- within Real Estate and Construction topic(s)

Real Estate Investment Trusts, commonly known as REITs, are closed-ended retail funds that invest primarily in real estate and seek to provide returns to investors in the form of dividends. Investors purchase units of a REIT and earn rental income generated by the professionally managed real estate in the REIT portfolio without having to own the real estate.

REITs have gained wide popularity in major international capital markets such as Singapore and the United States; however, they have not done the same in Hong Kong, notwithstanding the fact that Hong Kong is one of the most expensive cities to rent a property and features one of the most robust stock exchanges by revenue. Currently, there are only 12 REITs listed on the Hong Kong Stock Exchange (HKEX), whereas there are more than 200 listed in the United States. In March 2021, the capitalization of REITs as a percentage of the total stock market was only 0.4% in Hong Kong, compared with over 12% in Singapore and more than 2% in the United States.

Clearly, there is a lot of untapped potential. Recent government initiatives, including a grant scheme for REIT listings and the 2020 amendments to the Code on Real Estate Investment Trusts (the Code), which introduced more flexible rules on investments in minority-owned properties, may encourage more REITs to list in Hong Kong.

The REIT Regime in Hong Kong

In Hong Kong, a REIT is mainly regulated by the Code, which is administered by the Securities and Futures Commission (SFC). In addition, as a REIT is considered a collective investment scheme (CIS), its listing on the HKEX is subject to Chapter 20 of the Listing Rules.

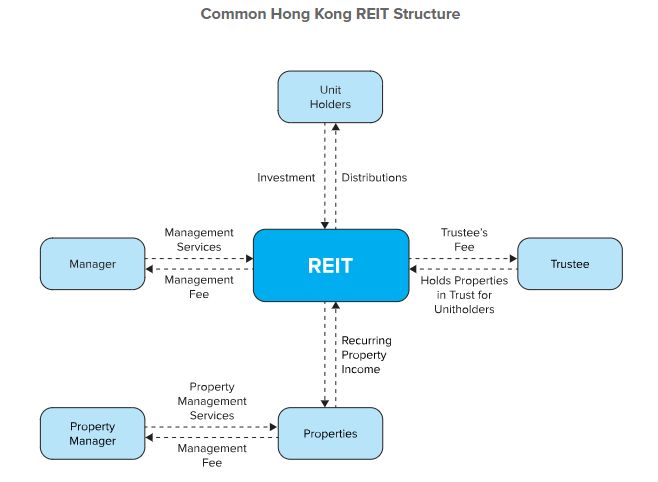

Basic Structure of a REIT

To apply for a REIT listing, a scheme must first obtain the SFC's authorization by satisfying the requirements in the Code. Some of these requirements are relevant to the basic structure of a REIT, including:

- The scheme must invest at least 75% of the gross asset value (GAV) in real estate that generates recurring rental income at all times, and is prohibited from investing in vacant land unless certain exceptional conditions are met.

- The scheme must distribute to unitholders as dividends 90% or more of its audited annual net income after tax.

- The scheme will be listed on the HKEX within a timeframe acceptable to the SFC.

- If the scheme is named after a particular type of real estate, at least 70% of its non-cash assets must be invested in such real estate.

- The scheme may hold real estate through a special purpose vehicle (SPV), subject to the preparation of an accountant's report on the profit and loss, assets, and liabilities of the SPV and a valuation report in respect of the SPV's interest in real estate.

Engagement of Operators

The scheme must engage operators that meet the qualification requirements of the Code. These operator requirements include:

- The scheme must appoint a trustee, which should be a licensed bank and have a minimum paid-up share capital and non-distributable capital reserves of HK$10 million, to hold the assets of the scheme in trust for the benefit of its unitholders.

- The scheme is managed professionally by REIT managers, or a REIT management company, who are licensed for Type 9 regulated activity by the SFC.

- The scheme must appoint a listing agent who is Type 6-licensed and is responsible for dealing with the SFC and the HKEX on all matters in relation to its listing application.

Government Initiatives to Encourage REITs in Hong Kong

Amendments to the Code

On 4 December 2020, the SFC announced some changes to the Code and accorded REITs with more flexibility in investing in properties and conducting asset enhancements. These changes include:

- REITs are now allowed to invest in minority-owned properties with different rules applying to qualified and non-qualified minority-owned properties. Previously, a REIT was required to hold more than 50% in each property it invested in.

- REITs are now allowed to invest in property development projects in excess of the previous limit of 10% GAV (subject to unitholders' approval and conditions).

- The borrowing limit for REITs increased from 45% to 50% of GAV.

Grant Scheme for REITs

On 24 February 2021, Hong Kong's Financial Secretary delivered his 2021-2022 Budget Speech, which featured the Grant Scheme for REITs, a three-year subsidy scheme that applies to SFC-authorized REITs listed on the HKEX with a minimum market capitalization of HK$1.5 billion at the time of listing. The grant amounts to up to 70% of the professional fees paid to local Hong Kong service providers, capped at HK$8 million, per REIT. This Grant Scheme, as an initiative to develop the REIT market and reinforce Hong Kong as a premier capital-raising center, may serve as an incentive for more REIT listings in Hong Kong.

Over the years, Hong Kong has taken steps to streamline and incentivize the listing of REITs, improving its competitiveness in the REIT market. The 2021-2022 Budget Speech once again highlighted the government's commitment to developing REITs in Hong Kong, which is an encouraging sign and will hopefully, in the years to come, lead to more activities in this untapped area of the Hong Kong capital markets.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.