- within Criminal Law topic(s)

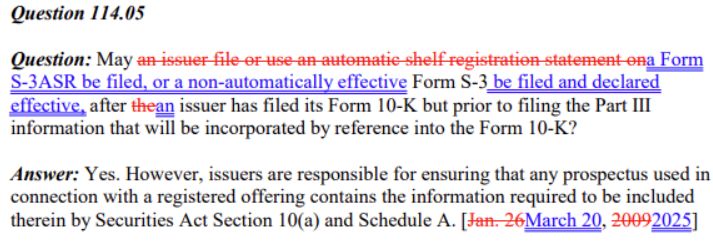

On March 20, 2025, the staff of the SEC's Division of Corporation Finance issued revised Securities Act Forms C&DI Question 114.05 indicating that non-automatically effective registration statements on Form S-3 may now be filed and declared effective after an issuer has filed its Form 10-K but prior to filing its Part III information that will be incorporated by reference into the Form 10-K.

The staff also withdrew Securities Act Forms C&DI Question 123.01 that previously stated that in order to have a complete Section 10(a) prospectus, a registrant filing a non-automatically effective Form S-3 had to either file its definitive proxy statement before the Form S-3 was declared effective or include Part III information in its 10-K.

The SEC's comparison to the prior version of Securities Act Forms C&DI Question 114.05 highlights these changes:

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.