- within Environment topic(s)

CSRD

The EU Taxonomy Regulation, which entered into force in 2020 as a part of the ESG framework adopted within the European Union, created a classification system which defines the criteria for economic activities to be considered environmentally sustainable in order to reach the environmental goals, such as the net zero target by 2050, set out by the Green Deal.

The four environmental objectives of the EU taxonomy are:

- sustainable use and protection of water and marine resources,

- transition to a circular economy,

- pollution prevention and control, and

- protection and restoration of biodiversity and ecosystems.

The referred regulation imposed transparency and reporting obligations for non-financial and financial undertakings, and gives the Commission the power to adopt delegated and implementing acts which are obligatory for the competent authorities and market participants.

Based on the referred authorisation the following Acts have been adopted so far:

- Climate Delegated Act (2021) on sustainable activities for climate change mitigation and adaptation objectives of the EU Taxonomy.

- Disclosures Delegated Act (2021) on the specification of the content and on the presentation of information to be disclosed by undertakings subject to Article 19a or 29a of the Accounting Directive concerning environmentally sustainable economic activities and specifying the methodology to comply with that disclosure obligation.

- Complementary Climate Delegated Act (2022) on the acceleration of decarbonation by including, under strict conditions, specific nuclear and gas energy activities in the list of economic activities covered by the EU taxonomy.

- Environmental Delegated Act (2023) on the inclusion of a new set of EU taxonomy criteria for economic activities making a substantial contribution to one or more of the non-climate environmental objectives, such as: sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and control and protection and restoration of biodiversity and ecosystems.

Based on the EU corporate sustainability reporting framework, non-financial undertakings started reporting their taxonomy key performance indicators (KPIs) as of 1 January 2023, while in the case of financial undertakings, these started to be recorded as from 1st January 2024.

In order to provide further guidance and clarification on Corporate Sustainability Reporting Directive, 'CSRD' and sustainability reporting rules, the European Commission regularly publishes Frequently Asked Questions (FAQs), which are based on questions from the stakeholders subject to the reporting requirements, such as the Platform on Sustainable Finance, and, national and European supervisory authorities on a regular basis.

Two sets of FAQs were issued on the 13th November 2024. The first set of FAQs aims to support financial undertakings to implement the relevant rules of Article 8 of the Taxonomy Regulation, moreover, to provide further interpretative and implementation guidance to financial undertakings on the reporting of their KPIs under the Disclosures Delegated Act.

The other set of Frequently Asked Questions, published on the same day, intends to clarify certain provisions of the Sustainable Finance Disclosures Regulation, 'SFDR' and to provide more explanation to the interpretation of certain provisions on sustainability reporting introduced by the CSRD into the Accounting Directive, the Audit Directive, the Audit Regulation and the Transparency Directive.

The Commission also included some explanations regarding the first set of European Sustainability Reporting Standards, 'ESRS'. It is worth noting that guidance notes in this regard are also regularly issued by the European Financial Reporting Advisory Group `EFRAG`, which is a multi-stakeholder advisory body tasked with advising the European Commission on ESRS.

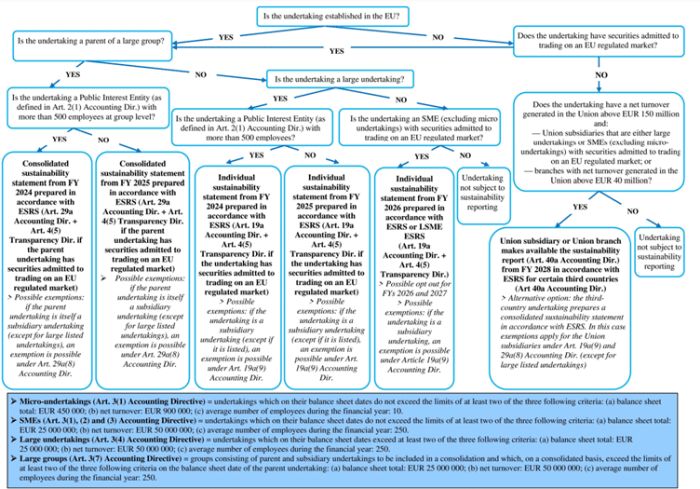

The FAQs confirm that all undertakings falling within the scope of Articles 19a and 29a of the Accounting Directive shall use, by default, the ESRS adopted under Article 29b of the Accounting Directive. However a list of exempt undertakings is included, which entities can report based on the ESRS LSME , which is ESRS for Listed SMEs.

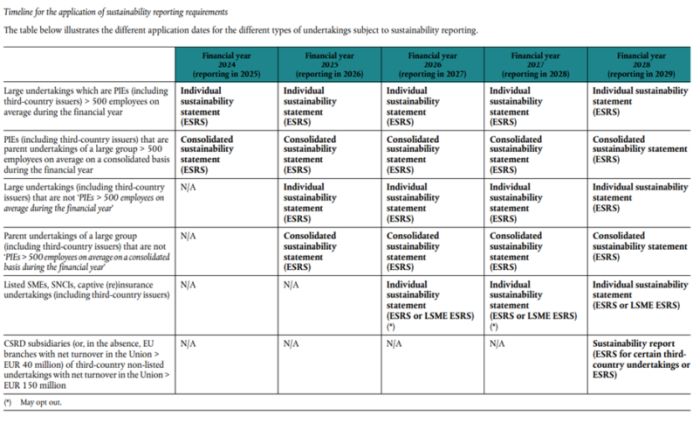

The below flowcharts, published within the FAQs, illustrate the process to determine whether an entity is subject to sustainability reporting requirements and from which financial year:

Source: EUR-Lex - 52024XC06792 - EN - EUR-Lex

Source: EUR-Lex - 52024XC06792 - EN - EUR-Lex

The FAQs provide more guidance on the concept of 'reasonable effort', which is used to determine when an undertaking shall report an estimate of value chain information instead of reporting information collected from actors in its value chain. Additionally further clarifications are provided on certain taxonomy reporting requirements, on the applicable language, on the digitalisation, on digital tagging and on the publications of the sustainability reports. Finally, there are further details on the assurance of the sustainability reporting, on key intangible resources and on the non-material indicators referred to by the SFDR.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.