Taxes

Law No. 11-92 dated May 31, 1992 , which establishes the Tax Code of the Dominican Republic , as amended , lays down general provisions applicable to all internal taxable contributions and the emerging legal relations of them. This law is divided into 5 sections: ( i ) General Principles , Procedures and tax penalties ; ( ii ) income tax ; ( iii ) Tax on the Transfer of Industrialized Goods and Services (ITBIS ) ; ( iv ) Selective Consumption Tax (ISC ) ; and ( v ) Tax Assets ( ISA ) .

The Dominican Tax Administration specifically named as Dirección General de Impuestos Internos (DGII) is the institution responsible for the collection and administration of the main taxes and fees in the Dominican Republic. Ahead we indicate those most relevant taxes, as well as their scope and respective payment.

Income Tax (ISR)

It is the tax levied on all income, profit or benefit gained in a fiscal period from Dominican sources, natural persons and legal entities, regardless of nationality, residence or domicile, as well as undivided sucessions cause residing in the country. In addition, any natural or legal person residing or domiciled (after the third year of residency) in the Dominican Republic must pay taxes on their foreign income from investments and financial gains.

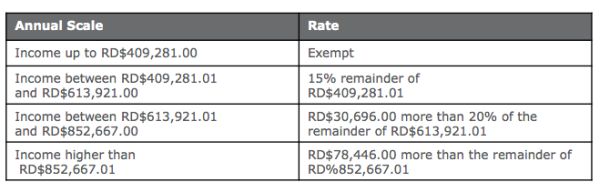

Natural persons

Individuals that benefit from an exemption on their annual income up to RD $ 409,281,000.00 (effective January 1, 2016 ). An amount that exceeds this sum will experience a progressive rate, as follows:

The deadline for submission and payment of (the affidavit) the sworn ISR declaration of natural persons and undivided estates is March 31st of each year and shall correspond to the income of the previous year (January 1 to December 31).

Legal persons

Legal persons domiciled in the country pay 27 % of the net income annually (applicable from 2015 and 2016 rate). The taxable amount is determined after deducting the overall gross income those deductions allowed by law, such as interest payments, taxes , insurance premiums , extraordinary damages , depreciation, bad debts , among others.

The deadline for submission and payment of the affidavit of legal entities or companies date is 120 days after the closing date of the company. The closing dates set out in the Tax Code companies are: from March 31, June 30, September 30 and December 31.

Withholding Income Tax

Withholding agents are designated by the legislation and regulations (public institutions, commercial companies and other) as direct responsible that must withhold the corresponding tax, and return it to the tax authorities within the prescribed period.

The main income subject to withholding are: (i) monthly salary that exceeds the monthly tax exemption (excluding employee contributions to the Social Security Treasury); (ii) payments abroad in general; (iii) interest on loans to foreign credit institutions; (iv) Dividends paid in cash; (v) rents paid to individuals; (vi) fees for services and commissions paid to individuals; (vii) prizes or lottery winnings or promotional campaigns and (viii) payments made by the State for the acquisition of goods and services not performed as an employee.

The deadline for submission and payment of this tax is within 10 days after the end of the declared period.

Abroad payments

Under Article 305 of the Dominican Tax Code, unless a different treatment is available for a particular category of income, any payment or credit on account of taxable income from Dominican sources to individuals, corporations or non-resident or not domiciled entities in the country, it is subject to the application of a withholding income tax at the same rate under Article 297 of the Code for legal entities. Such payment shall be considered as single and definitive tax.

For these purposes, the income gross shall be paid or credited, without proof to the contrary, as net income subject to withholding, unless the law stipulates assumptions regarding the net income earned, in that case the base tax for the calculation of the retention would be the imputed income.

In this sense, under Article 306 of the Code, exists a differentiated application for whoever pays or credits into account interests of Dominican source to natural persons, corporations or non-resident entities, which are subject to a 10% retention rate as payment.

Paid Interest or Accredited to Natural Residents

On another note, from the Law No. 253-12, any payment or credit on account of interest for residents or domiciled individuals in the country are subject to the application of a 10% withholding as single and definite payment.

It is said that individuals do their income tax return for the purpose of requesting a refund of amounts withheld by interest, in that case it shall be considered an advance payment of ISR, when it plays one of the following conditions: a) when the net income, including interest, is less than RDS240,000.00; and b) when the net income is less than RD $ 400,000.00, as long as their interest income does not exceed twenty-five percent (25 %) of its net taxable income.

In case taxpayers opt for this option, they must provide the DGII documentation they require to prove the amount of the net taxable income as well as interest income and retention. It is understood that the Ministry of Finance, in coordination with DGII, regulate the different types of interest, meaning any transfer to third parties of capital.

In the case of instruments values, the retention agent is the central ISR values.

Dividends

Dividends paid or credited by a commercial company to its shareholders, local or foreign, are subject to the application of a withholding tax of 10% (from 2012), as the sole and final payment. It is worth mentioning that since Law No. 253-12, permanent establishments in the country must withhold and pay the same amount when referring amounts to its headquarters for these concept or a similar one.

Capital Gains

Gains from the sale, barter or other disposition of a capital asset are subject to payment of 27% (applicable from 2015 rate). To determine capital gain, the cost of acquisition or production adjusted for inflation will be determine from a reduction made from the price or sale value of the respective asset. In the case of depreciable assets, the cost of acquisition or production to consider will be the thereof residual and over these the adjustment will be made.

This particular tax has the particularity that in virtue of the general norm 07-2011 issued by DGII, legal persons that legal persons who purchase stocks and shares should act as withholding agent of this tax, withholding 1% of the amount paid to seller of the same, be it physical, legal, national or foreign. Such withholding is a prepayment of tax capital gain payable by the seller of the shares in the event of a profit result.

Income tax advances

All income tax payers who are legal persons or single owner, whose effective tax rate is less than or equal to 1.5 %, should pay a monthly payment of income tax of fiscal year equivalent to 1.5 % of gross income of each month. However, companies whose tax paid in the previous fiscal year represents a higher effective rate to 1.5 % of the gross income of the same fiscal year, paid monthly in advance one twelfth of the tax paid for the last fiscal year stated.

Individuals and undivided estates who receive income from the exercise of liberal professions must pay 3 advances on the basis of 100% of the tax paid the previous fiscal year, as follows: 50 % at six months, 30% in the ninth month and 20 % in the twelfth month. Individuals whose incomes come from commercial and industrial activities pay monthly in advance 1.5% of gross income each month.

Simple estimation scheme or Simplified Regime

Natural persons or single owner residing in the country, which do not keep organized accountability and whose income are exempt from sales tax on transfer goods by more than 50% of Industrialized Goods and Services (ITBIS) or better known as VAT, or in Services where ITBIS is retained 100%, may choose to hold a fixed amount of forty percent (40%) of their taxable income, in order to determine their net income tax if their gross income does not exceed RD$6,000,000. This net income will benefit from the annual tax exemption (previously mentioned in the chart) for purposes of applying the tax rate. This annual statement must be filed no later than the last working day of February each year. The resulting applicable tax will be payable in two equal installments, the first one in the same deadline affidavit and the second, the last working day of August of the same year.

Tax on the Transfer of Industrialized Goods and Services (VAT)

This tax is levied on the import and transfer of industrialized goods, as well as the provision and location of services.

In the case of the transfer of goods based on the net transfer price plus accessory services. Import of manufactured goods, on the basis of CIF (Cost, Insurance and Freight) of assets over rates. For the provision and location of services, based on the value of the service. The export of goods and services are exempt from tax, as long as it complies with the conditions set out in the Code.

Natural and legal persons (domestic or foreign) that make

transfers and imports of manufactured goods or services are

responsible of the payment of this tax. Public and private

companies that conduct or not

taxable activities, are responsible of the obligation to make

withholdings from ITBIS involved in the services that are provided

to them by individuals, and they pay benefits for liberal

professional services and movable rental assets to other companies,

profit or non profit.

Law No. 253-12 provides taxable transfer applicable for rate transfer and/or provided services of (i) 18% for 2013 and 2014; and (ii) 16 % from 2015; and the planned reduction from 2015, would apply to the extent that would allow achieving and maintaining the tax burden by 2015, according to Article 26 of Law No. 01-12 of the National Development Strategy. Similarly, they reduced rates ranging from 8% to 16% from 2013 to 2016 respectively for certain industrialized goods ITBIS (these were established, and without the statement being limiting, are yogurts, butter, coffee, oils ,margarine, sugar, cocoa).

The tax rate is 18% on the price of the transfer of taxable goods and/or services. In addition, from 2015, the new reduced rate of 13% applicable to the above goods was established.

The declaration and payment of this tax shall be made during the first 20 days of the month following the declared (ex: The month of January must be submitted and paid before February 20) period. The import is paid together with the customs duties or taxes.

Some goods and services are exempted from ITBIS.

Selective Consumption Tax (ISC)

This tax is levied on the transfer of some national manufacturing products, importation and the provision of telecommunications services, insurance and payments made with checks by financial entities and those made through wire transfers. Some examples of products subject to this tax are automobiles, jewelry, alcohol and tobacco products.

The tax rate varies depending on the goods or services to which you are applying, among which we can cite:

- Tobacco products, specific amounts depending on the number of cigarette packs and 130% for cigars.

- Telecommunication services, 10%

- Insurance services in general, 16%

- Checks and wire transfers, 1.5 % per thousand (0.0015)

Real estate Property Tax, Sumptuary Housing and Non-constructed Urban Plots (IPI/IVSS)

Law No. 18-88 establishes an annual tax called Real estate Property Tax, Sumptuary Housing and Urban Lots not built (IPI/IVSS). The IPI/VSS extends only to individuals, and is applied on capital total property of individuals, which will be determined on the value established by the Directorate General of National Land Survey (from 2012).

The assets burdened with this tax is as follows:

a) Consists of properties made for housing for natural persons, whose value as a whole, including the place where they are built, exceeds RD$6,500,000.00.

b) Consists of urban Lots and non-residential properties, including those intended for commercial, industrial and professionals, belonging to natural persons whose combined value exceeds RD $ 6,500,000.00.

c) Comprises the combination of a) and b), which on the whole exceeds six million five hundred thousand pesos RD$6,500,000.00.

The amounts of a), b) and c) should be annually adjusted by the inflation published by the Central Bank of the Dominican Republic. This late 2015, the DGII will consider RD$6,752,200 as value.

It should be noted that this is imposed only for plots and buildings of the encumbered property and therefore it shall not form part of your taxable income rural land dedicated to the farm, nor the furniture, equipment, machinery, plants electrical, furniture and other goods that are within the encumbered property.

Similarly, those dwellings are exempt whose owner has reached age 65, provided that such property has not been transferred ownership in the last 15 years and its owner only owns the dwelling and real estate; and the retired people and foreign pensioners from its foreign sources by 50 %.

The Affidavit must be annually submitted within the first 60 days of the year. Two semi-annual fees perform the IPI/IVSS payment, the first within 10 days from the date of the deadline for submission of the said Affidavit and the second in September.

Tax assets (ISA)

This tax is levied on the total value of the assets of legal entities or individuals with single owner businesses, including real estate listed on the balance sheet of the taxpayer (not adjusted for inflation and after applying the deduction for depreciation, amortization and reserves for doubtful accounts). Not part of taxable assets equity investments in other legal entities, the land located in rural areas, real estate by nature destined for farms and developed or advances taxes.

ISA rate applicable is 1% based on the total value of taxable assets, and settlement is made in the same affidavit for the ISR submitted by the taxpayer. The payment shall be made in two (2) installments, the first in the same deadline for the payment of income tax, and the second within six (6) months from the expiration of the first installment.

Law No.253-12 contemplated a reduction in the rate of the ISA 0.5% from the 2015 period similar to ITBIS; it has not been effective on the basis of not achieving the goal of tax burden. Similarly, Law No. 253-12 provided for the elimination of the ISA as of fiscal year 2016 and that, once removed the ISA, the IPI / IVSS provisions of Law No. 18-88 will be applied to the property of legal or moral persons. However, it has not been either effective.

Inheritance tax

Law 2569 of December 4, 1950, as amended creates tax on any transfer of movable and immovable property by inheritance or donation. In the case of donations, the tax must be paid by the favored of that donation and fall on the value of donated goods. Tax payment successions meanwhile, the heirs, successors and assigns of the deceased will be charged.

The payable rate for successions is 3%, calculated on successor mass, after making the deductions. Donations meanwhile, from Law No. 253-12, is subject to a tax equivalent to the income tax rate of legal persons in effect at the time of donation, with the rate to be considered from 2015 27% applicable to the value of donated goods.

In order to settle the tax on the inheritance, you must present the affidavit of inheritance within 90 days elapsed after the death, with possible extension of up to 105 days in cases where the successors have been unable to complete the documentation required for the record. The donation tax must be paid within 10 days after completion of the respective grant, is not entitled to overtime.

Collaboration from: Ana Taveras, Farah Raful

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.