- within Compliance and Family and Matrimonial topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Banking & Credit, Healthcare and Law Firm industries

Replay the Economic Outlook seminar presented at the Bennett Jones office on November 29.

This Fall Outlook has four sections. The first section describes the main aspects of the "new normal" of low growth that has prevailed for advanced economies in the last six years of economic recovery. The second section discusses key factors that have shaped the economic performance of advanced economies and are likely to condition growth in aggregate demand and potential output over the next several years. With this analysis in background, the third section briefly explains our short term outlook for the global economy and Canada to 2018, showing that for the advanced economy it remains well on the low-growth path of the "new normal". Finally, a fourth section draws implications of the "new normal" for the conduct of economic policies in advanced economies and the strategy businesses should follow.

Section I: The New Normal – Low Growth: 2011-2016

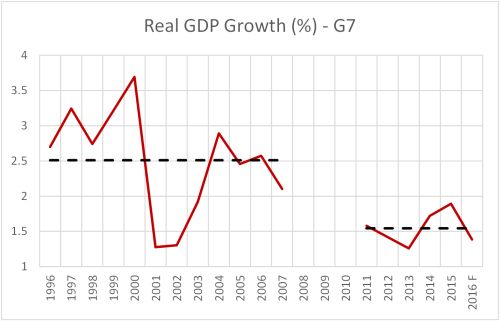

The world as a whole, and notably the advanced economies (AE), have experienced subdued growth after 2010, much below the trends experienced before the 2008 crisis (Chart 1.1). There seems to have been a structural break, which the usually protracted effects of debt reduction which follow a financial crisis can explain only in part.

Chart 1.1:

Source: IMF, World Economic Outlook, October 2016 database.

This low growth for advanced economies reflects both inadequate demand growth and a decline in potential output growth. It was accompanied by subdued core inflation and persistently low actual and expected interest rates.

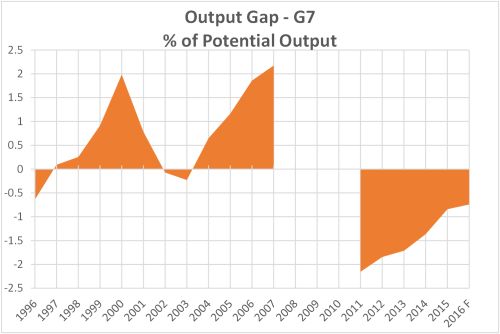

Inadequate demand growth showed up in a considerable, persistent shortfall of actual aggregate demand relative to potential output (Chart 1.2).

Chart 1.2:

Source: IMF, World Economic Outlook, October 2016 database.

Demand in advanced economies was held back by several factors, whose relative importance varies from country to country. In both Canada and the United States the lower growth in aggregate demand over 2011-2015 relative to 1996-2007 primarily comes from household consumption, then from government consumption and investment, and then from nonresidential fixed business investment.

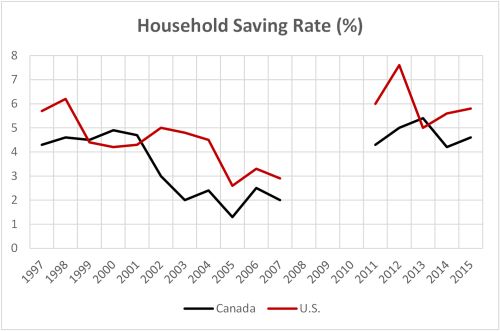

Households adjusted to the recession by sharply raising their saving rate and subsequently keeping them at these higher levels in order to reduce their debt and as a precaution in the face of uncertainty (Chart 1.3).

Chart 1.3:

Sources: Statistics Canada Cansim 380-0072 and U.S. Bureau of Economic Analysis.

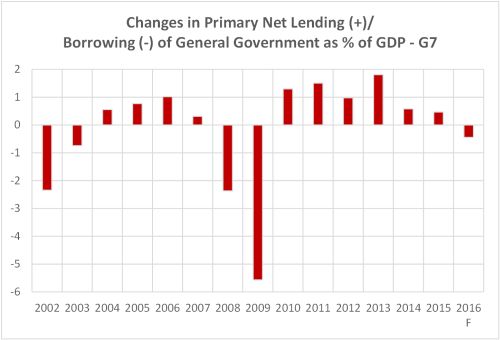

Governments also increased their saving rate as fiscal consolidation followed a major stimulus in 2008-2009 and resulted in a drag on growth until 2015 (Chart 1.4).

Chart 1.4:

Source: IMF, World Economic Outlook, October 2016 database.

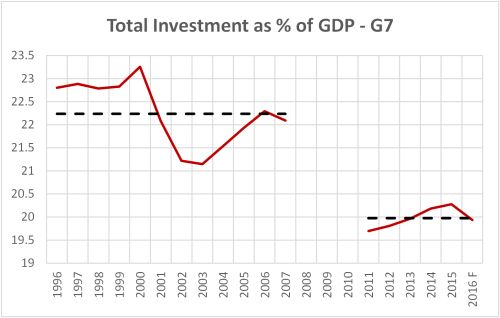

Inadequate demand also reflects a lower investment rate due to several factors, including weaker growth and pessimistic outlook regarding future demand, housing market correction in a number of countries, and a collapse of capital spending in the oil and gas sector starting in 2015. (Chart 1.5).

Chart 1.5:

Source: IMF, World Economic Outlook, October 2016 database.

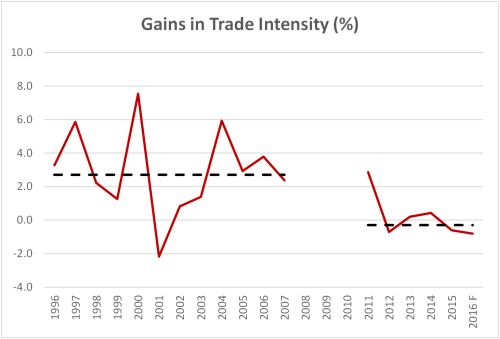

A lower contribution of real nonresidential business fixed investment to real GDP growth not only slowed productivity growth but also contributed to depress gains in international trade intensity1 as the machinery and equipment component of investment has a particularly high import content (Chart 1.6).

Chart 1.6:

Source: IMF, World Economic Outlook, October 2016 database. Calculations by the authors.

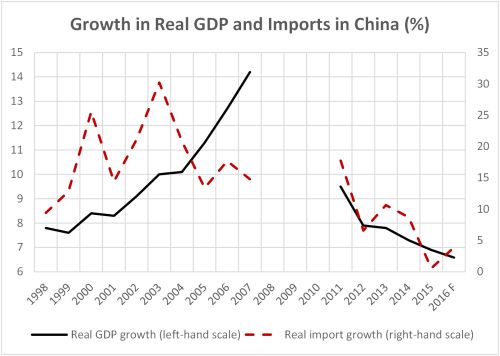

The slowing of growth in advanced economies partly resulted from the negative spillovers of a deceleration of growth in China since 2011, which combined with a shift away from high-import components of final demand and production, compressed Chinese imports from the rest of the world (Chart 1.7).2 The slowdown in China was indigenous for the most part, reflecting rebalancing toward a more sustainable growth model, and some tightening of fiscal policy and credit conditions at times.

Chart 1.7:

Source: IMF, World Economic Outlook, October 2016 database.

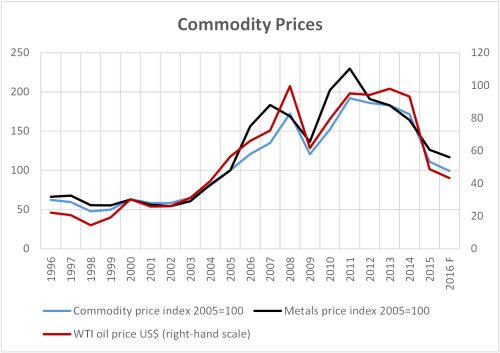

The slowdown in and change in composition of Chinese growth, and more generally the slowing in world growth, combined with increased supply in response to high prices, led to a fall in commodity prices from their 2011 peak (Chart 1.8). In real terms, commodity prices in 2016 are at about the same levels as at mid-2000s. These more sustainable levels result from the termination of the commodity supercycle that lasted from 2004 to 2014 rather than from the structural break in the growth rate of advanced economies that started showing up in 2011.3

Chart 1.8:

Source: IMF, World Economic Outlook, October 2016 database.

Accompanying subdued growth of demand in advanced economies was a decline in potential output growth due to adverse demographics and lower trend labour productivity growth (Chart 1.9). Population aging per se would have cut growth in trend aggregate labour force participation and hours worked by 0.4-0.5 percentage points per year over 2011-2016. Lower productivity growth, on the other hand, would have been partly a consequence of persistent weak growth of demand, which discouraged business investment.

Chart 1.9:

Source: OECD database. Estimate for 2015 from the authors.

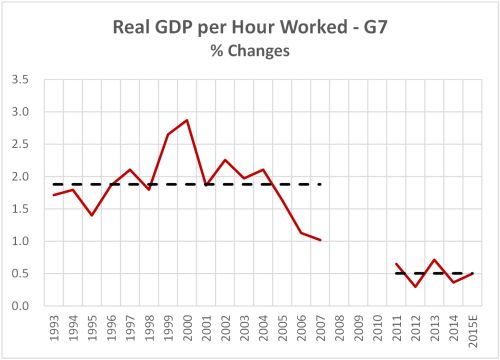

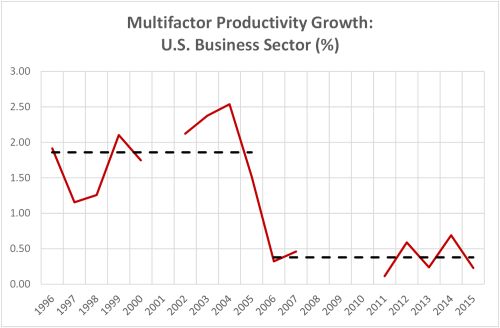

The fall in trend labour productivity growth also reflected a fall in trend multifactor productivity (MFP) growth. In the U.S., trend MFP growth was unusually high in 1996-2005 as business models and logistics more fully captured the benefits of ICT and Internet (Chart 1.10). Trend productivity growth petered out in 2006, well before the onset of the financial crisis, and has since remained in the doldrums.

Chart 1.10:

Source: U.S. Bureau of Labor Statistics.

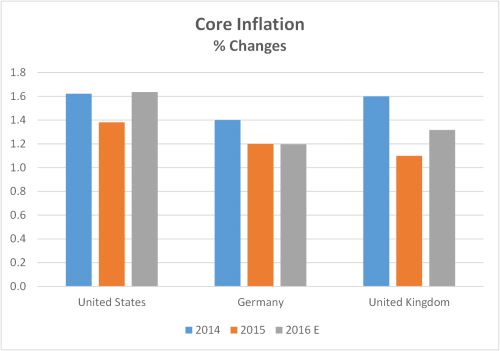

Even after several years into the recovery, core inflation has remained subdued as a result of domestic and global excess supply and moderate growth in wage costs (Chart 1.11).

Chart 1.11:

Sources: OECD database and U.S. Bureau of Economic Analysis. Core inflation: U.S.: PCE excluding food and energy; Germany and U.K.: CPI excluding food and energy. 2016 figures: U.S.: average of January to September; Germany and U.K.: average of second and third quarters.

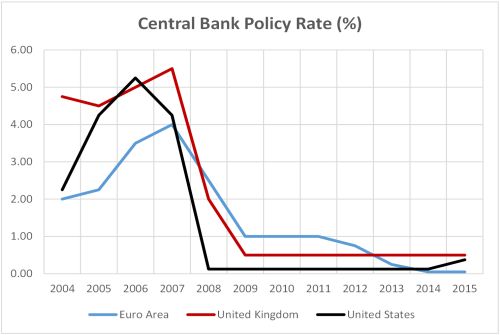

Slack in the labour and product markets and low core inflation prompted monetary authorities to keep policy interest rates near zero and, in a few important cases, to engage in a massive expansion of their balance sheets through quantitative easing (Chart 1.12). The lower effectiveness of monetary policy once policy interest rates were reduced to near zero, as they were by 2009, pervasive uncertainty about future prospects, which made households and businesses more cautious in taking advantage of low interest rates, high household debt levels to start with, and in some cases credit constraints help explain why demand has remained inadequate and inflation low in spite of exceptionally accommodative monetary policies.

Chart 1.12:

Source: IMF, International Financial Statistics.

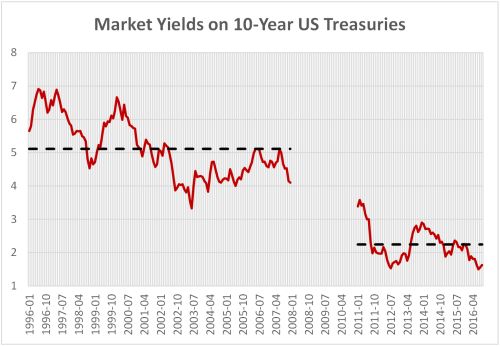

Financial investors' focus on the risk of prolonged lower-than-expected inflation in a context of low growth has contributed to expectations of low short-term rates for a long time and hence persistently low long-term interest rates and a flattening of the yield curve since early 2011 (Chart 1.13).

Chart 1.13:

Source: Board of Governors of the Federal Reserve System.

Summary 2011-2016

To conclude this section, it is clear that structural developments have been less favorable to growth in the advanced economies in the last six years than in the decade that preceded the financial crisis. These structural developments, whose intensity varies from country to country, relate to lower trend productivity growth (Chart 1.9), higher saving rates by households (Chart 1.3) and governments (Chart 1.4), lower business investment rates (Chart 1.5), and lower trade intensity (Chart 1.6). In addition, as will be discussed below, demographics have become more unfavorable to growth (Chart 2.1).

Section II: Factors Conditioning Growth: 2016-2020+

The persistently low growth of advanced economies over 2011-2016 represents a structural break from the much higher trend growth rate that prevailed during the two decades that preceded the financial crisis. Part of this recent weak performance has been the consequence of the financial crisis (e.g., private and public debt reduction), the effect of which should diminish over time, and part has been due to structural developments and increased uncertainty, both of which likely to persist in the years to come. We believe that these structural factors will keep demand growth by households and businesses subdued as they realize that growth in lifetime income and potential output would now be lower, or at least more uncertain, than perceived before. We conclude that the "new normal" described in Section I is likely to persist in significant measure to at least the end of this decade and that businesses should plan accordingly.

In this section we discuss key factors that have shaped recent performance and are likely to condition growth in aggregate demand and potential output over the next several years: demographics; investment rate; productivity growth; transition in China; commodity prices; and trade developments. The effectiveness of economic policies in supporting growth is another such factor, but it will be discussed in Section IV on the implications of the "new normal" for governments and businesses.

Demographics

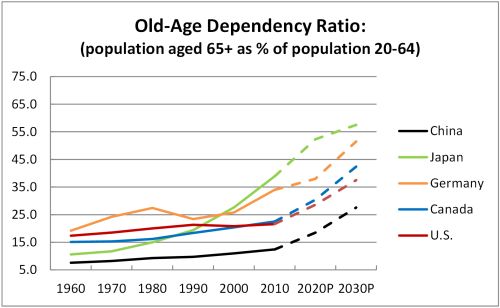

Various demographic projections concur in showing slower growth in new labour force entrants and population aging (Chart 2.1) over the next decades. These adverse trends are likely to be only partly offset by a rise in the labour force participation of older workers in response to economic pressures or incentives to work more and longer, such as expected increased longevity, modest returns on savings and improved health status. In Canada, for example, population aging would cut labour force growth by about 0.5 percentage points per year although an increase in the labour force participation rate of older age groups is likely to offset some of this decline by as much as 0.2 percentage points annually in the next several years.

The slowdown in trend hours worked resulting from demographics will depress potential output growth and leaves less room for demand expansion without triggering a rise in inflation. Thus projected slower growth in potential output, partly due to demographics, anchors projected slower growth in aggregate demand in the medium term.

Chart 2.1:

Source: United Nations, World Population Prospects, the 2015 Revision.

Demographics, notably expected increased longevity, may also have a direct restraining impact on household demand by prompting workers and retirees to save more out of their current income in order to finance a longer period of retirement (dynamic effect). It is true that the rise in old-age dependency rates associated with population aging may tend to reduce the aggregate household saving rate because the increasing fraction of the population in retirement would tend to save at a lower than average rate (static effect). However our own calculations, based on plausible assumptions about saving rates by age group4 and projections of population shares by age group, show that the static effect for Canada would be very small over the next decade and is likely to be more than offset by a modest increase in the saving rate of the 50-65 age group.5 On net, therefore, we judge that demographics will likely boost the aggregate household saving rate in Canada over the next decade and thereby directly contribute to hold back the pace of aggregate demand growth.

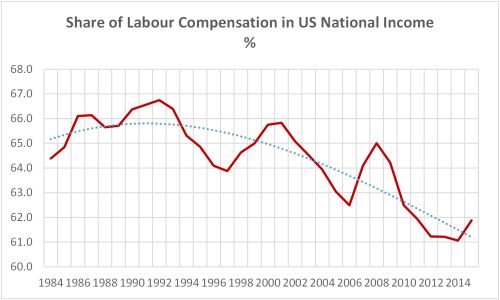

Other structural factors that would have restrained household demand growth over the last decades and might continue to do so, in the U.S. at least, include a decline in the labour share of national income and rising inequality of income (Chart 2.2). A decline in the labour (compensation) share, the counterpart of which is a rise in the capital (profits, financial investment income, property income...) share, would tend to restrain the contribution of consumption to real GDP growth. Rising inequality of income would have a similar effect as an increasing share of total income would accrue to high-saver households, thereby reducing aggregate consumption growth.6

The consumption share of U.S. GDP actually turned out to be higher over 2008-2015 than 1996-2007 in spite of a declining labour share and rising inequality. This was made possible by a sharp rise in household debt relative to income, supported by exceptionally low interest rates and hence debt service costs. Going forward, as interest rates rise, the room for increased reliance on debt is limited, thereby offering little further cushion against the negative effects on consumption of continued decline in the labour share and rise in inequality.

Chart 2.2:

Source: U.S. Bureau of Economic Analysis.

Business Investment Rate

Business investment rates in 2011-2015 appear to have been held back by uncertainty about growth prospects and future rates of return. With apparently still high hurdle rates on fixed investment, U.S. firms would have diverted more earnings than before to dividends, share buy-back, mergers and acquisitions relative to fixed investment, at least partly for the purpose of boosting the price of their equity in the short term. Real fixed nonresidential investment saw its contribution to real GDP growth reduced by 0.4 percentage points per year in 2011-2015 relative to the combined years 1996-2000 and 2004-2007. Perceived uncertainty about the future evolution of factors that condition growth prospects and future rates of return is likely to continue to weight on the pace of business non-residential investment in the years to come. These factors include among others:

- Political developments – e.g., populist, nationalist threats, potential geopolitical conflicts;

- Trade developments and protectionist threats as they affect access to markets and the need to build capacity to supply exports;

- Pace of innovation as it conditions the volume of investment required to exploit new technologies and develop new products;

- The potency of macro policies to significantly boost economic growth, eliminate slack, and significantly mitigate recessions; and

- The prices of oil and other commodities for producing countries.

In an uncertain environment, investment is postponed. Flexibility commands a premium so that firms tend to use more labour rather than increase capital per worker when they need to raise production. This tends to boost employment at the expense of capital deepening7 and therefore reduces labour productivity growth.8

Productivity Growth

The slow growth of U.S. labour productivity growth over 2011-2015 (0.6 percent per year for businesses) need to be put in perspective: rates for the total economy average 2.7 percent over 1948-1970, 1.5 percent over 1970-1994 and 2.3 percent over 1994-2004.9 Thus the recent period shows exceptionally depressed labour productivity growth in the U.S. by historical standards.

Conventional growth accounting reveals that this very slow growth in labour productivity is attributable mostly to a fall in capital deepening and, to a lesser extent, a low rate of multifactor productivity growth. Thus, a recovery in trend labour productivity growth in the future will likely depend on a rebound of both capital deepening (the investment rate) and multifactor productivity growth.

As discussed earlier, a future rebound in the investment rate, which itself would partly depend on a pick-up in the innovation rate, is far from assured given pervasive uncertainty ahead. This casts a cloud over prospects for a future recovery in labour productivity growth.

Prospects for a rebound in trend multifactor productivity (MFP) growth also are far from assured. At the outset, it must be acknowledged that what has caused the deceleration of MFP growth is not well understood by economic analysts. The presumption is that at least two broad factors have been involved. First, the pace of innovation, as it translates into higher labour and capital productivity, would have slowed markedly as a result of several factors, including a lower investment rate by businesses. In particular, investment in ICT, software and R&D grew significantly more slowly in 2011-2015 than in 1996-2007 (4.4 percent per year vs 6.4 percent per year in the U.S.) and these are the components of investment that are most likely to boost multifactor productivity growth. While nobody contests that technological progress is rapid in many spheres (e.g., ICT, artificial intelligence, big data, robotics, genomics...), there is intense debate as to whether this will have a broad enough scope to lift measured aggregate productivity growth significantly. Thus, both murky prospects for a lift in investment rate, particularly with respect to ICT, software and R&D, and the uncertain scope of current technological progress make the future contribution of innovation to productivity growth hard to project.

A second potential factor in the decline of productivity growth would be a decline in the intensity of competition. The pace of creation of new firms appears to have slowed markedly in a context of accelerated market consolidation by large, dominant firms.10 At the same time, low interest rates and debt charges would have boosted the survival of inefficient firms. Given that productivity growth tends to be rapid in new (small) firms and comparatively slow in older (large) firms,11 the average rate of productivity growth at the firm level would have declined as a result of these two developments, thereby depressing aggregate productivity growth.12 More importantly, a decline in competitive pressures would have reduced incentives for efficiency and innovation13 and rising protectionist pressure would reduce these incentives even further.

Another factor at play in the decline of productivity growth has been a shift of labour away from the high-measured-productivity financial services industry in the wake of the financial crisis. In the U.S., for example, the share of total employment accounted for by financial services fell from 6.1 percent in 2006 to 5.7 percent in 2015. Given that measured labour productivity is much higher in financial services than in the economy as whole, the shrinkage of the labour share of financial services contributed to depress aggregate labour productivity growth in the U.S. Of course, the relative importance of this factor would have varied from country to country. At this point, it is not likely that the relative shrinkage of labour in finance will significantly reverse in the next several years and raise aggregate productivity growth.

While one cannot be precise about the future evolution of productivity, our judgment is that a rebound in U.S. labour productivity growth from 0.5 percent per year is possible, but in all likelihood to not much more than one percent, considerably lower in any case than during the 1996-2007 period (Chart 1.9).

Transition in China

Further slowdown in the growth of China's final demand, further shift in the composition of that demand away from high-import-intensive investment toward consumption and services, and further production at home of some previously imported intermediate goods (onshoring) are to be expected in the years ahead as the economy continues to transition toward a more sustainable growth model and move up the value-added chain. This will have modest negative spillover effects on growth in the advanced economies through trade and in a number of commodity-producing countries through weaker trade and commodity prices. IMF research suggests that China's global spillovers would add another 25 percent to the direct effects of a Chinese slowdown in final demand growth on world growth (given growing China's weight in world output, now at 17 percent).14 Thus, a slowing of 2 percentage points in China would subtract 0.3 points from global growth directly and a further 0.1 points indirectly. The spillover effect would be much larger for some countries.

There is considerable uncertainty about the pace of the expected slowdown in China over the next several years. One downside risk in the short term arises from debt overhangs, property bubbles, and unhealthy state-owned enterprises. Chinese growth has proven to be surprisingly resilient recently, no doubt in response to a major easing of economic policy (fiscal, monetary and the exchange rate). This creates an upside risk to future growth relative to our expectations inasmuch as the Chinese government has the willingness and firepower to keep growth close to its planning targets over the next few years. As will be seen in Section III, our own projection calls for a fall in growth of 1.4 percentage points over the next two years, a significantly more pessimistic outlook than most others over this short horizon. This is because we think Chinese authorities will have to sacrifice more growth than they are ready to admit in order to accommodate other pressing policy goals, to facilitate transition to a service economy and to avoid exacerbating already large imbalances and financial risks in the economy.

Commodity Prices

The key point that we want to emphasize is that the supercycle of 2004-2014 is dead and that real commodity prices, particularly those of oil and industrial materials, will fluctuate around flat or at best slightly rising trends over the next several years. Demand for commodities will continue to grow, but at a more moderate pace as Chinese goods production and construction slow and global growth remains subdued. With respect to oil, a relatively price-elastic supply from the U.S. shale oil industry will likely contain the upward price pressure likely to emerge from the recent collapse of oil investment in the rest of the world. With respect to metals, substantial new production capacity in recent years will stem upward price pressure for years to come.

The implication of nearly flat real commodity prices ahead is that future growth in the terms of trade, real income and resources investment in commodity-producing countries, which include many emerging economies, will be limited, contributing to keep aggregate demand growth in these countries considerably lower than in 2004-2014.

Trade Developments

This sub-section takes account of recent analysis done by the OECD and the IMF on why the growth in world trade has stagnated. In the light of that analysis it considers the potential impact of recent political developments, notably the American election and the Brexit vote in the U.K. We also take a brief look at where Canada fits in this picture.

An OECD policy paper15 issued in September 2016 notes:

"A remarkable two decade period of rapid globalisation, during which the trade intensity of global GDP increased rapidly, came to an end with the financial crisis. Instead of world trade growing at more than double the rate of global GDP, in the wake of the crisis it has barely exceeded the growth rate of global GDP, slowing sharply from an average of 6½ per cent per annum over the two decades to 2008 to 3¼ per cent per annum over 2012-2015. During 2015 trade volume growth weakened further to 2½ per cent, and was again anaemic in the first half of 2016."

The OECD paper identifies both cyclical and structural reasons for the downturn. The paper observes:

"Trade growth in the pre-crisis period was boosted by world-wide liberalisation of trade policy, particularly through multi-lateral agreements, NAFTA and deepening of the E.U. single market during the 1990s. A further boost to trade came from the growing importance of global value added chains (GVCs), whereby production processes are fragmented across countries and so increased trade, particularly in intermediate products. As trade liberalisation measures slowed around 2000, world trade remained supported by the ongoing expansion of GVCs and was given a further boost by a growing contribution from the rapid emergence of China into the world economy."

Structural changes since the global financial crisis impacting negatively on the growth of trade include:

- a slowdown in the growth of GVCs,

- the declining effect of earlier trade liberalization which is now fully implemented, and

- the growth in restrictive trade measures taken since 2008.

While political will has helped keep protectionist forces in check there has been a steady creep in protectionist actions which is taking a toll. The WTO recently reported that "the share of world imports covered by import-restrictive measures implemented since October 2008 and still in place is 5% and the share of G20 imports covered is 6.5%."16

The IMF in its October 2016 World Economic Outlook also focuses on "Global Trade: What's behind the Slowdown?".17 The IMF concludes that, "Empirical analysis suggests that, for the world as a whole, up to three-fourths of the decline in real goods import growth between 2003–07 and 2012–15 can be traced to weaker economic activity, most notably subdued investment growth." Slower growth in China as noted elsewhere in our fall outlook is another factor weighing on the growth of world trade. However, like the OECD paper, the IMF also sees the role of structural factors as being important.

Both institutions believe that renewed trade liberalization would make a positive contribution to increased productivity and renewed growth in the global economy. This being said, over the remainder of this decade the prospects for trade liberalization, and for the international trading system more generally, look bleak. Equally bleak are the prospects for competitive pressures from expanding trade to stimulate growth in productivity, potential output and aggregate demand in the world economy.

Potential Trade Impact of Recent Political Developments

The election of Donald Trump as President of the United States and the aftermath of the Brexit vote in the U.K. create major uncertainties about the future course of trade policy globally. However, there are important differences.

In the U.K., the government of Prime Minister Theresa May has made clear publicly that it wants open trade with all its partners, but from a position outside the European Union. What is unclear is how it will get there and what sort of deal it will be able to strike with the E.U.

In the U.S., Donald Trump has taken a series of protectionist positions during the election campaign. Exactly how the bombastic rhetoric of the election trail will be translated into policy once he is sworn in as the 45th President on January 20 remains to be seen. What is clear already is that:

- During the campaign, in his "contract with the American voter", Donald Trump stated that as the first of "seven actions to protect American workers" he would "announce my intention to renegotiate NAFTA or withdraw from the deal under Article 2205."

- Also in the "contract", he said he would "announce our withdrawal from the Trans-Pacific Partnership". Then, on November 21, President-elect Trump provided a video "update on the transition and our policy plans for the first 100 days" in which he announced that on day one he is "going to issue our notification of intent to withdraw" from the TPP. "Instead," he continued, "we will negotiate fair, bilateral trade deals that bring jobs and industry back onto American shores". His video update was silent on NAFTA.

- The Transatlantic Trade and Investment Partnership (TTIP) negotiations between the U.S. and the E.U. have been effectively sidelined.

- The fate of other negotiations, such as the Trade in Services Agreement (TISA) negotiations in Geneva and other WTO negotiations, have been thrown up in the air.

- Mr. Trump has appointed Dan DiMicco, the former CEO of Nucor, the largest steel producer in the U.S., as the point person for trade on the transition team. DiMicco has taken a tough anti-China stance and has made clear the goal of the administration will be to eliminate the trade deficit and to "balance" trade.

All of these factors mean that the actions of the new administration are much more likely to be trade restricting rather than trade liberalizing. If that is the case they will clearly have a negative impact on global growth.

It is possible that the Republican led Congress, most of whose members are pro trade, will have a restraining effect on the President as he approaches the trade agenda, but he has a lot of wind in his sails and a lot of tools in his pocket. Most business interests in the U.S. will be pressing for open trade, including agriculture interests in many "red" states.

Obviously this turn of events presents real challenges for Canadian policy. As the largest trading partner of the U.S. we are on the edge of a crisis and preparations for what lies ahead should be a top Canadian government priority.

The government should be prepared to enter discussions with the new administration on NAFTA. To prepare for the likelihood that there will be negotiations to change NAFTA, the government should be developing a list of how Canada thinks the agreement could be improved. We may not like the proposals that come from the American side of the table, so deploying our own wish list will be tactically important. One proposal that is almost certain to arise from the U.S. will be targeted at dismantling Canadian supply management programs in the dairy and poultry sectors.

It will be important for Canadians to work with their many allies in the U.S. with whom common interests are shared, among others on such important issues to Canada as country of origin labeling regulations for meat, softwood lumber and the Keystone-XL pipeline.

The government should also exchange views bilaterally with the Mexicans. Sharing intelligence and comparing notes will be useful. Bilateral discussions would also help guard against efforts by the U.S. to play us off against each other.

We recommend that the Canadian government set two overriding priorities with respect to Asia. First, now that the TPP has been upended, re-engage bilateral talks with Japan to conclude the Comprehensive Economic Partnership Agreement negotiations to take advantage of benefits that would otherwise have come to Canadian business through participation in the TPP. Second, expedite the agreed exploratory discussions for a possible Canada-China Free Trade Agreement, recognizing not only that China is our second largest trading partner but, even more importantly, that China will play an increasingly large role in setting international trade rules, especially if the U.S. withdraws. The leadership of the world trading order, which passed across the Atlantic from the U.K. to the U.S. after World War I, is now about to be passed across the Pacific from the U.S. to China.

As the U.S. enters a more protectionist phase, Canada should differentiate itself as being open and outward looking, thereby promoting Canada as a hospitable site for investment.

Canada now has a major opportunity to strengthen its relationships with the E.U. The CETA agreement between Canada and the E.U. has finally been signed and prospects are good that it will enter into force provisionally in 2017 after ratification by the European Parliament and after the necessary implementing legislation is passed at the federal and provincial levels in Canada. Given the uncertainty surrounding the U.S.-E.U. TTIP negotiations it seems likely that Canadians will enjoy preferential access to the E.U. for some time before their American competitors catch up. This could offer Canadian business a major opportunity to consolidate the benefits from the CETA. It will also increase the attractiveness of Canada as an investment location for companies interested in serving both the North American and European markets.

It is clear that not every word uttered by Donald Trump during the election campaign was carefully calibrated. Canadians will need to watch closely as the administration develops its approach to various trade issues. This transition will be more complicated than most and it may be summer at least before some important points are clarified. During this period the best approach for the Canadian government is to keep a low profile while quietly preparing for various scenarios.

It is also likely that even this administration over time will begin to realize that it will be easier to manage American interests in a world with trade agreements than in one without.

It is even possible that we may see an interest in the prospect of new approaches in the WTO. It may begin with fireworks as the U.S. takes on China but that might set the stage for a new effort at rule-making designed to take account of the way the world now is rather than how it was in 1986 when the last successful multilateral round of negotiations was launched. Such a process might also be given a push by the U.K. as it seeks to assert itself as a fully independent member of the WTO. Canadians should be giving thought to how to use such a development to advance our own interests. We should be open to all possibilities for reviving "the virtuous cycle of trade and growth".

Conclusion

Before closing Section II, the table below summarizes the evolution of key factors discussed earlier.

| Evolution relative to 1996-2007 | ||

| 2011-2016 relative to 1996-2007 | 2017-2020 relative to 2011-2016 | |

| Demographics | ||

| Labour force growth | lower | slightly lower |

| Household saving rate | higher | slightly higher |

| Income distribution | ||

| Labour share of income | lower | stable to lower |

| Inequality of household income | greater | greater |

| Investment | ||

| Investment share of GDP | lower | uncertain |

| Incentives for buyback/dividends, M&A | greater | uncertain |

| International trade intensity | much lower | lower |

| Productivity | ||

| Innovation | lower | uncertain |

| Growth ICT, software and R&D investment | lower | uncertain |

| Firm creation rate | lower | uncertain |

| Trend growth in China | lower | lower |

Apart from demographics, the medium term evolution of key elements of the new normal for advanced economies, including uncertainty itself, remains far from clear but nonetheless could well lead to persistent low growth. In the short term at least, there appears to be agreement that growth in advanced economies will remain subdued generally—a continuation of the "new normal".

Section III: Global Growth Outlook 2016 – 2018

Against the background of the preceding analysis, we project a "low for long" scenario with the global economy growing on average at about three percent per year from 2016 to 2018, as in the Spring 2016 Outlook (Table 3.1). While recovering in part from a marked softening in 2016, growth in advanced economies remain on the low-growth path of the "new normal" in 2017 and 2018. Growth for emerging economies, on the other hand, strengthens slightly in 2016 before gradually losing ground in the next two years. This is the result of a cyclical recovery from the slowdown of 2014-15 in many emerging economies, which gets blunted in 2017 and 2018 by the direct and indirect effects of a pronounced slowing of growth in China.

Table 3.1:

Short-term Prospects for Output Growth (%)*

| Share (%) | 2015 | 2016 | 2017 | 2018 | |

| Canada | 1.5 | 1.1 | 1.2 (1.4) | 2.0 (2.4) | 2.0 (1.9) |

| United States | 16.4 | 2.6 | 1.5 (1.9) | 2.3 (2.3) | 2.3 (2.1) |

| Euro area | 12.3 | 2 | 1.5 (1.6) | 1.5 (1.6) | 1.5 (1.5) |

| Japan | 4.6 | 0.5 | 0.6 (0.8) | 0.6 (0.7) | 0.5 (0.6) |

| China | 17 | 6.9 | 6.6 (6.1) | 5.7 (5.2) | 5.2 (4.8) |

| Rest of World | 48.2 | 2.7 | 2.9 (2.9) | 3.2 (3.2) | 3.2 (3.2) |

| World | 100 | 3.2 | 3.0 (3.0) | 3.1 (3.1) | 3.0 (2.9) |

*Figures in brackets are from the Bennett Jones Spring 2016 Economic Outlook.

- This scenario incorporates no major specific shock from political or trade developments. This is a big assumption in view of the current multiple risks, arising notably from the results of the U.S. election. Most likely, however, the environment will be less trade friendly.

- Interest rates are expected to remain low, with only a gradual rise in 2017; U.S. rates would rise further in 2018 if U.S. fiscal policy becomes as expansionary as Mr. Trump has promised. In any event, the total rise in U.S. policy rate should be limited by historical standards, reflecting a much lower neutral interest rate than in the past.18

- WTI oil prices are expected to trend upwards until they reach about US$60 in 2018. They are likely to show volatility around this trend.

U.S. growth finally picked up well beyond its potential rate in the third quarter of 2016 (2.9 percent) as inventory investment and net exports rebounded after several quarters of negative or very weak contributions to growth. Growth should average only 1.5 percent for 2016 as a whole, but rise to over 2 percent over the next two years.

The extent to which U.S. growth over the next two years exceeds its medium term potential (estimated at 1.8-1.9 percent) depends in part on the magnitude of Mr. Trump's promised tax cuts and spending on infrastructure. At this point our best guess is that these fiscal actions would start in the second half of 2017 and might cumulate over time to more than one percent of GDP. Should this be the case, this stimulus would raise real GDP growth by 0.1 to 0.2 percentage points in 2017 and 0.3 to 0.5 points in 2018 so that GDP growth over those two years should average about 2.3 percent. Growth in business non-residential investment should pick up in response to stronger aggregate demand growth and an economy at capacity while net export gains are likely to be restrained by additional upward pressure on the exchange rate of the U.S. dollar and stronger domestic demand.

With an economy roughly at capacity to start with, the projected above-potential GDP growth rate would be expected to generate some inflationary pressure and the Federal Reserve would be expected to react by raising its policy interest rate in both 2017 and 2018. By the end of 2018, the policy interest rate would likely have risen to close to 2.5 percent in nominal terms. The rise in U.S. rates would likely widen the interest rate differentials in favour of U.S. dollar assets and put upward pressure on the U.S. dollar.

The rebalancing of economic policies in the U.S. would have spillover effects on the rest of the world, including Canada, through trade and financial linkages. Section IV discusses the advantages of a rebalancing of economic policies for advanced economies.

In Canada growth in 2016 is turning out to be very weak for a second year in a row as a result of low U.S. growth in the first half of the year, continued difficult adjustment to the earlier fall in commodity prices and collateral decline in real income, tough competition in export markets, further retrenchment in inventory investment, and wildfires in the Fort McMurray area in the second quarter.19

Looking ahead, growth is expected to pick up from slightly above one percent in 2016 to close to two percent in 2017 and 2018. In view of the current considerable slack in the economy, this somewhat faster-than-potential pace would not put pressure on core inflation beyond the two-percent target over the next two years and therefore would leave little room for policy rate increases. The resultant widening interest-rate differential in favour of the U.S. would exert downward pressure on the Canadian dollar, offsetting an upward pressure on the currency arising from the projected increase in international oil prices. The exchange rate could thus fluctuate considerably during certain periods as expectations adjust to new information. For planning purposes, we expect the Canadian dollar exchange rate to move within a range of 71-77 U.S. cents over the projection period.

As in the spring, we believe that several factors would support stronger Canadian growth in the next two years. Total business non-residential investment, which has been depressed by the retrenchment in the oil and gas sector in the last two years, should resume growth in 2017 as the economic expansion gathers momentum and investment in the oil and gas sector stabilizes or edges up. Likewise the drag on final domestic demand exerted by the loss of real income associated with the earlier fall in the prices of oil and other commodities should diminish, thereby boosting growth relative to 2016. Firmer growth in the U.S., including in import-intensive U.S. investment in machinery and equipment, should also support a faster Canadian expansion via stronger export demand. Finally, stimulative fiscal measures by the federal government, mainly in the form of increased infrastructure investment and larger transfers to households (Canada Child Benefit), would boost growth in 2017 relative to 2016. These measures would continue to support the level of activity in 2018 but are unlikely to make a significant additional contribution to growth in that year.

For Canada the risks revolve around:

- the impact of President Trump policies on U.S. demand and interest rates;

- the evolution of oil prices;

- the impact of the federal fiscal stimulus; and

- the competitiveness of Canadian firms in export markets, notably the U.S.

An additional risk regarding Canadian exports relates to the potential restraining effects of U.S. protectionist measures put in place by Mr. Trump's government.

To conclude, at this juncture we expect for the short term much the same scenario of subdued global expansion and strengthening growth in the U.S. and Canada as in the Spring 2016 Outlook. With a Trump administration in place, a rebalancing of economic policies in the U.S., which would have taken place at least in small measure anyway, will likely be reinforced to some degree insofar as an expansionary fiscal policy boost growth and inflation in the U.S. in the short term. This fiscal stimulus would have positive spillovers on the rest of the world, including Canada, in the short term. At the same time a more protectionist trade policy by the U.S. would certainly have negative effects on the rest of the world. While the U.S. fiscal stimulus and its positive spillovers would be over by 2018, the drag on global growth arising from the U.S. protectionist measures would continue and possibly get worse.

SECTION IV: IMPLICATIONS FOR GOVERNMENT POLICIES AND BUSINESS STRATEGY

Implications for Economic Policies

Rebalancing economic policy with less reliance on monetary policy and more reliance on public investment and structural policies would help to achieve stronger demand growth in advanced economies and hence help break out of the "new normal". At the September 2016 G20 meeting, many government leaders expressed interest in such rebalancing. While the economic plan of the Trump administration in the U.S. implies a vigorous rebalancing, any rebalancing on the coordinated international basis that would be necessary to materially boost global growth remains problematic.

Monetary Policy

Central banks contribute to the stabilization of real domestic demand through the setting of their policy interest rate. Traditionally, a cut in interest rates worked to induce increased demand in the near term because businesses and consumers viewed that over time inflation would increase—hence there was an advantage to bringing forward intended expenditure and take advantage of lower borrowing costs. The reduction in rates would also have an impact on the exchange rate, inducing demand for domestic output. Since the onset of the financial crisis, a slide in policy interest rates to near zero supplemented by a heavy dose of unconventional monetary policy in a number of advanced countries provided support to aggregate demand and boosted asset prices.

The efficacy of monetary policy to stimulate demand appears to be lower now than it used to be. First, the limited success of the extraordinary efforts of central banks to lift aggregate demand growth beyond mediocre rates after 2010 have led to expectations that interest rates will be "low for long" and to a flattening of the yield curve, thereby providing less incentive to pull forward more consumption and investment. Second, with household debt/disposable income ratio at an all-time high in Canada, and approaching that again in the U.S. and many other economies (including EMs), households are reluctant to incur more debt even though the ratio of current debt service costs to disposable income is low, indeed at an all-time low in Canada (6.4 percent vs 11 percent in 1990).20 Third, "radical uncertainty", to use a Mervyn King term,21 prevails and induces caution on the part of households and businesses. Finally, the efficacy of monetary policy is limited by the effective lower bound on nominal interest rates. The greatest danger at present is that there is no room to lower rates by the 400+ basis points needed to pull an economy out of recession before hitting the effective lower bound, should there be another dramatic collapse in demand.

Not only is there almost no practical room to use monetary policy going forward to stabilize growth in the event of a major negative demand shock, there is accumulating anecdotal evidence and increasing concern that today's ultra-low rates may actually be retarding growth (by inducing a rise in retirement saving), widening income inequality and distorting financial markets (causing uncertainty and leading to a misallocation of real resources).

Fiscal Policy

In the end it is not going to be modifications to monetary policy alone that offer the greatest chance for macro-economic policy to facilitate the escape from the current global economic stagnation. Fiscal policy has an important role to play as indeed it did in the past, not only in the severe slump of 2008-2009 but also as part of the activist Keynesian approach to stabilize the economy that prevailed in the first few decades of the post-war period. Recent statements from the IMF and the communiqué from the G20 meeting in Hangzhou indicate that many authorities now acknowledge the importance of expansionary budgets as a source of aggregate demand growth. Clearly this was recognized by the Canadian federal government in setting its 2016 Budget. But it is not just change in the size of the deficit that matters for growth; change in the composition of spending and revenues is even more important in the medium term. Thus, increasing public investment in productivity-enhancing infrastructure raises the long term growth trajectory—and hence expected real growth over the longer term.22

Globally many governments have the capacity to increase their borrowing at current interest rates provided that borrowing is used to finance productivity-enhancing physical or human infrastructure—infrastructure which will yield future cash flows to governments. The Canadian government has seized this opportunity in the spring 2016 Budget by committing in a first phase to invest $14 billion in infrastructure between 2016 and 2020. In a fall economic statement on November 1, the federal government committed to deliver an additional $81 billion between 2017 and 2027 to fund public infrastructure, this time partly through the agency of a newly established Canadian Infrastructure Bank and with a focus both on attracting private sector investment and relying at least in part on user charges to fund the operational, maintenance and financing costs of new infrastructures.23 Clearly all these infrastructure initiatives have the potential, if well executed, not only to stimulate demand in the economy over the next several years, but, more importantly still, to enhance trend productivity growth and hence potential output growth over the longer term.

Policy Mix

While demographic, technological, and structural factors clearly limit the extent to which macro-economic policies alone can promote higher growth, judicious coordination of monetary and fiscal policies can get countries closer to that limit than can disparate efforts of central banks and finance ministries in their respective domains. At the present time, both price and financial stability would be better served by somewhat higher policy interest rates—rates that would not imply a sacrifice of employment and growth if (and this is a big if) fiscal policy were more expansionary.

Macro-economic policies alone, however, will not materially lift long-term growth rates. If the advanced economies of Europe and North America are to achieve growth rates closer to those experienced in the second half of the last century, it is essential that governments focus on growth-enhancing structural policies—trade, education, health, competition, income distribution, taxation and public infrastructure investment. Competition and open international trade provide incentives for the development of new technology. But it is labour, education and income distribution policies that provide reasonable assurance that gains from trade and technological progress will be reasonably shared. Without such assurance, popular resistance to change can grind economic growth to a halt.

To conclude, a rebalancing of economic policy to place greater emphasis on government investment and structural policies and somewhat less reliance by central banks on ultra-low interest rates and long-term asset purchases (QE) would be a step towards escaping from the current stagnation of global economic growth, enhancing competition and productivity-raising investment, improving the distribution of income and wealth, and supporting the losers from technological change and globalization. Although such rebalancing is more likely than not, its implementation remains uncertain both in timing and extent. One important issue with increased reliance on fiscal policy is that it is hard to know when enough is enough and hard politically to turn the wheel in a timely fashion when and if fiscal restraint is ultimately required.

Implications for Business Strategy

In this world of slow growth and heightened uncertainty, businesses need to put an emphasis on flexibility, adaptation and technological innovation while at the same time maintaining a reserve of dry powder to meet unforeseen circumstances. Continued reinvestment of profits at a somewhat lower hurdle rate than was used a decade ago will be essential to maintaining productivity and competitive advantage over time.

Until well into 2017 there will be a good deal of political and economic uncertainty related to the Trump administration actions, Brexit, the December vote in Italy, and national elections in France and Germany. During this period, it would be wise for businesses to make plans for the future but refrain from making commitments until these uncertainties are substantially lifted.

Footnotes

1 Gains in international trade intensity are measured by the differences between growth in world real GDP and growth in world trade volumes of goods and services. For more details on the causes of the decline in trade intensity, see the sub-section on trade developments in Section II.

2 The fall in import growth exaggerates the amount of negative spillovers on the rest of the world. Some of the slower import growth reflects negative shocks originating outside China. See IMF. 2016. "Spillovers from China's Transition and from Migration", World Economic Outlook, October.

3 Commodity supercycle here refers to "the rise, and fall, of many physical commodity prices (such as those of food stuffs, oil, metals...) which occurred during the first two decades of the 2000s (2000–2014), following the Great Commodities Depression of the 1980s and 1990s. The boom was largely due to the rising demand from emerging markets..., particularly China..., as well as the result of concerns over long-term supply availability...The 2000s commodities boom is comparable to the commodity supercycles which accompanied post–World War II economic expansion and the Second Industrial Revolution in the second half of the 19th century and early 20th century." Wikipedia, 2000s Commodity Boom entry.

4 The distribution of saving rate by age groups would have a hump shape with a peak at age group 55-59.

5 The weak static effect stems from slow increases in the population shares of older age groups (65+) and decline in the share of the young age group (0-24) whose saving rate is practically nil.

6 Intra-country income inequality has been going up mainly because income has been rising rapidly at the very high end relative to the middle income earners. Inter-country inequality has been going down because of huge increases in income overall in countries like China, India, Indonesia, etc. The overall effect has been an increase in a global class of super rich combined with a global decrease in poverty and a strong growth of a middle class (in emerging economies). See Milanovic, B. 2016. Global Inequality: A New Approach for the Age of Globalization, Harvard University Press.

7 Capital deepening refers to an increase in capital input per labour input. With a slower growth in labour input, the same capital deepening would be achieved with a slower growth in capital input, hence lower investment. Besides uncertainty, demographics could lead to a lower investment rate than otherwise as the projected slower growth in hours worked would require a lower investment rate to accommodate the same pace of capital deepening as before. If the lower supply of hours leads to upward pressure on wages, however, desired capital deepening may actually rise faster than before and this would help support the investment rate.

8 The potential conflict between capital deepening and job creation seems part of the political dynamic trade-off that appears to be taking place.

9 Gordon, R. 2016. The Rise and Fall of American Growth. Princeton University Press, Table 18.3.

10See "The rise of the superstars", The Economist, September 17-23, 2016, and Council of Economic Advisers. 2016. "Benefits of Competition and Indicators of Market Power", Council of Economic Advisers Brief, April.

11 For evidence on firm size effects, see Baldwin, J.R., D. Leung and L. Rispoli. 2013. "Canadian Labour Productivity Differences Across Firm Size Classes, 2002-2008." Statistics Canada, The Canadian Productivity Review, April.

12 However, small firms tend to have a lower productivity level than large ones. A rise in the proportion of large firms would thus raise the average level of aggregate productivity as a result. The net effect on aggregate productivity growth of slower average growth of productivity at the firm level and rising aggregate level of productivity as concentration increases is an empirical issue.

13 This argument must not be pushed too far. Empirical support was found for the prediction that the threat of firm entry spurs innovation in sectors close to the technological frontier whereas it discourages innovation in laggard sectors because it reduces the incumbents' expected rents from innovating. See Aghion, P., R. Blundell, R. Griffith, P. Howitt and S. Prantl. 2006. "The Effects of Entry on Incumbent Innovation and Productivity". NBER Working Paper No. 12027.

14 IMF (2016), p. 174.

15 "Cardiac Arrest or Dizzy Spell: Why is World Trade so Weak and What Can Policy Do About It?", OECD Economic Policy Paper. September 2016 No. 18.

16 "Trade restrictions among G20 remain high, despite slight slowdown in new measures", World Trade Organization, November 10, 2016.

17 World Economic Outlook (WEO) Subdued Demand: Symptoms and Remedies, October 2016

18 The neutral interest rate is the policy rate consistent with the economy operating at capacity and inflation remaining on target. Given a lower neutral rate at present, actual policy rates need not rise as high as before to eliminate excess demand in the economy.

19 Oil sands production returned to normal by the third quarter so that the temporary wildfire-related fall in oil sands production would have had only a small effect on Canadian GDP growth for 2016 as a whole.

20 Statistics Canada Cansim 380-0073.

21 King, M. 2016. The End of Alchemy: Money, Banking and the Future of the Global Economy. Norton.

22 Public infrastructure covers a wide range of assets. Some would enhance population welfare but have dubious value when it comes to long-run enhancement of productivity. Thus the mix of infrastructure investment, and not just the amount, matters for long-term growth.

23 See Dodge, D. and J. Bird. 2016. " Minister of Finance Commits to Establish a Canadian Infrastructure Bank", November 1 and Dodge, D. 2016. "Canada's Infrastructure Bank Done Right", November 3.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.