- within Tax, Real Estate and Construction and Family and Matrimonial topic(s)

- with readers working within the Aerospace & Defence industries

On December 22, 2017, the Tax Cuts and Jobs Act 2017 ("T.C.J.A.")1 introduced the foreign derived intangible income ("F.D.I.I.") regime into the Code. This tax favorable regime is limited to entities taxed as U.S. corporations.

In essence, F.D.I.I. constitutes a taxable U.S. corporation's income from specified export activities. More precisely, the F.D.I.I. regime allows for a reduced corporate tax on hypothetical intangible income used in a U.S. business in exploiting foreign markets. Under the F.D.I.I. rules, the hypothetical intangible income is reduced by a 37.5% deduction, which is intended to result in an effective Federal corporate income tax rate of 13.125% for a U.S. corporation.2 It is important to note that, due to the way F.D.I.I. is computed, the effective rate on export income is generally higher than 13.125% under this rule.

On March 6, the I.R.S. published comprehensive proposed regulations addressing F.D.I.I.3 They contain a substantial number of examples. If adopted in final version, the proposed regulations would be applicable to taxable years ending on or after March 4, 2019.4

THE F.D.I.I. COMPUTATION – A BRIEF RECAP

To determine its F.D.I.I. deduction, a domestic corporation must first determine its F.D.I.I. amount.

This determination is made through a multistep process that involves the following calculations:

- Deduction eligible income ("D.E.I.")

- Foreign derived deduction eligible income ("F.D.D.E.I.")

- Qualified business asset investment ("Q.B.A.I.")

- Deemed intangible Income ("D.I.I.")5

- F.D.I.I.

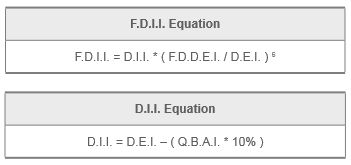

The formula to determine F.D.I.I. can best be summarized by the following equations:

A key concept under F.D.I.I. is the computation of a U.S. corporation's hypothetical intangible income, known as D.E.I. The computation of D.E.I. begins with the gross income of the domestic corporation, from which the following income items are removed

- Subpart F Income derived from controlled foreign corporations ("C.F.C.'s") and included in taxable income under Code §951(a)(1)

- Amounts of global derived intangible income ("G.I.L.T.I.") derived from C.F.C.'s and included in taxable income under Code §951A

- Financial services income of the corporation – typically limited to financial institutions

- Any dividend received from a C.F.C.7

- Domestic oil and gas extraction income of the corporation

- Foreign branch income8

D.E.I. is then reduced by a deemed 10% return on the corporation's Q.B.A.I.9 Q.B.A.I. is measured by reference to the U.S. corporation's average aggregate adjusted bases in depreciable tangible property used in the production of D.E.I. The result is then prorated in the ratio export-related D.E.I. (i.e., F.D.D.E.I.) bears to total D.E.I.

Footnotes

1 Public Law 115-97.

2 For tax years beginning after December 31, 2025, the allowable deduction is decreased, and the effective tax rate will be 16.406% (Code §250(a)(3)(A)).

3 I.R.S.; Deduction for Foreign-Derived Intangible Income and Global Intangible Low-Taxed Income, 84 Fed. Reg. 8188 (March 6, 2019).

4 Prop. Treas. Reg. §1.250-1(b).

5 See in detail, "A New Tax Regime for C.F.C.'s: Who Is G.I.L.T.I.?" Insights 5, no. 1 (2018), Components of the F.D.I.I. Provision.

6 The ratio F.D.D.E.I. to D.E.I. is also referred to as foreign derived ratio ("F.D.R.").

7 Under the definition as expanded by the T.C.J.A., a non-U.S. corporation is a C.F.C. if more than 50% of the voting power or value of all shares outstanding are owned by one or more U.S. Shareholders. A U.S. person is a U.S. Shareholder if it owns at least 10% of the voting power or value of all outstanding shares of the foreign corporation.

8 Code §250(b)(3)(A)(i)(VI)

9 Code §250(b)(2)(A).

10 Code §250(b)(4).

11 Code §250(b)(5). Specific rules exist for non-U.S. related-party transactions.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]