- within Tax topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Accounting & Consultancy, Business & Consumer Services and Law Firm industries

A. INTRODUCTION

ICOs have recently exploded and become an increasingly popular method of fundraising for start - ups and other companies with the intention to fund innovative projects based on the Blockchain technology.

Our Firm being a business-oriented Firm has early identified the needs of the business world as to this innovative technology development based on Blockchain and in this respect has invested towards this direction with the establishment of an ICO team of professionals to cover all aspects of ICOs and assisting its international clients in this respect.

This is the second publication on the ICO subject. The first publication handling general issues of ICOs through Cyprus titled, "Initial Coin Offering (ICO) through Cyprus", can be downloaded from here.

Summary of this publication

With this publication, we shall try to give clarity to the unclear and highly unstable issue of the TAX and VAT treatment of ICOs from the issuer company's perspective. In particular, we shall deal with the issue of how the ICO proceeds received by a Cyprus issuing company may be treated, in terms of both direct taxation (Corporate Tax) and indirect taxation (VAT).

The review will be performed from the perspective of the Cyprus ICO issuing company. The tax treatment of the investors or token users would largely depend on the tax laws in their country of residence and it is outside the scope of this publication.

In the absence of specific guidelines by the Cyprus Tax Authorities on both TAX and VAT implications on ICOs, we will express our views based on the basic and fundamental provisions of the Cyprus Tax and VAT Legislations that are currently in force, while having in mind the general provisions of the International Financial Reporting Standards (IFRSs) that relate mainly to income recognition.

It must be stressed that the rights and powers represented by each token issue, are not uniform. As a result, there is no single answer as to how the issued tokens should be treated for tax purposes, hence, before concluding, careful consideration to the specific characteristics of each case is necessary.

VAT Rate

The currently applicable standard VAT rate for taxable supplies in Cyprus is 19%. As an ICO process involves a multinational approach with participants from all over the world, subject to the applicability of the offer, we shall mainly deal with the Vat aspect from Cyprus and in effect European Union (EU) perspective, where we consider the issued tokens will be mainly offered.

Income / Corporate Tax Rate

Cyprus can become one of the most beneficial EU jurisdictions for an ICO domiciliation due to its legal framework and flexible tax laws based on which business income of a Cyprus company is taxed at 12,5% on resulting net profits which tax rate may be further reduced subject to careful tax planning.

Intellectual Property (IP) Company

In addition, Cyprus has a very attractive IP Box Regime based on which 80% of Qualifying Profits generated from Qualifying IPs can be considered as deemed expenses and only 20% of the income is subject to 12,5% corporation tax, reducing thus the effective tax rate up to 2,5%.

As the most common result of an ICO is the development of intellectual property (IP), the benefits of the Cyprus IP Box Regime with the reduced taxation rate up to 2,5% might also be available to the ICO issuing companies making Cyprus one of the best destinations for an ICO having in mind also the rest of the surrounding circumstances.

For details of this Cyprus IP company treatment, you may refer to our Tax Update publication "The New Cyprus IP Box Regime" which can be downloaded from here.

The type of company to be used for the scope of our publication

The type of company for which we are considering the TAX and VAT treatment in an ICO prospect is the Cyprus Private Company Limited by Shares (LTD), being tax resident of Cyprus as we consider this type of company to be the most suitable vehicle for the intended operation of an ICO having a business nature and characteristics.

We have seen, mainly for tax reasons, foreign Foundations to be used as vehicles in ICO projects. Their charitable nature renders it questionable whether Foundations are indeed always a proper solution for all types of ICOs. It has also been suggested that Limited Liability Companies by Guarantee with or without share capital or even Purpose Trusts as another option.

For various reasons which are not the subject of discussion on this publication, we shall not examine those possibilities which might be the appropriate vehicles for particular type of ICOs having a philanthropic or charitable nature but not a business one.

On the contrary, a Cyprus non-tax resident Private Company Limited by Shares might be an option under the appropriate factual conditions but again we do not favor such approach, despite its tremendous Tax and VAT benefits from a Cyprus law perspective. The hidden risks involved in such approach makes us reluctant to suggest or consider such an approach.

B. TYPES OF TOKENS

The Tokens, subject to the particular issue, are in effect "contracts" granting certain rights to the investors or users. The issuing company decides the rights or claims it undertakes to grant to the investors or users through the tokens.

Subject to the characteristics of the issue, tokens may have different forms and classifications.

We consider that in their simple form, tokens may be any one of the following categories:

Pure Payment - Currency Tokens

These are tokens similar to cryptocurrencies, with an exclusively transactional purpose, which do not have any connection with any project or equity in the company. They are designed to be used solely as a means of payment. Such tokens do not have the characteristics of a security.

Pure Utility Tokens

These are tokens used to access products and services offered in the platform of the issuer. The issuing company has contractual obligation to exchange them with a service or product or allowing the use of the platform offering various services or products. They do not have any connection with the equity of the company. Such tokens do not have the characteristics of a security.

Pure Asset - Investment Tokens

These tokens are analogous to equities, debentures or derivatives. They are granting rights to dividends like equities / shares or to interest payments like bonds or to payments linked with the performance of a specific asset of the company like derivatives. Such tokens have the characteristics of a security.

The hybrid nature of a token

Despite the above classification of the tokens in the three main categories, the majority of the tokens issued are of hybrid nature which have at a certain degree, components of all the three classes identified above or any two of them. They are in effect, of Payment – Currency nature and/or Utility nature and/or Asset – Investment nature, all mixed together.

Ultimately, the tax treatment of such hybrid tokens will depend on whether they are classified as being within any of the above three main categories in the concept they will be used.

In effect, if a particular hybrid token is used at particular case as a Utility token then it might be treated as such and if in another occasion the same token will be used as a Payment - Currency token, then it might be treated as such, despite its hybrid character.

In this respect, our publication will mainly deal with the TAX and VAT treatment of the above three main categories of tokens leaving the hybrid nature of the tokens outside the below analysis.

Classification of tokens

The complex procedure of the classification of tokens in any one or a combination of the above categories in the context of an ICO, will not be the subject of this publication but to a forthcoming one in this respect.

Securities

For clarification purposes, the meaning of securities we adopt in this publication is the meaning of securities given under the Cyprus Prospectus law which it refers to transferable securities under the MiFID II definition as follows:

"transferable securities" means those classes of securities which are negotiable on the capital market, with the exception of instruments of payment, such as:

(a) shares in companies and other securities equivalent to shares in companies, partnerships or other entities, and depositary receipts in respect of shares;

(b) bonds or other forms of securitised debt, including depositary receipts in respect of such securities;

(c) any other securities giving the right to acquire or sell any such transferable securities or giving rise to a cash settlement determined by reference to transferable securities, currencies, interest rates or yields, commodities or other indices or measures;

Whether a particular type of token is a security or not, will not be the subject of this publication but of a forthcoming one in this respect.

C. ACCOUNTING TREATMENT AND THE CORRESPONDING TAX AND VAT IMPLICATIONS OF ICOs.

In order to be able to discuss the tax implications of ICOs for the issuing company, we first need to understand the classification of the relevant tokens based on their legal and economic characteristics on a case by case basis and then to refer to the accounting treatment of the relevant issuance in the books of the issuing company.

More specifically, we need to check whether the proceeds of an ICO can be recognized as Revenue in the Income Statement of the company according to IFRS 15 'Revenue from Contracts with Customers' and be taxed accordingly in the hands of the ICO issuing company.

Revenue recognition under IFRS 15 is based on the transfer of control. Control is defined as the ability to direct the use of and obtain substantially all of the remaining benefits associated with the asset.

Therefore, the key point for the correct accounting treatment of the ICO proceeds will depend on whether there is a transfer of control of an asset and if yes, to determine if the transfer of control happens over time.

Having considered the characteristics of the aforementioned categories of ICOs and the provisions of IFRS 15 mentioned above, we shall try to analyze the accounting and the corresponding tax treatment of each category.

I. Payment - Currency Tokens

By issuing tokens that qualify as a means of payment, (such as Bitcoins, Ether or Litecoin), the issuing company seems to have no other contractual obligation towards the token holder, other than the actual transfer of the tokens to the potential holders. As such, the sale of tokens triggers a taxable event and thus revenue should be recognised on the sale of payment - currency tokens.

The ICO proceeds (either in cryptocurrency or in any other fiat currency) will need to be translated to the reporting currency in which the issuing company presents its Financial Statements and taxed accordingly.

TAX treatment of Payment - Currency Tokens

ICO proceeds from the sale of tokens in the above category, seems to constitute taxable income in Cyprus for the issuing company, thus they are subject to 12,5% corporation tax on net profits.

The taxable amount can be reduced with careful tax planning. The related tax allowable expenses i.e. development of the relevant technology may be taken into account accordingly.

VAT treatment of Payment – Currency Tokens

The Court of Justice of the European Union (ECJ), in its Hedqvist decision, Case 264/14, explained that bitcoin (a cryptocurrency) represents a direct means of payment between the operators that accept it, therefore, the transaction concerning the exchange of bitcoin for fiat currency may fall within the scope of the exemption under Article 135(1)(e) of the EU VAT Directive 2006/112/EC, covering, inter alia, currency, bank notes and coins used as legal tender.

Consequently, one may argue that the exchange of payment tokens under an ICO for other cryptocurrencies or fiat currency could also qualify as an exempt transaction, within the scope of the exemption under Article 135(1)(e) of the EU VAT Directive 2006/112/EC and in this respect is exempt from VAT.

II. Utility tokens

Where the utility token simply defines a pre-paid right to consume an issuing company's goods or services, reference should be made to IFRS 15 'Revenue from Contracts with Customers'.

One may argue that, revenue cannot be recognized in full at the time of the ICO sale if the issuing company has additional contractual obligations towards the investor or user. It must be recognized over time as the performance obligation is satisfied. The utility token is equivalent, in effect, to an unsecured, non-interest bearing promissory note issued in exchange for goods or services that may or may not exist yet.

In other words, revenue should be recognized at the time the token is presented to the issuing company for redemption into goods or services.

Further, due to the IFRS 15 requirement to defer revenue until the company's performance obligation is met, the issuing company should recognize a deferred revenue liability at the time of the ICO which will be converted gradually to income as the obligations (i.e. the provision of a product or a service) are performed.

TAX treatment of Utility Tokens

The tax liability of a Utility Token is, based on the above, deferred until the point the issuing company will be actually providing the goods or services. Therefore, at issuance there may be no tax liability for the issuing company.

Once the performance obligation is satisfied, i.e. when the issuing company will offer the service or product to the investor or user, then the associated income will be taxed under corporation tax at a rate of 12,5% on resulting net profits at the end of the financial year.

Utility Tokens can therefore be very attractive since they result in no equity dilution as the company does not issue new shares and at the same time it achieves tax liability deferral.

IP Company – Cyprus IP Box

Careful consideration of the specific characteristics of each case will be required in order to determine whether the company's technology will be considered as Qualifying Intangible Property and thus the income generated therefrom to qualify under the Cyprus IP Box and be subject to effective tax rate up to 2,5% as explained above.

VAT treatment of Utility Tokens

According to the EU VAT Law, a supply of services is rendered for consideration within the meaning of Article 2 of the VAT Directive and can therefore be subject to VAT, only if a direct link exists between the services supplied and the consideration received by the taxable person.

During the ICO stage, the issued tokens are used as a means of collecting funds for the development of future products and services by the issuing company. At this point, neither the service nor the corresponding price can be clearly identified. If the project undertaken by the issuing company is not successful, the investors might get nothing in return.

Having this in mind, it may be argued that at the time of an ICO, there is no direct link between the tokens issued and the services rendered and thus there is no taxable event. In other words, it may be argued that at the time of issue, the proceeds received do not fall within the scope of VAT and an ICO itself may not be regarded as a taxable event for VAT purposes in Cyprus in the case of Utility tokens.

Utility tokens and Multi-purpose vouchers

One could also associate the fundamental legal characteristics of Utility tokens with the so called multi-purpose vouchers for VAT purposes.

At the time of sale of a multi-purpose voucher, the voucher is not subject to VAT as there is difficulty in establishing the direct link between the payment of the voucher itself and the exact services to be offered. Only the actual handing over of the goods or services in return for a multi-purpose voucher is considered as a vatable event (Article 30b of amended VAT Directive).

In other words, multi-purpose vouchers will only be subject to VAT when the voucher is redeemed. No VAT will be due when the voucher is transferred through the supply chain. The value on which VAT should be accounted for, is either the net price paid by the consumer, or if that is not known, the net face value of the voucher.

The treatment of multi-purpose vouchers may be argued that is correspondingly applicable to Utility tokens and in effect at the time of an ICO, issued Utility tokens might not trigger a taxable event for VAT purposes. After the ICO, any future use of such tokens as a means of payment and access to products and services offered by the issuing company may be subject to VAT considering the particular facts of each case and the possibility of applying the exemptions provided by article 135 of the VAT Directive.

This argument is further substantiated by the fact that the opposite standpoint would lead to double taxation, as VAT would be applied both upon:

- The issue of a token and

- Its subsequent use as a means of payment for specific products/services provided by the issuing company.

The VAT treatment of the exchange of utility tokens with products and/or services of the issuing company should follow the VAT treatment of the underlying product (origin and destination of the products) or service (i.e. the place where the recipient of the service belongs).

If the place of supply of a transaction is considered to be within EU, then the VAT applicable rate in that Member State will apply. If the place of supply is considered to be outside EU, then the transaction is outside the scope of EU VAT Law.

Special Attention needed!

The VAT treatment of Utility tokens needs special attention and consideration once the Utility tokens will be offered within EU Member States to persons not exercising economic activities. In particular, in the case that the service offered is considered as an electronically supplied service, then the issuing company will have to:

- either register with all Member States to which it provides services to persons not exercising economic activities and apply the local VAT rate on the relevant supplies or

- to register with the Mini One Stop Shop (MOSS) system in Cyprus which enables the company to charge the VAT rate applicable in other Member States in a single declaration.

It is also important to clarify that the aforementioned VAT treatment applies both for companies established in a jurisdiction within and outside EU. If the services to be offered in exchange for utility tokens are considered as electronically supplied services, then the issuing foreign company (i.e. Swiss, USA, Cayman Island, BVI or of another jurisdiction company) has to:

- either get registered with all MS to which it provides services to persons not exercising economic activities and apply the local VAT rate on the relevant supplies or

- to register with the Mini One stop shop (MOSS) system in a MS of their choice (i.e. Cyprus) which enables the company to charge the VAT rate applicable to other MS in a single declaration.

As the omission of compliance with VAT provisions might entail criminal liability in addition to the heavy penalties in default, the issuers must consider seriously this aspect of ICOs and receive proper VAT advice on time, instead of receiving the heavy bills and possible prosecution afterwards!

III. Asset - Investment Tokens

These are tokens which have similar characteristics to:

- Equity shares in a company, entitling the holder to ownership rights, dividends or voting rights, or

- Bonds, entitling the holder to interest payments, or

- Derivatives, entitling the holder to payments linked to the performance of a specific asset of the company.

One may argue that the proceeds generated from an ICO with tokens having the above characteristics, do not meet the definition of Income under IFRS 15, explained above and should therefore be classified either as equity or as a liability in the books of the issuing company.

It remains to be seen though, if based on the prospective ICO regulations, if any, tokens classified as equity will be treated similarly to the share capital of the company or they will be treated as an additional reserve of the issuing company.

TAX treatment of Asset – Investment Tokens

As the issuance of Asset – Investment tokens might not be reflected in the income statement of the company as revenue, but instead in the equity or liabilities of the company in the Statement of Financial Position, it might not trigger any taxable event for corporation tax purposes.

If based on the prospective ICO regulation, if any, equity tokens are considered to have the same characteristics as the share capital of a company, they might be subject to once off capital duty of 0.6% in Cyprus, something that seems not to be applicable in tokens having similar characteristics with debentures (i.e. debt tokens).

One could also claim that in case the issued Asset – Investment tokens have similar characteristics with the share capital of a company, once regulated, they might also be eligible for Notional Interest Deduction (NID) on the new capital introduced into the company. For more details as to Notional Interest Deduction (NID) applicability please refer to our Tax Update which can be downloaded here.

Finally, if the issuance refers to debt tokens, equivalent of loans that carry an interest rate on the principal amount loaned to the company, such issuance would normally be reflected in the liabilities of the issuing company, generating no taxable income for the company.

If the proceeds generated from a loan related token are used in the production of taxable income, then any interest element associated with this taxable income should be considered as an allowable expense for tax purposes reducing thus the taxable base of the company.

VAT treatment of Asset - Investment Tokens

As with the utility tokens mentioned above, it is important to analyse what the investor gets in exchange for the Asset – Investment tokens.

As the relevant tokens give rise to dividends, or interest payments, we need to examine whether they fall within the scope of the exemption under Articles 135(1)(b) and (f) of the EU VAT Directive 2006/112/EC.

The above article specifically exempts:

- the granting and the negotiation of credit and the management of credit by the person granting it, and

- transactions (including negotiation but not management or safekeeping) in

i. shares,

ii. interests in companies,

iii. debentures and other securities,

Based on the above one may argue that Asset – Investment tokens will most probably qualify as an exempt transaction for VAT purposes and would therefore not create any VAT liability for the issuing company.

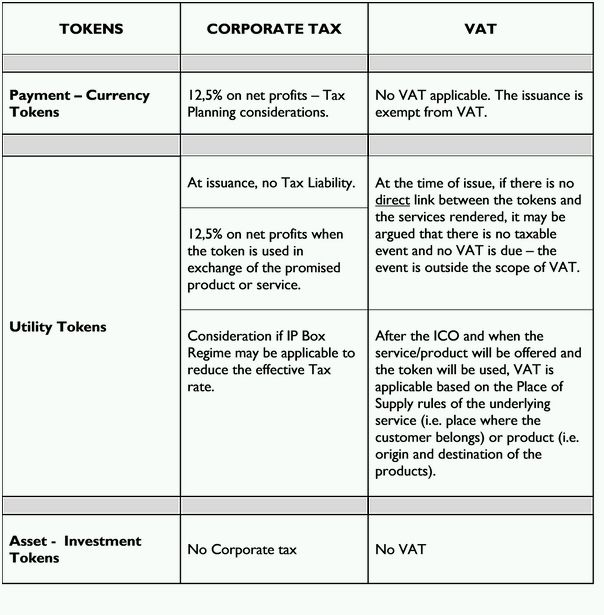

D. SUMMARY TABLE

The above discussed as to the VAT and TAX treatment of ICO tokens has been summarised in the below table for easy reference.

ICOs are an innovative and quick method for companies to raise capital but should not be seen as an easy way to circumvent laws and regulations. Even without specific regulation on the matter, an ICO would still need to meet the general provisions and requirements of other general laws, such as Contract Law, Financial Securities Laws, AML Laws, General Data Protection Laws, VAT Laws and Tax Laws.

The objective is always to have a proper structure that is able to attract potential investors or users and at the same time optimise corporate and indirect tax outflow, thus the choice of jurisdiction for the ICO-issuing entity is of utmost importance. The chosen jurisdiction should be an appropriate jurisdiction for both regulatory and taxation purposes.

Irrespective of the fact that currently there is no specific ICO regulation in place, Cyprus can still play a significant role in this field as its legal and tax legislation provide the required flexibility.

With the proper guidance and professional advice, an ICO through Cyprus, engaging, among others, a Cyprus company, may become a solid valuable method of financing companies and give a boost to innovative technology and infrastructure. – On this matter, you may refer to our publication, "Initial Coin Offering (ICO) through Cyprus" which you may download from here.

F. HOW KINANIS LLC CAN ASSIST

Our consultants, lawyers and accountants may assist potential ICO organizers on the following, subject to the project evaluation, based on Cyprus Law:

- Legal support for ICO procedure;

- Review and Consultation on Whitepaper to confirm compliance with Cyprus Legislation;

- Classification of Tokens to be issued;

- Drafting or review and consultation on Terms and Conditions of the token sale;

- Drafting or review of agreements between issuing company and other entities (if applicable);

- Drafting of Shareholder(s) agreements (if any);

- Notification to Authorities re: ICO project (if necessary);

- Drafting and review of the document listing the Risk Factors (if applicable);

- Tax Structuring and advice on the ICO Structure;

- Tax Rulings (if applicable);

- VAT review and advice on the ICO structure;

- VAT Rulings (if applicable);

- Formation of companies to be used in the project;

- Legal analysis of the Cyprus regulatory framework;

- Advise on AML, KYC, and Compliance issues – preparation of relevant manuals;

- Advise on Data Protection law issues - GDPR;

- Technical support on GDPR issues;

- Tax advisory;

- VAT advisory;

- Accounting issues;

- Support on banking issues and opening of bank accounts;

- Legal drafting and preparation of documents;

- Drafting and establishing of Trusts for beneficiaries / shareholders;

- Ongoing legal advising on the matter and related issues.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]