- within Compliance, Family and Matrimonial and Wealth Management topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- in Canada

- with readers working within the Banking & Credit and Healthcare industries

Replay the Economic Outlook seminar presented

at the Calgary office of Bennett Jones on November 23.

Replay the Economic Outlook seminar presented

at the Toronto office of Bennett Jones on November 28.

After a marked slowdown in 2016, the global economy is experiencing robust, synchronized growth in 2017, which exceeds earlier expectations and should continue in the short term. Notwithstanding this improved outlook, uncertainty about future economic policy and geopolitical developments remains very significant, if not even greater than before. Moreover, financial vulnerabilities, population aging, and weak productivity growth continue to weigh on prospects going into the medium term.

In Section I, we summarize recent developments in the world economy and present a base-case projection to 2019. In Section II, we discuss four economic risks and some of their implications for Canada. These risks relate to possible U.S. fiscal/tax changes; trade negotiations, especially regarding NAFTA; monetary policy decisions under uncertainty; and China's economic plan. Section III is a special-topic section in which we elaborate on the challenges that central banks currently face in conducting monetary policy under conditions of "radical" uncertainty. In Section IV, we deal with the likely process and possible outcomes of trade negotiations, particularly with regard to NAFTA, and their implications for both government and business strategy in Canada. In Section V, we present our take on the economic implications of the recent 19th Communist Party Congress in China. Finally, in Section VI, we focus our attention on the implications of our analysis for key planning parameters for Canadian business going forward.

SECTION I: GLOBAL GROWTH TO 2019

Recent Developments

The world economy experienced subdued growth in 2016, much below the trend experienced over 2011 to 2015 and a fortiori before the 2008 crisis. In the second half of 2016, however, a few countries started experiencing faster growth and that strengthening spread to many advanced and emerging economies in the first half of 2017. Indicators generally point to continued solid global growth in the third quarter.

Real gross domestic product (GDP) growth accelerated in both advanced and emerging economies in the first half of 2017, with particularly impressive gains in Japan, the euro area, Canada, Russia and Brazil, and slightly increased growth in China. The United States, the United Kingdom and India were notable exceptions, although in the case of the U.S. growth firmed up to a brisk pace in the second and third quarters following a soft patch in the first. In the advanced economies, growth largely originated from a strengthening of domestic demand supported in part by improved confidence levels, accommodative financial conditions and a slight positive impulse from discretionary fiscal policy. In the United States and Canada, there was a marked pick-up in business non-residential investment growth, partly reflecting some revival of investment in the oil and gas sector.

Expectations that economic slack would soon disappear, if it had not already done so, and that currently subdued inflation was set to pick up in the near term led the U.S. Federal Reserve to start monetary policy normalization in December 2016 and to continue it at a moderate pace in 2017, with 3 increases of 25 basis points in the target range for the Federal Funds rate in March, June and October. In Canada, the unexpectedly strong growth of output and employment beginning in the second half of 2016 prompted the Bank of Canada to raise the target overnight rate a bit earlier than generally projected previously, by 25 basis points in July and again in September.

Diminishing prospects for implementing tax and other growth-enhancing measures promised by the Trump administration led to a significant depreciation of the U.S. dollar from its year-end 2016 level, particularly against the currencies of countries experiencing comparatively strong growth momentum, notably the euro. The Canadian dollar largely appreciated against the U.S. dollar only in the summer, when expectations of an earlier start of monetary policy normalization firmed up and were subsequently validated by the Bank of Canada.

In spite of stronger global growth, international oil prices mostly moved sideways in the year to October 2017 as increased demand was met by an expansion of supply from two sources: ample inventories were drawn down and non-OPEC production increased. Around the end of October, however, political developments in Saudi Arabia pushed the West Texas Intermediate (WTI) oil price up from about US$52 to an expected level of US$57 in the December 2017 futures market. These futures are currently calling for a slow price decline starting in the second half of 2018, which would bring the annual average for 2018 to US$56 from US$51 projected for 2017. These annual averages are fully consistent with the views that we have maintained in the last year that WTI oil prices would experience a slight upward trend but, barring escalating tensions in the Middle East, would not durably remain at or above US$60 during 2018. Nevertheless, the evolving geopolitical situation in the Middle East is likely to contribute to greater volatility in oil prices than over the last two years.

Base-Case Projection

As in our Spring 2017 outlook, but to a greater extent now, faster demand growth is expected to raise real GDP growth rates in the world economy in 2017–2019, to 3.5 percent, well above the 3.2 percent experienced in 2016. This scenario reflects several key factors and assumptions:

- The adverse effects on growth of the earlier shocks that have contributed to depress demand up to 2016 have essentially disappeared. These shocks include the global financial crisis, the European debt crisis, and the fall in the prices of oil and other commodities. These shocks have had different impacts on different countries, but there is evidence that the negatively affected countries have recovered or are recovering from their effects. Moreover, advanced economies shifted their fiscal policy stance from austerity to neutral or slightly expansionary starting in 2016.

- As they anticipate inflation to rise to target levels in the short term, monetary authorities indicate they plan to increase policy rates in 2017–2019, but at a pace that is expected to be gradual and "data dependent". Policy rates should therefore remain accommodative, i.e., below estimated neutral levels, at least through 2018 (see Sections II and III).

- The projected pick-up in demand and the rise in capacity utilization will, in turn, have positive spillover effects on business investment and international trade, thereby providing a positive feedback effect on aggregate demand and eventually on potential output.

- China continues to pursue a policy of infrastructure investment and domestic credit expansion that will allow real GDP to grow at rates consistent with earlier targets in the short term (see Sections II and V).

- No financial disruption arises in 2018 or 2019 from rising interest rates and high levels of consumer debt and house prices in some advanced economies or from excessive debt of dubious quality in China.

- As before, WTI oil prices are assumed to trend upwards in the short term, but would not durably remain at or above US$60 during 2018. For planning purposes, and barring an escalation of geopolitical tensions in the Middle East, we assume an average price of US$55 in 2018 and US$60 in 2019, compared with a projected US$51 price in 2017. More than a projected slight upward trend, what will dominate oil price movements in the short term is their high volatility, especially in a context of changing geopolitical tensions in the Middle East.

- Negotiations regarding NAFTA drag on until the first half of 2019, after the U.S. mid-term elections, causing uncertainty. But we assume that in the end some sort of arrangement will be reached that would allow continued high levels of trade between the partners. Uncertainty about the outcome of the negotiations slightly holds back GDP growth in Canada (and to a lesser extent in the United States) in 2018–2019 through lower business investment than would otherwise be the case (see Section II and IV).

Based on these assumptions, global growth is expected to rise to 3.5 percent per year in 2017 and 2018 from 3.2 percent in 2016, with the expansion accelerating in both advanced economies (to around 2 percent from 1.5 percent and emerging economies other than China (to around 3.5 percent from 3.2 percent). Global growth diminishes marginally to 3.4 percent in 2019 as advanced economies only expand at close to their potential rate in the absence of significant economic slack and the expansion in China slows a bit.

Short-Term Prospects for Output Growth (%)*

|

World Output Share (%) |

2011 to 2016 | 2016 | 2017 | 2018 | 2019 | |

| Canada | 1.5 | 2.1 | 1.5 | 3.1 (2.0) | 2.1 (2.0) | 1.6 (1.7) |

| United States | 16.4 | 2.1 | 1.5 | 2.2 (2.3) | 2.3(2.3) | 2.0(1.9) |

| Euro Area |

12.3 |

0.9 | 1.8 | 2.2(1.5) | 1.9(1.5) | 1.6(1.5) |

| Japan | 4.6 | 1.0 | 1.0 | 1.5(0.6) | 1.0(0.5) | 0.8(0.7) |

| Advanced

Economies1 |

34.8 | 1.5 | 1.5 | 2.1(1.8) | 2.0(1.8) | 1.7(1.6) |

| China | 17 |

7.7 |

6.7 |

6.8(5.7) | 6.5(5.2) | 6.3(5.9) |

| Rest of World | 48.2 | 3.6 | 3.2 | 3.3(3.2) | 3.6(3.2) | 3.6(3.6) |

| World | 100 | 3.6 | 3.2 | 3.5(3.1) | 3.5(3.0) | 3.4(3.4) |

* Figures in brackets are from the Bennett Jones Fall

2016 Economic Outlook for 2017 and 2018 and from the Spring 2017

Economic Outlook for 2019.

1 Weighted average of Canada, United States, euro area

and Japan.

A year ago we believed that even with a cyclical rebound in advanced economies in 2017–2018 the world economy was set to grow at 3 to 3.25 percent to the end of the decade compared with about 3.5 percent over 2011–2016 and 5.1 percent over 2003–2007, a period of high and rising commodity prices accompanying 12 percent growth in China. We now believe that the world economy is likely to grow by about 3.5 percent per year to the end of the decade. This improvement relative to the Fall 2016 outlook comes only partially from more growth in advanced economies, which are now projected to grow a bit faster in the short term largely stemming from the euro area and Japan. The main improvement comes from an upward revision to our previous, perhaps overly pessimistic, view of growth prospects in China, and from a universally more optimistic view of prospects for the rest of the world, which will benefit from the direct and indirect effects of strong Chinese demand.

The sustainability of solid global growth going into the medium term hinges on two important adjustments. In advanced economies there ought to be a shift of aggregate demand from consumption to investment, both to expand potential output and to reduce financial vulnerability. A change in policy mix—less accommodative monetary policy and a fiscal policy oriented toward infrastructure investment—would promote such a shift. In China, on the other hand, we think policy to facilitate the rebalancing of demand from investment to consumption and of production from manufacturing and construction to services should gain momentum (see Section V). These complementary adjustments in advanced economies and China would reduce global imbalances and hence the risks of increasing protectionism and sharp financial correction. To some extent such adjustments are factored into our projection.

United States

U.S. growth is projected to rise to above-trend rates of 2.2 percent in 2017, 2.3 percent in 2018 and 2.0 percent in 2019, supported by a strong labour market, strengthening investment, including in the energy sector, less drag from net exports at the current U.S. dollar exchange rate, and an assumed small positive fiscal impulse from tax cuts.

On the assumption (preferred by the Federal Reserve) that temporary supply shocks affecting particular prices dissipate, inflation should rise to the 2 percent target in a context of little or no slack in the economy. On that basis, the Federal Reserve is expected to continue raising the target range of its Federal Funds rate gradually to bring it to around 2 percent by the end of 2018 and likely closer to the 3 percent median estimate of the neutral rate by the end of 2019.1 With policy rate normalization under way, and in accordance with its recent declared intentions, the Federal Reserve has started in October to reduce slowly the size of its balance sheet. This likely will bring a modest rise in long-term interest rates relative to short-term rates (the term premium). The rise in real interest rates resulting from policy rate increases and balance sheet reduction would tend to slow aggregate demand growth to a rate consistent with potential growth and help keep the economy in balance. Complicating this task, however, is as always much uncertainty about possible economic shocks. But now there is also more uncertainty about the analysis of the inflation process itself. Evolving changes in this analysis may prompt the Federal Reserve to revise the pace or extent of its monetary policy normalization (see Section III).

Another source of uncertainty concerns the prospects for tax cuts and the stimulative effects that these cuts might have in the short term when the economy is at, or near, full employment (see Section II). The latest House bill allows for tax cuts, but limits their impact on the budget deficit through deduction cuts and other deficit-reduction measures to some $1.5 trillion after 10 years by Republican calculations.

The House proposal will need to be reconciled with a proposal from the Senate along the same lines before a final bill is passed. At the time of writing this report, there were significant differences between the House and Senate proposals which may necessitate a rather protracted process of negotiations and adjustments before reconciliation is achieved. One difference of consequence for our projection is with respect to the timing of the planned corporate tax rate cut from 35 to 20 percent. The House proposal has this cut taking effect in 2018 whereas with the Senate proposal it would become effective only in 2019. For our projection we make the assumptions that the corporate tax cut will be effective in 2018 and will generate a net fiscal impulse of around 0.8 percent of GDP in that year, thereby boosting real GDP growth by 0.2 percentage point in 2018 and by less than 0.1 point in 2019 (see Section II). These positive effects, however, are expected to be offset in small measure by the negative effects on growth of another shock—the uncertainty surrounding the outcome of the NAFTA negotiations. Such uncertainty, which is assumed to persist until late in 2019, would lead to somewhat less business investment than otherwise in 2018 to 2019 (see Section II).

China

Growth in China should reach 6.8 percent in 2017, but slow to 6.5 percent in 2018 and 6.3 percent in 2019. This is a considerably more buoyant scenario than we envisioned last spring, but one that entails the risk of increasing financial vulnerabilities. This projection is consistent both with the expected impact of current monetary and fiscal policies in 2017 and 2018 and the new emphasis of economic policy on the quality of growth that was articulated during the 19th Congress (see Section VI), which will have an impact only starting in 2019. In Section II, we discuss the risks involved and in Section VI, we give our take on the implications of the latest 19th Congress.

Other Advanced Economies

Growth in the euro area is projected to accelerate to 2.2 percent in 2017 and moderate to 1.9 percent in 2018 and 1.6 percent in 2019, all much higher rates than the average growth recorded over the 2011–2016 period. The acceleration in 2017 stems from improved confidence, very accommodative financial conditions, mildly expansionary fiscal policy and a pick-up in world trade and growth. In the short term, domestic demand leads the recovery with monetary policy very accommodative throughout and fiscal policy essentially neutral to mildly supportive. The considerable appreciation of the euro in 2017 would tend for a while to moderate the favorable impact of solid global growth on exports. This being said, the level of the euro remains relatively favorable by historical standards, which may partly explain why in spite of its considerable appreciation in the last year, growth in the euro area has remained robust.

With inflation rising only moderately toward its target during 2018, the European Central Bank (ECB) is likely to start raising its policy interest rate no earlier than late 2018, although it will proceed with a halving of its bond purchase program to €30 billion a month from January 2018 onwards. The ECB has not set an end date yet for the bond purchase program per se. The short-term interest rate differential in favour of the United States should widen through 2018 and narrow during 2019, thereby keeping a lid on, if not weakening, the euro in 2018 before some reversal in 2019.

Growth in Japan is set to rise to 1.5 percent in 2017 on the strength of export gains and fiscal stimulus. Fiscal support is projected to fade in 2018, as previously scheduled, but employment and business investment should be buoyed by labour and capacity shortages and very high profits. Growth declines to 1 percent in 2018 and 0.8 percent in 2019, near its potential by conventional estimates.

Canada

Current information suggests that growth in Canada will slow considerably in the second half of 2017 from its torrid pace in the first half, but will still be significantly above potential. Consequently, for 2017 as a whole, growth is projected to rise to 3.1 percent, twice as fast as in 2016, and to decelerate to 2.1 percent in 2018 and 1.6 percent in 2019, in the vicinity of the potential rate. Consumer Price Index inflation is expected to rise in response both to pressures on capacity and the firming up of wage growth as labour market slack dissipates. In the latest Bank of Canada Monetary Policy Report (October 2017) inflation would reach its 2 percent target2 in the second half of 2018 and remain there to the end of 2019.

Monetary authorities are set to move cautiously in raising the policy interest rate in the short term as they emphasize "data dependence" in conducting monetary policy: "...the Bank will be guided by incoming data to assess the sensitivity of the economy to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and price inflation."3 We therefore expect the target overnight rate to rise to about 1.75 percent by the end of 2018 and to 2.5 to 3 percent by the end of 2019, the bottom half of the range of Bank of Canada estimates of the neutral rate. Fiscal policy, on the other hand, should have a modest expansionary effect in 2017–2019, although it is hard to judge by how much, if only because the pace of federal investment in physical infrastructure over the next two years remains highly uncertain.

The slowing of growth in 2018–2019 largely reflects a softening of consumption and housing as households adjust to rising interest rates and to macroprudential and other housing policy measures. Business fixed investment and net exports, on the other hand, should increase their contributions to GDP growth relative to 2017. Pressures on capacity, comfortable profit margins and expectations of a solid expansion of sales accompanying global growth would stimulate business investment. But uncertainty about the outcome of the NAFTA negotiations will likely reduce intended investment, at least temporarily (see Section II). Net exports should benefit from the projected strength of United States and overseas demand and expansion of domestic industrial capacity as long as the Canadian dollar continues to trade at about 80 U.S. cents.

SECTION II: RISKS TO THE PROJECTION

The evolving geopolitical situation presents downside risks to growth, which cannot be properly measured and so far have been largely ignored by financial markets. At the same time, economic policy uncertainty has intensified in part because of the unpredictable actions of the Trump administration, in part because unexpectedly subdued inflation in advanced economies has left monetary authorities perplexed, and in part because Chinese authorities face a choice: high growth versus structural transformation, financial stability, and a clean environment.

In this section, we briefly outline what we consider to be four key risks to our base projection: future tax cuts in the United States; NAFTA negotiations; monetary policy normalization; and China's growth strategy.

Future Tax Cuts in the United States

The details of the fiscal reform that will probably emerge from the U.S. Congress remain to be worked out at this point. Nevertheless, the current House bill suggests that cuts in personal and especially corporate tax rates will be partly financed by reductions in certain deductions and credits and other deficit-reducing measures so that the tax reform would generate a cumulative deficit of about $1.5 trillion over 10 years by Republican calculations. Under budget rules congressional Republicans are using to pass a tax plan without Democratic help, the bill can only increase deficits by $1.5 trillion over 10 years before any induced growth is taken into account. It is highly questionable that the currently proposed bill would meet this requirement. According to the Congressional Budget Office, for example, the plan would increase budget deficits by $1.7 trillion over 10 years. In any event, the House bill will need to be reconciled with a proposal from the Senate along the same lines before a final bill is passed. At the time of writing, there were serious considerations given to include in the Senate proposal both a repeal of Obamacare's requirements for Americans to have health insurance and an increase in child tax credit.

The significant differences between the House and Senate proposals may require a rather protracted process of negotiations and adjustments before reconciliation is achieved. One difference of consequence for our projection is with respect to the timing of the planned corporate tax rate cut from 35 to 20 percent. The House proposal has this cut taking effect in 2018 whereas with the Senate proposal it would become effective only in 2019. For our projection, we make the assumption that the corporate tax cut will take place in 2018.

In constructing our outlook, we have assumed that the eventual bill passed by Congress and signed by the president in 2018 will result in a net fiscal impulse of around 0.8 percent of GDP in 2018. This would boost real GDP growth by 0.2 percentage point in 2018 and less than 0.1 point in 2019. This relatively modest reaction, based on a fiscal multiplier of only 0.3,4 stems from two main factors. First, the impulse originates from tax cuts, much of which will be saved rather than spent. The great bulk of the personal tax reductions would accrue to higher-income households, who have a larger propensity to save than average. As well, corporate fixed investment has been rather insensitive to increases in profits in this business cycle. Hence corporate tax cuts per se are more likely to induce increased dividends or buybacks than GDP-enhancing investment in plant, equipment or R&D. But to the extent that tax cuts do increase domestic demand, with an economy already at or near full employment, they would fuel inflationary pressures and prompt monetary authorities to raise their policy rate more than otherwise, which in turn would likely entail some more appreciation of the U.S. dollar with a resulting decline in net exports.

Our fiscal assumptions are not without risks. The final Republican bill to be voted on may have the corporate tax cut becoming effective only in 2019, in line with the Senate proposal. This would shift some of the direct positive impact of the tax cuts on real GDP growth from 2018 to 2019. The size of the fiscal impulse could be larger or smaller depending on the size of the final changes in deductions and rates. Moreover, the fiscal multiplier could turn out to be a little larger or even somewhat smaller than we have assumed. Finally, it is very hard to judge the interaction effect of changing trade and tax policies on the investment behaviour of firms. All this to say that any estimate of the effect on growth of projected tax cuts is subject to a wide confidence band.

While stronger U.S. growth as a result of the tax reform would have a positive effect on Canadian growth, the contemplated cut in the maximum U.S. corporate tax rate from 35 percent to 20 percent could lead to some increased incentive to invest in the United States rather than in Canada, with negative effects on potential Canadian growth. Likewise, the U.S. proposals imply a small widening of the substantial Canada-U.S. gap in personal income tax rates for upper-middle and upper incomes. These small changes would reduce Canada's attractiveness to highly skilled professionals and entrepreneurs. This would not be favourable to Canadian growth down the road. However, in our base-case projection for Canada we do not attempt to quantify the impact of changes in the structure of the U.S. tax system on growth of Canadian GDP. We do, however, take account of the small impact on Canadian growth of somewhat stronger projected U.S. growth.

NAFTA Negotiations

Our base-case projection assumes that negotiations to renew NAFTA drag on to mid-2019. We assume that in the end some sort of arrangement between the parties to NAFTA would emerge which would enable a continuation of significant volumes of mutually advantageous North American trade (see Section IV). Meanwhile the "old" NAFTA would continue to operate, but in a climate of uncertainty about the outcome of the negotiations. In our projections we assume that this uncertainty will moderate business fixed investment somewhat, especially in Canada and Mexico, and consequently result in slightly slower real GDP growth than would be the case if NAFTA was not subject to renegotiation.

It may well happen, however, that the United States will actually withdraw from NAFTA some time in 2018, once the inevitable court challenges to a notification of intended withdrawal by the United States will have run their course. Several alternative trade arrangements would exist for Canada in that eventuality (see Section IV), with varying impacts across industries and firms. The size of the macroeconomic cost of such arrangements in terms of reduced trade, investment and output relative to our base-case projection are hard to evaluate but could be quite significant in the short term. This being said, the negative shock relative to our base-case projection would likely lead to a moderation in the pace of monetary policy normalization and to a depreciation of the Canadian dollar, both of which would support aggregate demand and partially offset the direct negative impact of NAFTA abrogation.

Monetary Policy Normalization

In the base-case scenario, monetary policy becomes gradually less accommodative as data validate central bank expectations that inflation would rise in response to pressures of demand on capacity. The cautiousness of central banks in raising rates reflects their prime concern about downside risks to growth and inflation, uncertainty about the level of the neutral rate, as well as concerns that increases in policy rates relative to other countries trigger a significant exchange rate appreciation which could unduly cut growth and keep inflation below target (see Section IV). "Data dependency" on the part of central banks implies that the pace and extent of policy rate increases going forward are uncertain and therefore may deviate significantly from our base-case projection in the short run. While we do not project a precise quarterly path of policy rate increases, if our base-case forecast of growth in Canada and the United States in 2018–2019 is met or exceeded we do expect that both central banks will have to raise rates by the end of 2019 to the lower half of the estimated 2.5 to 3.5 percent range of the neutral rate.

China's Growth Strategy

We had previously projected a marked slowdown of growth in China in 2018–2019 to significantly below the official target on the assumption that authorities would manage policy so as to facilitate rebalancing of the economy and, more importantly, to contain the risk of a sharp financial correction. However, it became evident in the last year that notwithstanding further build-up in financial vulnerabilities, the government was willing to expand credit and investment enough to meet its growth target. The recent 19th Communist Party Congress heralded a change in the importance attached to meeting the growth target. It downplayed existing growth targets to 2020 and failed to set future targets. It stressed "quality instead of speed" (see Section VI). Nevertheless it is clear that authorities will still not permit growth to decelerate very much in the short term.

In our base-case projection, Chinese authorities are projected to maintain a sufficiently expansionary mix of monetary and fiscal policies to support growth of close to 6.5 percent yearly to 2019. Even with some greater emphasis on quality, such a pace of growth runs the risk of exacerbating financial vulnerabilities. China's central bank governor, soon to depart from his job, has recently taken the unusual step of publicly warning of the risks of excessive debt and speculative investment, which could lead to a sharp correction in asset prices. However, we do not expect that in the short-term policies will sharply restrain credit growth in order to preserve financial stability nor do we foresee a sharp correction in asset prices over the next two years.

SECTION III: INTEREST RATES, RADICAL UNCERTAINTY AND CENTRAL BANK POLICY

In making business plans, firms must make some assumptions not only about the future of demand for their products but also, very importantly, about the future path of interest rates and the ease (or difficulty) of access to credit. The future path of interest rates over the medium and longer term will of course depend on underlying forces determining saving and investment. But in the short run, certainly over the next one to two years, interest rates will be largely determined by the policies of central banks. And recently, central banks—in particular the Federal Reserve and the Bank of Canada—have been less than completely helpful in indicating where their policy interest rates are headed. In the face of radical uncertainty, both central banks have said that their future decisions will be "data dependent" and declined to give much by way of forward guidance.

The purpose of this section of the outlook is to explain what central banks mean by "data dependence", and to describe the difficulties and uncertainties that central banks face in assessing the future path of aggregate demand and hence inflation. Both the chair of the Federal Reserve and the Governor of the Bank of Canada have tried to lay out what they mean by "data dependence" in recent speeches.5 6 In these speeches and in the Bank of Canada's most recent Monetary Policy Report (October 25), the central banks explain how they are interpreting the current conjuncture of tight labour markets (low unemployment) and well-below target inflation as they set interest rate policy to achieve their target of 2 percent inflation.

While there are technical differences between the approaches of the two central banks, both tackle the problem in roughly the same way. Both start with models that provide forecast estimates of future inflation based on measures of the balance between underlying aggregate demand and supply in the economy. In estimating supply capacity both banks put heavy emphasis on measures of labour market slack (or tightness). They both base projections of demand on measures of investment and consumer intentions, inflation expectations, the outlook for exchange rates and the growth of foreign demand. Both banks put little emphasis on volatile elements (energy and food prices) in assessing the outlook for future inflation.

When their models indicate that excess demand is likely to drive future inflation above target, the basic objective is to reduce monetary accommodation by raising the policy interest rate, and vice versa when models indicate the likelihood of future excess supply. When models indicate a rough balance in aggregate supply and demand and inflation very close to the 2 percent target, both banks currently estimate that a "neutral" policy rate would be 2.5 to 3.5 percent—a rate at which monetary policy would properly accommodate GDP growth at its "potential" rate.

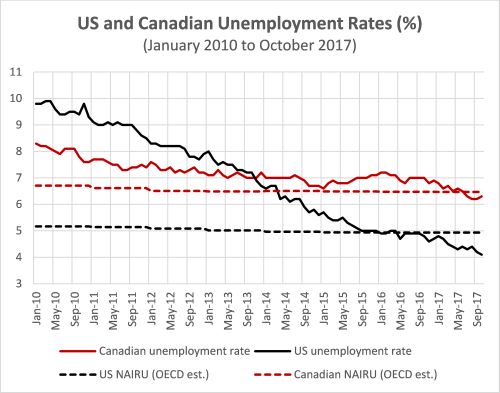

In the United States, the main but by no means the only indicator of excess supply or slack in the economy used by the Federal Reserve is the unemployment rate.7 This measure currently indicates that future inflation is likely to rise as both the current and forecast future unemployment rates are at or below estimates of the NAIRU—the non-accelerating inflation rate of unemployment (see Chart 1).

In Canada, the Bank's preferred measure of slack—the output gap—reflects aspects of the labour and product markets that are broader than overall unemployment. The Bank projects in its October Monetary Policy Report that excess supply measured by the output gap is completely eliminated by the first quarter of 2018. If both Canadian and U.S. central banks were to believe their judgment that there is little or no slack currently and if both were confident of their published base-case forecasts of future growth and slack, then they both should be planning to raise their policy rate at a measured pace from the current 1 or 1.25 percent to at least 2.5 percent (the lower end of their estimated neutral rate) by the end of 2019. Given the current term structure of interest rates, this would imply a 3.25 to 4 percent rate on 10-year government bonds.8 Moreover, given the uncertainty that central banks entertain about the response of their highly leveraged economy to higher interest rates, and hence uncertainty about where the neutral rate level will be, we would expect that they proceed cautiously as their policy rate gets close to the 2.5 percent lower bound of the neutral rate range.

Meanwhile neither of the central banks are indicating that they intend to raise rates at the speed that would be appropriate to avoid the risk of inflation above target in 2019, account taken of the lags in the response of inflation to interest rate changes. In fact, both have been at pains to stress that they will move cautiously depending on the economic outlook as informed by incoming data. Why are both central banks being so cautious? Why are they willing to take the chance of being "behind the curve" with respect to future inflation and what does this mean for financial markets as we near the end of the decade?

First, both central banks imply or explicitly say that the risks to their forecast of economic growth are weighted to the downside. While the Bank of Canada forecasts growth of 2.1 percent in 2018 and 1.5 percent (potential) in 2019, the risks the Bank lists in the October Monetary Policy Report are weighted to the downside. In particular, the Bank elaborates on the risk to exports of a shift toward protectionist trade policies and the downside risk to consumption and housing from a pronounced drop in houses prices. These downside risks appear to the Bank to be greater than the upside risks of stronger U.S. GDP growth and improved consumer sentiment in Canada.

Second, both central banks express worry that the measures of labour slack in their models understate the excess supply of labour. They think that labour force participation and average hours worked could increase more than projected so that wage rate growth and increases in unit labour costs could be less than projected. As Governor Poloz said in his November 7 speech:

"Even though Canada's unemployment rate has returned to 2007 lows, other indicators suggest a fair amount of slack remains."

Third, they both concede that changes in the structure of product markets (greater competition, e-commence) and new technologies may constrain price inflation more than previously estimated, although they find little direct evidence that this is a materially important constraint. Central Banks and ministries of Finance always face "radical uncertainty"9 in understanding how the changing structure of the market economy is likely to impact future behavior of wages, prices and inflation. Just as central banks and government analysts did not understand the structural shifts in the 1970s, shifts which changed the relationship between measured slack in the labour market and wage and price inflation, so today analysts may be misjudging the impact that structural shifts are having on wage and price behavior with the result that, perhaps, the economy can run hotter without generating wage and price inflation.

Fourth, both central banks worry that if they raise their policy rate faster than other central banks raise their rates, the exchange rate will rise reducing net exports and aggregate demand.10 Both central banks have a "first mover" problem which makes them cautious about raising interest rates.

Finally, while both central banks recognize that excessively low interest rates may be causing excessive risk taking and over-leverage by households, non-financial firms and non-bank financial firms, they place less weight on this risk than on other risks. This excessive leverage buildup, just as during the 2004–2007 period, risks creating a financial crisis and sharp correction in asset prices. The Bank of Canada acknowledges this risk but argues that it is the job of macroprudential policy, not monetary policy, to deal with it. This being said, the Bank does not dismiss the risk that the buildup in leverage makes the economy more sensitive to future increases in interest rates. This enhanced sensitivity would create the risk that a policy rate escalation to the upper part of the "neutral rate" range of 2.5 to 3.5 percent would lead to a greater contraction of demand than warranted at that stage of the business cycle. The likelihood of a greater sensitivity of the economy to interest rate increases therefore is likely to induce the Bank to be very cautious as its policy rate gets close to 2.5 percent.

It is important to note that a limited rise in policy rates would leave monetary authorities with relatively little rate-cutting room to counteract the next recession, implying that they may have to rely relatively heavily on quantitative easing and other unconventional tools to stimulate the economy in that event.

For all these reasons (and abstracting from possible geopolitical crises) we think it is prudent to expect that both central banks will exercise their judgement and raise their policy rate only gradually in the near term, less rapidly than their base-case economic outlook as well as financial stability concerns may warrant. To quote the latest statement from the Federal Reserve:

"The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data."11

As stated by Bank of Canada Senior Deputy Governor:

"During periods of uncertainty like today, a cautious approach may be prudent."12

It is also prudent to plan that both central banks will limit their total policy rate increase over the next two years to the bottom half of the current 2.5 to 3.5 percent range for the neutral rate.

Based on this discussion we describe for 2018–2019 our base-case interest rate planning scenario for business in Section VI.

SECTION IV: TRADE NEGOTIATIONS

The renegotiation of the NAFTA is by far and away the largest current trade policy issue for Canada. There are good reasons to be seeking a modernization of the NAFTA as it approaches its 25th anniversary. But, unfortunately the key interest of the Trump administration seems to be in moving away from trade agreements which they believe fetter the use of American power in their dealings with other nations. The fact that NAFTA has been very beneficial to the United States and is strongly supported by business, most elected officials at the state level and by the leadership of the Republican majority in Congress seems to cut little weight with the president and his Trade Representative—so far at least.

This section considers the prospects for the NAFTA negotiations, the likelihood of a decision by the president to withdraw from NAFTA, what that could mean for Canada, and what Canada might do at the different points in this unfolding scenario. There are serious disagreements inside the United States about what should be the trade negotiating objectives of the administration. This makes it more difficult to assess how events will unfold. It is probable, however, that events inside the United States will have a much larger impact on the negotiations than anything that Canada or Mexico might do at the negotiating table. It follows, therefore, that both Canada and Mexico should remain in close touch with various American domestic interests with a stake in NAFTA.

Prospects for the NAFTA Negotiations

There are really two NAFTA negotiations going on: a modernization update negotiation which is going very well and a very important renegotiation that is going very badly. The modernization negotiation is introducing NAFTA to the digital age and e-commerce, borrowing significantly from provisions in the TPP that were largely inspired by American negotiators. Good progress has been made and chapters are emerging that would be of benefit in the eyes of all three NAFTA partners.

The more important negotiation, however, is a renegotiation in which the administration seems determined to move away from a rules-based agreement that provides an opportunity to compete throughout the North American marketplace to one ostensibly predicated on achieving certain results, notably a perceived positive balance of trade for the United States particularly in manufactured products. A key objective for the Trump administration is to discourage investment in Mexico and Canada and to encourage it in the United States. This is what seems to be driving American proposals that would:

- require the agreement to sunset after five years unless the parties decided to renew it;

- weaken all the NAFTA dispute settlement systems to ensure they have no binding effect on the United States thereby rendering them virtually meaningless;

- effect changes to the rules of origin in the automobile sector that would require 50 percent U.S. content in any vehicle being imported into the United States as well as requiring 85 percent North American content. Both proposals are unacceptable to Canada and Mexico, all the vehicle producers, the auto parts manufacturers, and the unions;

- totally eliminate Canada's agricultural supply management programs while making no concessions in protectionist U.S. programs such as sugar and dairy; and

- render the NAFTA government procurement disciplines worthless by lowering potential Canadian access to U.S. government contracts to a level well-below what is open to Canadian suppliers under the World Trade Organization (WTO) procurement agreement.

It is difficult to judge whether these proposals are tactical or whether they are ultimately essential requirements if the Trump administration is going to continue United States involvement in NAFTA. Given President Trump's longstanding distaste for NAFTA and Trade Representative Robert Lighthizer's enthusiasm for pushing a winner-take-all approach at the negotiating table, Canadian business should be prepared for the United States to withdraw from NAFTA.

The bright spot is that the American business community has finally begun to speak in defense of NAFTA. They have grasped, albeit rather late in the game, that the current American approach to the NAFTA negotiations presents an existential threat to the agreement and to the vast commerce that has developed over the last quarter century. Business, led by the major associations including the U.S. Chamber of Commerce, has begun to blitz members of both houses of Congress. There are signs of increasing concern on Capitol Hill about the administration's approach. Business has also begun to gear up a communications campaign designed to explain the value of NAFTA to the public (and to their own employees).

The only significant positive development to emerge from the October negotiating round in Washington was agreement to slow down the pace of meetings and extend the time frame for the negotiations through the first quarter of 2018. This development provides time for the business forces favouring NAFTA to gain strength in the United States and to make their influence felt on public opinion and the administration. The objective of the business coalition is to bring sufficient pressure to bear to force the administration to recalibrate its positions at the negotiating table. Whether they will be able to do that is unknown, but extending the time frame of the negotiations will provide businesses the opportunity to make their case and to rally support in Congress and among senior political figures at the state level.

A key problem facing Canadian and Mexican negotiators is whether anyone on the American side has both the authority to put a deal together and the interest in doing so. The president is not interested in details and Robert Lighthizer, the United States Trade Representative, appears to be a true believer in everything he has put on the negotiating table. No one below Mr. Lighthizer has the authority to cut a deal. It is not clear whether anything can be done in the near term to get around this problem.

It is worth considering what the Canadian government should do at this juncture. In our view, the course is clear. Canada should remain constructively engaged at the negotiating table but hold firm in not accepting American proposals that would undermine the benefits of NAFTA for Canada. We should urge the Mexicans to adopt a similar approach. Canada should keep the negotiations going by "ragging the puck". Of course, uncertainty will continue under this approach, but it offers the best hope of a favourable outcome.

If the negotiations are going to fail, Canadian governments and business should make sure that the blame is not put on Canada. It would be important to be able to make the case with our allies in the United States that Canada was not the cause of the inevitable economic dislocation. It is important to bear in mind that the status quo, the existing NAFTA, is satisfactory for Canada and Mexico. It is the United States that is the demandeur for change. If anyone is going to leave NAFTA let it be the United States. If the Americans withdrew, NAFTA would remain in force between Canada and Mexico, thereby continuing to provide Canada free access to a large emerging market that is already one of our top five trading partners. Furthermore, it would mean that the NAFTA framework would remain intact, which would make it easier for a subsequent administration in the United States to come back to NAFTA.

Possible American Withdrawal From NAFTA

Most observers consider that the president does have sufficient executive authority to be able to withdraw from NAFTA without the assent of Congress. However, almost all observers think there would be a court challenge if the president were to give the six-month notice of his intention to withdraw from the agreement. The court case would probably be initiated by the business community. These developments might also cause Congress to react. There is some ambiguity under the Constitution with Congress responsible for foreign commerce and the president having power to make treaties. But it is clear that Congress, with sufficient will, could act in the trade space and could take back authorities it has delegated to the president. In this regard, comments by Senator Roberts, chair of the Senate Agriculture Committee, are significant, namely that he did not rule out the possibility of Congress legislating to protect NAFTA, while making it clear that such action would be premature at this stage.

Any scenario in which the president were to announce his intention to withdraw would usher in a period of great uncertainty.

In the event of withdrawal, it is unclear what actual trade regime the United States would apply to Canada and Mexico since that regime is provided for in domestic law rather than under the provisions of NAFTA. However, once the United States left NAFTA, the WTO rules that allow countries that belong in a free trade association to discriminate in favour of each other would no longer be applicable. This means that the United States would no longer be able to discriminate in favour of Canada and Mexico, and vice versa. Canada and Mexico would still have free trade relationships with each other and with other countries, as would the United States, at least in the short term. Gradually the United States would move to a least-favoured-nation-situation in which American exporters would in effect be discriminated against in Canada and Mexico and in many other major markets e.g., the EU and Korea and potentially the Trans-Pacific Partnership (TPP) region. The same would apply to Canadian and Mexican exports to the United States.

What Would This Mean for Canada and How Might Canada Respond

The withdrawal of the United States would have a dramatic effect on the landscape of Canada's international trade relationships. Canada's trade relationship with the United States would be governed by the WTO rules (and bound tariff rates) unless, of course, the Canada-US Free Trade Agreement (FTA) were to come back into force. It is important for business and both federal and provincial governments to analyze what the practical effect of these two scenarios would be. This analysis would need to take account of the fact that the General Agreement on Tariffs and Trade Uruguay Round was completed after the NAFTA came into force so that U.S. most-favoured-nation (MFN) duties would be lower than they were at the time the FTA and the NAFTA were negotiated. In addition, as noted recently by Foreign Minister Freeland, some 40 percent of current Canadian exports to the United States rely on the WTO provisions rather than NAFTA provisions to secure the most favourable entry to that market.

It would be essential in considering plan B outcomes to have a detailed understanding (industry by industry) of how FTA treatment might differ from WTO treatment and most importantly whether there are situations where FTA treatment would in effect be WTO minus.

Another area to consider is processed food products where reimposition of MFN duties on American imports could well induce firms to reestablish branch plants in Canada.

The situation in automobiles provides an interesting case study. Let us look in particular at passenger vehicles. Under NAFTA, the rate of duty is zero provided the rules of origin threshold of 62.5 percent is reached. Under the WTO the rates of duty would be 2.5 percent into the United States and 6.1 percent into Canada. A 16% rate (MFN applied rate) would apply into Mexico but with a WTO bound rate of 50 percent, implying that the Mexicans could legally under WTO increase the applied duty to that level. This would mean Mexico would be required to impose duties of at least 16 percent on American automobile imports and could legally impose duties of 100 percent on all non-preferential suppliers, e.g., the United States and China. Mexico could lower the 16% rate but would have to do so for all WTO members with whom they do not have free trade agreements. A key point here is they would be required to apply the same duties to China and the United States. Furthermore under WTO rules any sort of rule of origin requiring North American content would be prohibited. Canada and Mexico would still have duty free trade with each other and with other FTA partners like the EU This scenario would clearly weaken the prospects for automobile production in the United States. It is hard to see how President Trump would be able to sell this successfully as a win for the U.S. industry.

Conclusion

The negotiations to renew NAFTA are likely to drag on, probably into 2019. In the end, they should result in a new agreement between the parties to NAFTA, but one that would not include the egregious American proposals that are now on the table. This scenario could well include an American notification of their intention to withdraw from NAFTA that would never be executed.

The main alternative scenarios that need to be looked at in the event of U.S. withdrawal are:

- keep the NAFTA in effect between Canada and Mexico but go to WTO treatment for trade with the United States. It would be hoped that a future American administration would rejoin NAFTA; and

- try to bring the suspended Canada-U.S. FTA back into force, but keep the NAFTA in effect between Canada and Mexico. If the price for bringing the FTA back were making new concessions to the Americans, it might complicate subsequently returning to NAFTA as the agreement governing Canada-U.S. trade.

The most important factor to consider in analyzing the practical effect of the different scenarios would be the effect on investment. Clearly a deterioration in the terms of Canadian access to the U.S. market would have negative effects on investment in Canada. However, in certain cases higher Canadian duties might well induce U.S. firms to invest in Canada to avoid the duty. The nature of such investment might be conditioned by the prospects of exporting to the EU under the duty free provisions of CETA as well as exporting back to the United States even after paying the relatively low U.S. MFN tariffs.

Opportunities with Other Countries

We would urge the government to continue to negotiate trade liberalizing agreements with other countries. Although other markets will never replace the central importance of the U.S. market for Canada, any serious efforts at diversification will help. Also, new agreements will further emphasize the growing least-favoured-nation status of the United States and increase pressure on the American government to return to an open, rules-based trade agreements policy.

The best news on the trade agenda lately is that Ministers from the 11 countries (minus the United States) that originally signed the TPP agreed in Vietnam on the core elements of a slightly revised TPP—now called the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). A few months ago, after President Trump had announced the United States' withdrawal from the TPP, very few observers gave the TPP a chance at survival. With some further effort by the participants, this agreement now seems likely to come into force. While a number of countries have been supportive of this effort, it is Japanese leadership that proved decisive.

For Canada the CPTPP offers the prospect of reaching the long-time goal of free trade access to Japan and other promising markets in the region. It also shows that our efforts at trade diversification are bearing fruit. It should increase domestic pressure on the Trump White House to modify somewhat its approach to trade. Significantly it establishes a high quality trade agreement in the Asia-Pacific region, which will serve as a useful model as countries engage China in trade negotiations. This may prove to be particularly useful to Canada if the government decides to move ahead with FTA negotiations with China.

The Canadian governments should put the necessary resources into ensuring the successful final conclusion of the negotiations and push to bring the agreement into force as soon as possible.

SECTION V: CHINA AFTER THE CONGRESS

At the 19th Congress of the Chinese Communist Party, President Xi outlined a vision for economic progress in China, a vision which places less emphasis on the highest possible economic growth rate as the singular objective of policy and greater emphasis on economic transformation and the quality and sustainability of economic development. Policy will be driven by "Quality instead of Speed". What precisely this means remains to be seen, but in his speech to the Congress, President Xi described six elements of a "modernized economy": 1) further supply-side structural reform; 2) promotion of innovation; 3) rural vitalization; 4) coordinated regional development domestically; 5) flourishing of the socialist market economy; and 6) new ground for opening up.

The key implications are: 1) the quality of economic development outweighs growth rate; 2) financial stability is part of national security; and, 3) the goal is to completely eliminate poverty. Xi's road map for progress includes: moderately prosperous society by 2020; modernized socialism by 2035; a prosperous, democratic, civilized, harmonious and beautiful modern powerful socialist China by 2050.

While this strategy for a "modernized economy" has significant implications for both the structure of the economy and rate of GDP growth in the 2020s, the implications for growth and credit creation over the remainder of this decade are much smaller. Growth of GDP in 2018–2019 is likely to continue at 6.5 percent and credit growth will still be managed to meet this target. There will be adequate credit for housing to facilitate growth in urban areas and prevent rent spikes in first and second tier cities but not enough to trigger a renewed boom in house prices nationwide and over-building in third and fourth tier cities.

The emphasis on the "modernized economy" implies relatively less support for investment in traditional heavy industries and more emphasis on higher-technology, less energy-intensive production. Nevertheless in the short run, investment in heavy industry (especially in the northeast) is likely to continue in order to maintain employment, to modernize plant and equipment, and to reduce pollution. At the same time, greater emphasis will be placed on facilitating investment in the service industries, especially mobile internet, online banking, online education, domestic tourism, logistics services and cross-border retail. The government will also put greater emphasis on the development of new complex online financial services. All financial technology services will continue to be tightly controlled.

The outcome of the Congress for monetary policy is that there is likely to be little change in the near term. Even though China central bank (PBoC) has not changed its benchmark one-year deposit and lending interest rates since October 2015, many in China suggest that PBoC does not need to raise the benchmark rates as some western analysts had predicted. This is because PBoC's micro-management of the money market rates along with tighter credit control have already started generating the desired effects. Chinese authorities will likely adopt a series of micro adjustments over time in order to achieve the seemingly conflicting goals of deleveraging while at the same time maintaining high growth. The recent announcement of their intention to permit foreign investment banks and insurers access to China is a clear indication of their desire to improve the efficiency of the domestic market. Authorities will also want to keep the ability to re-adjust without appearing to have policy shifts causing panic or confusion. Despite the unusually candid and public urging of the outgoing governor of PBoC, Zhou Xiaochuan, it is unlikely that China will allow a flexible RMB exchange rate and free flows of capital across the border.

It is likely that the central government will try to "internalize" the debt overhang without bankrupting a large number of State-Owned Enterprises (SOE), local governments, and even some large private corporations. This is consistent with the central government's insistence on the maintenance of financial stability. On November 8, the State Council launched a new agency named Financial Stability and Development Committee (FSDC). It is headed by Vice Premier Ma Kai. FSDC outranks PBoC and the existing regulators (CBRC, CSRC, and CIRC). It will supervise the financial regulators, review key plans and policies, and ultimately be responsible for managing systemic financial risks for China.

Fiscal policy is likely to continue to be expansionary over the next few years as the central government will probably allow the deficit/GDP ratio to continue to rise beyond the current level of 3 percent in order to facilitate structural transformation and maintain employment growth. Nevertheless, the central government will continue to crack down on off-balance-sheet financing by local governments. The central government will also likely assume responsibility for some local government debt (using local taxes as collateral). At the same time, the central government will force the restructuring of some zombie SOEs, assuming some of their debt obligations on government account in order to preserve the stability of bond markets. In the context of a tightly controlled economy, we believe that increased central government deficits and the rise in the debt/GDP ratio should be appropriately supportive of both growth and structural transformation in the short and medium run.

For both domestic transformation and geopolitical reasons, the central government will continue to provide continued budgetary support for the "Belt and Road Initiative."

The Belt and Road Initiative is a collection of regional economic corridors, e.g., China-Pakistan, Bangladesh-China-India-Burma, China-Mongolia-Russia, Eurasia etc. Through infrastructure projects beyond China's borders, this initiative has facilitated the absorption of some of China's industrial overcapacity to supply infrastructure. The initiative's vision of creating several regional economic corridors, if successful, could also significantly ease China's logistic burden in acquiring much needed energy and raw materials. Geopolitically, the Belt and Road Initiative is likely to be used by China to demonstrate an alternative approach to distribute the benefits of increased global trade and cross-border manufacturing chains. China is becoming increasingly confident in playing the role of world leader and in exporting the "China Model" (a combination of strict political control, rapid economic growth and innovation) globally. It hopes to fill the void created by the inward-looking and protectionist stances of many countries. The recent Congress incorporated the Belt and Road Initiative into the Chinese Communist Party's newly amended constitution.

In sum, the policies emerging from the 19th Congress are likely to have only a small impact on aggregate Chinese economic growth in the short run. Growth is likely to continue at close to 6.5 percent for the next two years and the investment share of GDP is likely to change only slowly. Nevertheless the Congress signaled significant "Reform and Opening Up" over the medium term, implying a shift from emphasis on investment and trade to emphasis on consumption, services, and more equitable distribution of income, a shift which implies considerably lower growth rates in the 2020s.

During the first press conference after the Congress, President Xi assured the international press that China would continue to reform and open up. However, he described "Reform and Opening Up" as "one important tactic". The Chinese wording is a noticeable downgrade from its conventional characterization as the fundamental principle of state governance. Now it is a means to an end. Psychologically, "reform" no longer simply means the learning and adaptation of western systems—as long as the party is capable of continuous evolution, this qualifies as reform. "Opening Up" increasingly implies a bidirectional relationship in which China expects to lead the world in the development and sale of advanced technologies and not just acquire these technologies from developed economies.

SECTION VI: SOME PLANNING PARAMETERS FOR CANADIAN BUSINESSES

The future is uncertain, yet Canadian businesses must make decisions to best position themselves for it. In this final section, based on the previous analysis and additional considerations, we spell out some of the planning assumptions that seem the most critical for Canadian business.

We think that it is appropriate for business to plan on the base-case assumption that global, synchronized growth will remain solid at around 3.5 percent to the end of this decade. While there are downside risks, especially related to financial vulnerabilities, the odds for a downturn or a major slowdown in growth in the short term appear to be low, although they build somewhat as the decade comes to an end.

Growth in Canada will slow from the unsustainably rapid pace experienced in the four quarters to mid-2017 (nearly 4 percent) to more sustainable rates. This being said, as the economy will be operating at or close to capacity, it will be difficult for business in general to meet the need for increased production going forward without investing in plant, equipment, or technology. Moreover, businesses should expect to face labour market pressures for stronger wage rate growth. The risk of rising unit labour costs will increase if firms do not invest enough to raise labour productivity growth.

In all likelihood it will take time before a revised NAFTA or a new alternative trade arrangement with the United States is put in place and operational. Whatever the new arrangement, it may well be less advantageous to Canada, especially in some industries. Nevertheless it is best for most businesses to expect that the new arrangement will still enable a high volume of profitable Canadian exports provided that competitive prices and quality are maintained on domestically-produced products and services. Remaining price competitive in U.S. dollar terms would be facilitated by a depreciation of the Canadian dollar if the new arrangement was expected to be materially disadvantageous to Canada relative to NAFTA.

We think that it is reasonable for businesses to base their financing plans on the assumption that each of the Federal Reserve and the Bank of Canada will raise their policy rate targets by three quarters of a percentage point by the end of 2018. It would also be prudent to assume that both banks will judge it appropriate to raise policy rates to 2.5 to 3 percent by the end of 2019, recognizing that there is some downside risk to this planning assumption.

Business should prudently base their financing plans on the assumption that 10-year government bond rates in both countries will be in the range of 3.25 to 4 percent by late 2019, and that risk spreads will have widened somewhat. In other words, business should plan on the basis that their borrowing rates will be almost two percentage points higher two years hence. This is the same prudence that Office of the Superintendent of Financial Institutions is requiring household borrowers to exercise in order to qualify for mortgage loans at rates substantially higher than current rates. At the same time, we would judge it appropriate to plan on the basis of an exchange rate moving in a fairly wide band centered on 80 U.S. cents and a WTI oil price not consistently exceeding US$60 until the end of the decade.

On the structural side, it is hard to judge for now how large might be the impact on Canadian business of new large investment projects, either public infrastructure or pipelines, in the next several years. It is quite possible that at least one of the major projects now started or under construction (Keystone XL, Kinder Morgan, Site C, Muskrat Falls) will not proceed and that no new major federally financed infrastructure project will be well underway by the end of 2019. While detailed plans for federal assistance for additional provincial or municipal infrastructure projects are yet to be announced, the aggregate federal assistance through Integrated Bilateral Agreements will be in the order of $30 billion over a decade and likely will be back-end loaded. This is not a large increase from what the Harper government was considering. It is uncertain how quickly the Canada Infrastructure Bank will be able to initiate projects, especially since governments at all levels have demonstrated extreme reluctance to support projects which require user charges or tolls. Thus on balance, business should plan on very little new additional public investment in infrastructure in 2018 and much of 2019.

Here is a table of key parameters for 2017–2019.

Key Planning Parameters for 2017–2019

|

2017 |

2018 | 2019 | |

| U.S. GDP Growth

(%) |

2.2 | 2.3 | 2.0 |

| Canadian Growth (%) |

|||

| Real GDP | 3.1 |

2.1 | 1.6 |

| Household Consumption | 3.5 | 2.2 | 1.8 |

| Business

Non-Res. Investment |

1.9 | 3.8 | 2.9 |

| Interest Rates (Year-End) (%) | |||

| BOC Target Overnight Rate | 1.0 | 1.75 | 2.5-3.0 |

| 10-Year GOC | 2.1 | 2.75–3.0 | 3.25–3.75 |

| 10-Year U.S. Treasuries | 2.4 | 3.0 | 3.50–4.0 |

| U.S. Fed Funds Rate | 1.5 | 2–2.25 | 2.5–3.0 |

| Exchange Rate US$/C$ (Year-End) | 0.79 | 0.8 | 0.82 |

| WTI Oil Price (US$/bbl) | 51 | 55 | 60 |

Footnotes

1. The neutral rate, which is unobservable but is estimated to vary over time, is that level of the Federal Funds rate that keeps the economy in balance and inflation on target.

2. The existing inflation-control target of 1 to 3 percent centered on 2 percent was renewed at the end of December 2016 for a 5-year period to the end of December 2021.

3. "Bank of Canada maintains overnight rate target at 1 percent", Bank of Canada press release, October 25, 2017."

4. Based on the lower range of estimated multipliers for tax cuts reported by the U.S. Congressional Budget Office (Working Paper 2015-02).

5. Janet Yellen, "Inflation Uncertainty and Monetary Policy", Cleveland, September 26, 2017.

6. Stephen Poloz, "The Meaning of Data Dependence", St. John's, September 27, 2017, and "Understanding Inflation", Montreal, November 7, 2017.

7. The Federal Reserve actually employs both narrow and broader measures of unemployment.

8. In the United States, the future term structure will also depend on the speed at which the Federal Reserve reduces its balance sheet. They have committed to a slow, measured reduction.

9. The concept of "radical uncertainty" was developed by Mervyn King in his book The End of Alchemy, 2016. Radical uncertainty implies that there are not only unknown or non-estimable knowns, but also unknown unknowns.

10. The Federal Reserve worries about getting too far ahead of increases by the ECB and Asian central banks. The Bank of Canada is worried about getting out ahead of increases by the Federal Reserve.

11. The appointment of Jerome Powell as chairman next February is not likely to change the approach of the Federal Open Market Committee in the short run. It should be noted that there are likely to be four new appointments to the board over the next year and a new president of the Federal Reserve Bank of New York. These could lead to a more significant change in approach after 2018.

12. Carolyn Wilkins: "Embracing Uncertainty in the Context of Monetary Policy", speech in New York, November 15.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.