- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Healthcare and Technology industries

Executive summary

The 2025 Canadian venture capital market was defined by a contraction in both deal volume and total capital deployed. In a difficult exit environment, secondary transactions emerged as an increasingly vital source of liquidity for investors. Despite tightened fundraising conditions across the ecosystem, AI‑focused startups remained a notable bright spot in a maturing Canadian market— drawing significant investor interest in their respective rounds

Canadian startups experienced a challenging fundraising environment in 2025, driven by macroeconomic uncertainty and geopolitical disruption. The distribution of financings reflected the prevalence of early‑stage financings (pre‑seed and seed financings) vs mid‑stage (Series A and Series B) and later‑stage (Series C and later) financings. This distribution is consistent with years prior and in‑line with a well‑functioning startup ecosystem where many early‑stage companies can obtain financing, but few are able to scale and achieve the desired product‑market fit.

The state of play also affected large late‑stage financings, with many characterized by secondary transactions. These secondary components allowed for an efficient deployment of capital and provided early investors and employees of startup companies with access to liquidity. A frequent trend observed in our practice was the prevalence of insider rounds. These were generally on unchanged terms but included warrants and other sweeteners or offered fundraising through the issuance of convertible instruments such as SAFEs or convertible notes as a stop‑gap measure.

Overall, 2025 illustrated a lack of growth in venture financings, but without the substantial investor friendly terms that we observed in 2021. The challenging financing market notwithstanding, there remained year‑over‑year stability in deal terms, confirming a resilient venture market despite ongoing headwinds.

The political and global macroeconomic forces that drove fundraising challenges in 2025 have continued into Q1 2026. Looking ahead, a continuation of these conditions may result in an ongoing steady state of bridge round financings as a means of deferring valuation discussions. For those who need to raise funds, there may be an increase in down rounds

2025 financing activity in Canada

Regional disruptions and sectoral shifts resulted in fewer deals and less capital distribution, but the market continued to show resiliency through rising valuations.

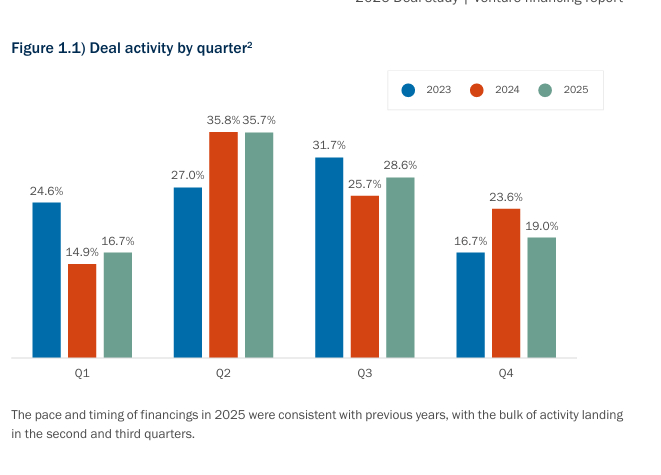

1) Deal activity

The topline number of financings in 2025 was down from 20241, with decreases in mid‑stage financings (Series A and Series B) relative to the proportion of early‑stage and later‑stage financings (Series seed, Series C and onwards).

Despite lower activity compared to years prior, valuations continued to rise—reflecting the ability for well‑placed and well‑performing startups to secure funding despite a challenging investment environment.

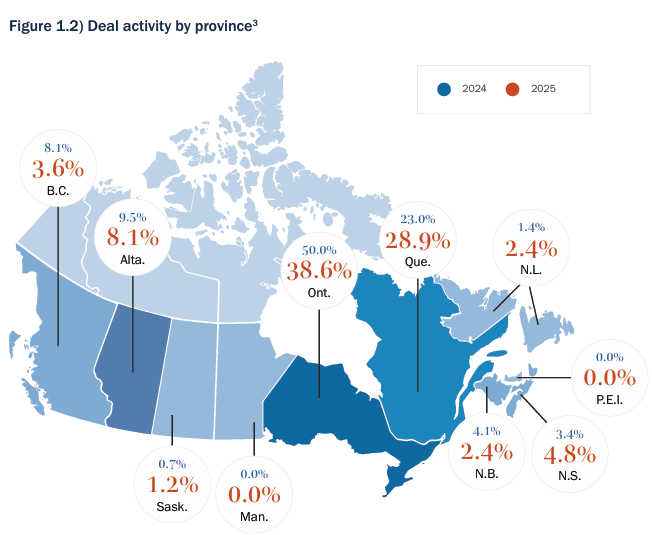

Deal volume mirrored the same geographic distribution as years prior, with Ontario accounting for the highest number of venture transactions, followed by Québec and Alberta.

Companies within the information technology sector saw the greatest number of financings, followed by healthcare and business‑to‑business products and services, respectively

Ontario and Québec dominated in deal volume, maintaining their long‑standing position as Canada's most active venture hubs. Alberta and Québec continued to attract strong early‑stage investment, reflecting the steady growth and increasing maturity of their respective ecosystems.

To view the full article clickhere

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.