define a "green debt security".

A green debt security is "any debt security issued for raising funds that are to be utilised for project(s) and/or asset(s) falling under any of the following categories:

- Renewable energy (including wind, solar, bioenergy, and any other energy sources using clean technology);

- Clean transportation;

- Sustainable water management systems;

- Energy efficient and green buildings;

- Sustainable waste management;

- Biodiversity conservation; and

- Any other category specified by the SEBI, from time to time".

Regulation 34 of the SEBI (Listing Obligations and Disclosure Requirements Regulations, 2015 mandates that the top 1000 entities (based on market capitalisation) must include in their annual report, business responsibility and sustainability report (BRSR) listing the ESG initiatives taken by the company.

Similar to the GBP, the legal framework for green debt securities has also been made available on the SEBI portal.

In addition to the regulatory changes, government has also created frameworks for sustainable corporate responsibility by way of environmental social and governance ("ESG") regulation.

It is pertinent to note, the corporate social responsibility framework under the (Indian) Companies Act, 2013 and extant rules, aligns regulation on eligible green CSR activities, annual reporting, and impact assessments – to support the adoption of best corporate governance practices.

The Green Bond market is essentially a subset of the corporate bond market and therefore, for Green Bonds to be recognised, the bond market needed to undergo further reforms as well.

RBI has increased the extent of partial credit enhancement to 50% of the bond issue size, with a limit up to 20% of the bond issue size for a particular bank5 . This move has led to provide additional comfort to the investors.

ADVANTAGES

Green Bonds have been rapidly emerging in the Indian market in recent years and have caught the eye of many investors for various reasons.

The proliferation of Green Bonds will help in financing eco-friendly projects and technology, as well as with attracting foreign investments due to the sudden growth in the energy sector globally. Green Bonds also have intangible value – they enhance the issuer's reputation and showcase their commitment towards sustainable development.

CHALLENGES

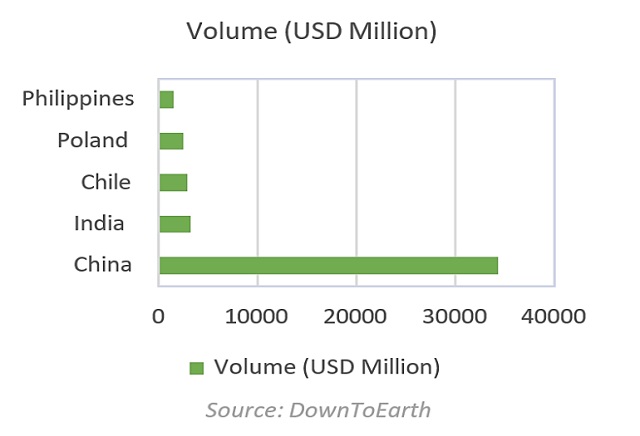

In accordance with a working paper published by the RBI titled 'Green Finance in India: Progress and Challenges' 6 , Green Bonds make up only 0.7 per cent of all the bonds issued in India. Even though India has the secondlargest Green Bond market, it lags far behind China (see above).

Importantly, Green Bonds have a relatively low interest rate viz. loans offered by commercial banks, this is a comparative disadvantage they will face, in being seen as a viable profitable avenue for investment. In general, larger investments imply faster access to debt for the companies and banks who are at the receiving end of this funding, resulting in higher yields.

Some of the challenges faced by Green Bonds in the Indian market are as follows -

Higher Costs:

The cost of issuing Green Bonds has remained higher than that of other bonds in India. This can be attributed to the lack of a national reporting and verification platform for tracking climate finance, the lack of coordination between investment and environmental policies and the insufficiency of policy and benefits framework at the national and state level7 .

Shorter tenure, uncertain returns:

Green Bonds in India have a shorter tenure of approximately 10 years while the tenure of a general loan is a minimum of 13 years. Furthermore, green projects often end up taking more time to showcase returns.

Lack of credit ratings for green bond market:

There is a lack of credit ratings for Green Bonds or Green Projects that ends up affecting the creditworthiness of such projects.

Greenwashing:

There have been several instances wherein the proceeds of Green Bonds have been used in projects that in reality have a negligible (or sometimes even negative!) impact on the environment. This is known as "green washing", and makes the whole point of issuing Green Bonds redundant.

THE PATH FORWARD

While the Indian government has been proactive in defining and regulating the Green Bond market in India, there are certain steps that need to be taken globally, in order to overcome the challenges that exist.

For instance, it is extremely important to align international and domestic guidelines and standards for Green Bonds, in order to establish a standardised market for these instruments.

It is also important to have a standard global definition of what is considered a 'green' investment' - for tax considerations as well as to avoid greenwashing.

Since Green Bonds are themselves a relatively new concept, it is imperative to spread knowledge on the advantages, as well as the procedures and ancillary information, in relation to Green Bonds. Creating awareness would help in addressing the institutional barriers to entry, into this market.

It is also interesting to see the (more recent) emergence of "Blue Bonds" in the global market, which are specifically issued to raise capital for financing the long-term sustainability of oceans, seas, and marine resources.

We believe that with the right regulations and screening processes in place, Green Bonds have the potential to play a major role in the development of both the Indian energy sector as well as its economy – and, as a bonus, help us move towards a sustainable tomorrow!

Footnotes

1 "Green Bonds And Greener Environment: Are They Linked?". Downtoearth.Org.In, 2021.

2 "NTPC Lists World's First Green Masala Bond By An Indian Issuer On London Stock Exchange". London Stock Exchange Group, 2021.

3 "International Platform On Sustainable Finance". European Commission - European Commission, 2021.

4 "SEBI | Disclosure Requirements For Issuance And Listing Of Green Debt Securities". Sebi.Gov.In, 2021.

5 "Reserve Bank Of India - Notifications". Rbi.Org.In, 2021

6 "Green Finance In India: Progress And Challenges*". Rbidocs.Rbi.Org.In, 2021.

7 Supra

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.