"Albertans are currently being appropriately compensated for the production and sale of their oil, gas and oil sands resources."

- Alberta Royalty Review Advisory Panel (January 29, 2016)

On January 29, 2016, the Alberta Government announced that it will adopt the recommendations of the Royalty Review Advisory Panel (the "Panel") from the Alberta at a Crossroads, Royalty Review Advisory Panel Report (the "Report") to modernize Alberta's royalty framework. The common-sense adoption by the Alberta Government of the Report prompted a collective sigh of relief across Alberta and the energy industry.1

The Report is extensive and not only recommends a new modernized royalty framework emulating a "revenue minus costs" approach but provides an educational summary of how the energy industry functions in the Province, how royalties are influenced by market conditions, and the global competiveness of Alberta's regime. Ultimately, the Report provides a harmonized royalty strategy across all hydrocarbons, aimed at rewarding innovation, efficiency and low-cost producers, while leaving oil sands royalties substantively as-is but with more transparency and financial reporting.

In addition to providing an overview of the new royalty framework, this article provides a summary of the Panel's key findings and a timeline for implementation. The new modernized royalty framework ("MRF") requires a "Calibration Period" to finalize specific formulas and set up procedures for implementation. Those key formulaic and final inputs are scheduled to be released by the Calibration Period Committee on or before March 31, 2016.

A. KEY FINDINGS & CONCLUSIONS

1. Alberta's Oil and Gas Industry

The Report has educational undertones, and provides a clear and concise overview of royalties in Alberta, including how commodity prices and costs influence royalties, the relationship between investment, industry's returns and royalties, and facts and statistics to illustrate the discussion. Some of the noteworthy facts and statistics are reproduced below.

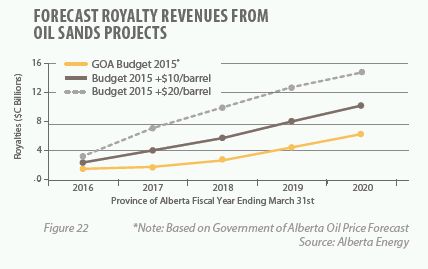

- The majority of Alberta's royalty revenues come from oil sands production. In the 2014/15 fiscal year, Alberta collected approximately $8.3 billion in total royalty revenues ($5.1 billion from the oil sands).2

- It is projected that for the 2015/16 fiscal year royalties will fall to approximately $2.8 billion (67% decrease year-over-year).3

- The upstream energy industry accounts for 23% of Alberta Gross Domestic Product.4

- The past five years have seen costs as a percentage of revenue rise beyond 80%. For the first time since 1960, close to 100% of a barrel's value was consumed by costs in 2012 and 2013.5

- As of 2014, Alberta was the eighth-largest producer of oil in the world, the eighth-largest producer of natural gas in the world, and the ninth-largest exporter of crude oil.6

2. New Challenges – A New Reality

In justification of its recommendations, the Panel discussed at length the changing global energy landscape and the new challenges facing Alberta's industry. Some of these "new challenges" include:

- Alberta's biggest customer is now its biggest competitor.7 Over the last 7 years, the dynamics with the United States (the "U.S.") have shifted because the U.S. is now producing huge volumes of oil and natural gas closer to key markets at lower costs with more infrastructure for upgrading, refining and transportationthan Canada.8 By way of comparison, in 2014, average U.S. shale gas production was over 37 billion cubic feet (Bcf) per day and Alberta's average was approximately 10 billion Bcf per day.9

- Oil and gas are no longer scarce resources.10 The same technological advances that resulted in the U.S. resurgence in oil and gas production have had the same effect around the world, and Alberta is now only one of many places where significant amounts of oil and gas can be produced.11

- Patterns in oil and gas demand, while strong, are also shifting as renewable sources of energy become more economically viable.12

- Canadian oil and gas producers have higher average operating costs relative to the global average.13

- Alberta Energy has estimated that discounts on Alberta's oil prices due to constrained market access have led to the forfeiture of more than $6 billion in royalties since 2010.14

- Overlaying these dynamics is an international tug-of-war for global oil market share. Saudi Arabia and other members of the Organization of Petroleum Exporting Countries have continued to maintain strong production in an effort to push down global oil prices and challenge U.S. and Alberta unconventional oil producers for market share.15

3. Alberta versus Canada and the World?

Part of the Panel's mandate was to compare Alberta's royalty regime to comparable jurisdictions in Canada and globally in order to determine its competitiveness.16 In order to do this, Wood Mackenzie, an international consultancy, was engaged to complete a fiscal comparative analysis. A full copy of the Wood Mackenzie analysis with commentary from the Panel is attached to the Report.17

Generally, the Panel determined that Alberta's royalties are comparable to similar jurisdictions, but the industry's costs are substantially higher. Within Canada, Saskatchewan's royalty regime is more favourable for investment for similar-type unconventional oil wells, while British Columbia's regime imposes lower rates than Alberta for natural gas.18

B. THE MODERNIZED ROYALTY FRAMEWORK

The stated goal of the MRF is to create a simpler, more transparent and efficient royalty system that encourages investment, creates jobs, and enhances economic activity in Alberta.

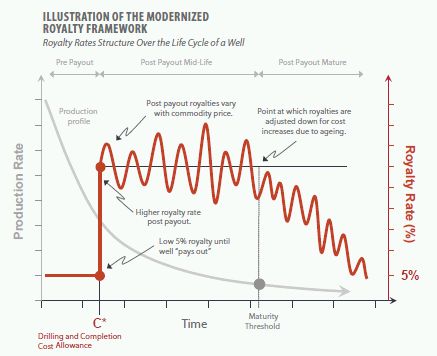

The MRF is divided by industry segments: conventional, unconventional, oil sands and value-added upgrading. First, all hydrocarbons (crude oil, liquids and natural gas) will be subject to a harmonized "revenue minus costs" approach with changes only applying to new wells spud in 2017 and thereafter (for wells drilled prior to December 31, 2016, existing royalties will remain in effect for 10 years).19 Second, Alberta's oil sands royalty framework will remain unchanged, subject only to new measures to increase transparency with respect to a project's allowable capital costs and financial reporting.20 Third, the Report recommends consideration of certain value-added partial upgrading investments.

1. A "Revenue minus Costs" Approach for Crude Oil, Liquids and Natural Gas

Pursuant to the Panel's report and recommendations, the Province will adopt the MRF in respect of crude oil, liquids and natural gas. The MRF will only apply to new wells spud after the implementation date of the framework (2017), provided however that a sunset provision will be established to transition exempt wells into the MRF 10 years from the implementation date of the framework.

As set out below, the MRF will undertake 5 actions:

| Action | Implementation |

| Harmonized Royalty Structure |

|

| Proxy "Revenue Minus Costs" Structure |

|

| Capital Cost Index |

|

| Implementation of Strategic Programs |

|

| Calibration of the MRF |

|

2. Oil Sands Royalties – Transparency and Public Reporting

The Panel found that the existing royalty structure for oil sands used a full revenue minus costs implementation that is consistent with global constructs for pre-payout and post-payout profit sharing between operating companies and resources owners.22 In addition, the current oil sands royalty framework is poised to deliver significant royalties post payout (as some projects begin to reach payout in the early 2020s).23

The Panel also concluded that future production growth from the oil sands is likely to be in the form of smaller-scale in-situ projects or the expansion of existing projects.24 For these reasons, the new royalty framework will not affect current oil sands royalty rates. Instead, changes will be made to the Oil Sands Allowed Costs (Ministerial) Regulation25 (which sets out the costs which are deductible when calculating oil sands royalties) in order to improve transparency, to ensure that companies face stern, fact-based decision-making in respect of allowable costs, and to create enhanced predictability, consistency and promptness regarding decisions in respect of the applicability of cost rules.

In addition to increased transparency and monitoring of oil-sands costs, the Panel recommended publication of a financial summary of each oil sands project, including:

- Revenue

- Capital Costs

- Operating costs

- Diluent cost

- Return allowance

- Realty dollars collected

- Gross revenue net of diluent

- Net revenue

- Gross revenue per barrel

- Bitumen production

- Royalty rate

3. Exploring Opportunities for Value-Added Processing

The Panel suggested two main opportunities for increased value-added processing in the Province.

First, the Panel recommended that the Province develop a value-added natural gas strategy. As part of that process, the Government is to undertake a review of Alberta's natural gas options, and develop an action plan to establish a fiscal and policy framework to encourage investment in value-added activities for natural gas while maintaining the goal of being a leader in environmental stewardship.

The second opportunity identified by the Panel concerned opportunities to accelerate the development and commercialization of partial upgrading and alternative value-creation technologies for bitumen.26 The Panel recommended that the Government undertake a review of such advancements, and highlighted that the success of such technology investments would enable Alberta to realize expanded crude marketability, expanded export capacity and a lower environmental footprint for a portion of the Province's bitumen production, as well as hedge against a future in which transportation fuel demand is disrupted.

C. TIMELINE AND KEY DATES

The following timeline and list of key dates assumes that the Alberta Government will implement all recommendations proposed within the Report in accordance with the suggested timeframes. As such, this summary should be used only as an outline of the anticipated timelines pending confirmation from Alberta Energy.

| Date | Action Item |

| March 31, 2016 |

|

| March 31, 2016 |

|

| March 31, 2016 |

|

| March 31 Annually |

|

| November 2016 |

|

| December 31, 2016 |

|

| June 2018 |

|

Footnotes

[1] Alberta, Royalty Review Advisory Panel, Alberta at a Crossroads (29 January 2016).

[2] Report at 21.

[3] Ibid.

[4] Alberta Treasury Board and Finance, as cited in the Report at 24.

[5] Report at 33.

[6] Report at 20.

[7] Ibid.

[8] Ibid.

[9] Report at 27.

[10] Report at 21.

[11] Ibid.

[12] Ibid.

[13] Report at 38.

[14] Report at 29.

[15] Ibid.

[16] Report at 46-47. The Panel used two criteria to determine which jurisdictions should be used in the comparative fiscal analysis. The two criteria were: (i) comparable resources (i.e. similar geologic play types similar in character and scale to Alberta) and (ii) capital competiveness (Wood Mackenzie considered only jurisdictions open for free market investment to companies currently operating in Alberta). The following competitor and comparator groups were selected: Natural Gas: British Columbia, Pennsylvania, Ohio, Texas, United Kingdom; Crude oil and liquids – Saskatchewan, Colorado, North Dakota, Oklahoma, Texas, Argentina, Colombia; Oil sands – California, Madagascar, Oman, Venezuela, Newfoundland and Labrador, Alaska, Deepwater Gulf of Mexico, Brazil, Kazakhstan, Norway.

[17] Wood Mackenzie Analysis is attached to the Report starting at PDF page 107.

[18] Report at 47.

[19] Report at 60.

[20] Report at 66.

[21] Report at 61, Figure 21 (formula equal to C* =a1*(TVD)+a2*(TVD-V deep)+a3*(TVD*TLL), where: (i) TVD is the true vertical depth of the well; (ii) Vdeep is the vertical depth threshold applicable to all wells, beyond which a well begins to receive additional capital cost allocation; (iii) TLL is the Total Lateral Length; (iv) a1 is a capital cost allocation for every meter drilled vertically; (v) a2 is a capital cost allocation for every vertical meter drilled deeper than Vdeep; and (vi) a3 is a capital cost allocation for every meter drilled horizontally, for every meter drilled vertically).

[22] Report at 52.

[23] Report at 80.

[24] Report at 37.

[25] Alta Reg 231/2008 (the Panel also recommended consultation regarding any changes to this regulation to ensure that any chances reflect current market conditions and Alberta's overall strategy, Report at 66).

[26] Report at 13 (at a high level, partial upgrading is the processing of bitumen to reduce the thickness by removing proportions of the heaviest fraction of the bitumen barrel. Partially upgraded bitumen can flow in a pipeline with little or no diluent, which can increase export pipeline capacity by as much as 30%).

[27] Report at 60.

[28] Ibid.

To view original article, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.