With ongoing supply chain issues, legislative challenges in Washington and a rising interest rate environment, many renewable energy investors prepared for a cooler start to 2022. Optimism grew as the year progressed, with President Biden instituting a two-year pause1 on the implementation of tariffs on solar panels from Southeast Asia and the passage of the landmark Inflation Reduction Act ("IRA"),2 providing $370 billion in tax credits for renewable energy projects. Navigating through these factors, 2022 M&A volume remained largely consistent with 2021 and included some notable transactions, such as RWE's acquisition of Con Edison's Clean Energy Businesses for $6.8 billion and Duke Energy's planned sale of its Commercial Renewable Business.3

Established renewable technologies represented the highest proportion of 2022 M&A activity with demand for renewable development platforms remaining strong. The pursuit of financial returns and the opportunity to quickly scale continued to drive investments in platforms plays. Notable transactions included Macquarie Green Investment Group's acquisition of Treaty Oak4and Blackrock's acquisition of Jupiter Power. Additionally, renewable investors not only continued to move up the value chain in search of financial returns but also diversified5 into emerging subsectors, such as Renewable Natural Gas ("RNG"), alternative fuels and standalone storage. Notably, RNG transaction volume more than doubled in 2022, with transactions such as BP acquiring Archaea Energy for $4.1 billion leading the charge.

As we move through 2023, we expect deal flow to remain strong as developers look to monetize opportunities and benefits driven by the IRA. Creative solutions and investor flexibility will be required as persistent supply-chain issues, long interconnection queues and high inflation remain. Furthermore, the rising interest rate environment will likely cause downward pricing pressure on 2023 asset sales. To address these challenges, we expect renewable energy investors to seek deals at the right price and move towards emerging technologies and subsectors to achieve an acceptable risk-adjusted rate of return. Furthermore, corporates may more closely examine the divestiture of non-core assets as a path to free up cash flow for strategic acquisitions or other operational drivers.

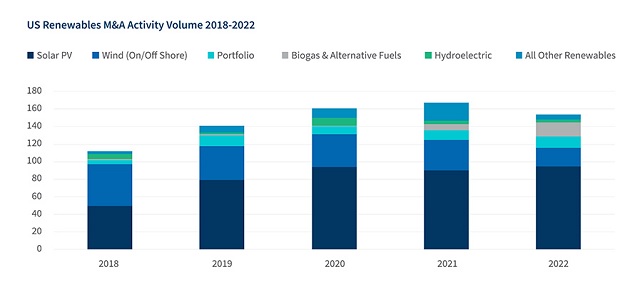

US Renewables M&A Activity Volume 2018-2022

Source: Infralogic

Key 2022 Trends

Renewable Fuels

RNG and alternative fuels received increased attention from investors in 2022, with headline developer-deals bringing new validity to a historically niche area. Energy majors led the way with landmark deals, including BP acquiring Archaea Energy and Chevron acquiring Renewable Energy Group. Both acquirers cited the need to reduce the average lifecycle carbon emissions of their product portfolio as key to their transaction rationale. With these new platforms, BP and Chevron can introduce low carbon alternatives to their more carbon-intensive energy portfolio, helping reduce their overall environmental impact.

Institutional investors followed closely behind with another eleven RNG platform transactions during 2022, including Kinder Morgan's acquisition of North American Natural Resources and CIM Group's acquisition of Terreva Renewables. We view this trend as driven by institutional investors looking up the yield-curve into emerging technologies to find acceptable risk-adjusted returns in a high inflation environment. RNG platforms are being considered as an attractive alternative to traditional solar and wind assets with the potential for higher returns and a faster development timeline than that of other renewables technologies. The IRA is likely to help de-risk and further boost the return profile of RNG developers with the expanded Investment Tax Credit ("ITC") eligibility afforded to qualified RNG projects. The renewal of the alternative fuel tax credit program should also provide higher revenue certainty for RNG developers selling fuel into the transportation market.

Notable Platform Deals Continue

In our M&A outlook for 2022, we anticipated that — while many of the marquee developers were acquired in 2021 — platform-deal activity would continue throughout 2022 as investors continued to seek out platforms as a potentially higher return alternative to the project market. We saw this trend shift from household name utility-scale developers to i) distributed energy within the commercial, industrial and community platforms and ii) standalone and hybrid storage-focused developers. And not surprisingly, financial buyers continued to be at the forefront, with Axium Infrastructure, Blackrock, Brookfield Renewable and Macquarie among other active financial buyers leading the charge. While majority stake acquisitions in the platform space are most common, we saw sizable equity investments in well-known names, including Generate Capital's into Pine Gate Renewables6 and Silicon Ranch's7 equity raise from Manulife.

We view the platform acquisition trend as being driven by several factors — key amongst these, rapid access to high-quality development pipelines and experienced management teams with successful track records (as further detailed in our Due Diligence Considerations for Investing in the Energy Transition Sparknote8 co-authored with DNV GL). The case for platform acquisitions has been reinforced by the extremely competitive environment for standalone renewable projects and more recently by the added complexity of supply-chain constraints and volatility in inflation and interest rates. All of which has increased the uncertainty associated with project valuations and implied returns.

Selected Notable 2022 Platform Acquisitions Are Outlined in the Table Below

| TARGET COMPANY | BUYER | SELLER | SUMMARY |

|---|---|---|---|

|

EQT Infrastructure |

Stonepeak Partners LP |

EQT Infrastructure to acquire Madison Energy Investments, a distributed-generation platform focused on solar and energy storage projects for commercial and industrial ("C&I") and community projects. |

|

|

Macquarie Green Investment Group |

Treaty Oak Clean Energy |

Macquarie Green Investment Group acquired Treaty Oak, a clean-energy platform focused on utility-scale solar plus storage projects in the United States. |

|

|

Blackrock Alternatives |

EnCap Investments |

Blackrock acquired Jupiter Power, a developer and owner of standalone, utility-scale-battery energy-storage systems. |

|

|

Aspen Power Partners |

PPL Corp. |

After a $350 million investment from Carlyle, Aspen Power Partners acquired Safari Energy, a distributed solar platform focused on C&I projects. |

|

|

Brookfield Renewable |

Scout Clean Energy |

Brookfield's $1 billion acquisition of Scout Clean Energy includes a portfolio of 1.2 GW of operating wind assets and a pipeline of >22 GW of wind, solar and storage projects across 24 U.S. states. |

|

|

Brookfield Renewable |

Standard Solar |

Brookfield's $540 million acquisition of Standard Solar, a C&I and community distributed solar platform, includes 500 MW of operating and under construction assets and a development pipeline of ~2 GW. |

|

|

Enbridge |

Tri Global Energy |

Enbridge acquired Tri Global Energy, a wind, solar and energy-storage developer with a development portfolio of >7 GW of wind and solar projects. |

|

|

Axium Infrastructure |

BlueWave |

Axium acquired BlueWave, a development platform focused on community-scale solar and solar energy-storage projects. |

Continued Investment in the U.S. Energy Transition

In a theme similar to that highlighted last year, energy majors made significant investments in renewables as part of a larger effort to expand into lower carbon alternatives. Notable activity included:

- BP North America agreed9 to purchase EDF Energy Services in order to expand BP's presence in C&I retail power and gas;

- TotalEnergies announced a definitive agreement10 to acquire SunPower's Camp;&I division for $250 million;

- Attentive Energy won11 a maritime lease to develop >3 GW of offshore wind projects in the New York Bight and, in conjunction with this, Total Energies acquired EnBW's stake in the Attentive Energy joint venture;

- Equinor acquired12 Charlottesville-based East Point Energy, which owned a 4.1 GW pipeline of early- to-mid-stage battery-storage projects.

There is also evidence of the early adoption of emerging technologies such as blue and green hydrogen and carbon capture and storage ("CCUS"). This included an uptick in M&A activity and capital raises in these developing technologies, including CCUS player LanzaTech entering into a merger agreement with AMCI.13 We also observed sizable equity raises from hydrogen players Intersect Power14 and Monolith.15 In all three cases, we see industry leaders raising significant amounts of capital in preparation for further ramping operations in 2023. We expect an even greater focus from investors headed into 2023, given wider technology adoption, maturing end-use markets and investors' focus on emerging sectors.

Electrification Drives M&A Activity

The electrification of buildings and homes, the proliferation of EVs and the need for battery storage to support the intermittency driven by wider renewables-deployment is also driving M&A activity. Investors and strategic players alike are capitalizing on the opportunity. Most notably, home electrification saw transformative deals in 2022. Smart homes requiring increased levels of connectivity are driving strategic acquisitions with cross-segment synergies. NRG has entered in to a definitive agreement for the acquisition of Vivint Smart Home for $2.8 billion16 in December 2022. Vivint has cemented itself as a leader in smart-home technology and has recently integrated residential solar solutions to increase its offering. Through this acquisition, NRG plans to capitalize on a holistic smart-home service offering to its customers. Other companies, including Schneider Electric17 and XL Fleet,18 also completed 2022 acquisitions to expand offerings in the rooftop solar and electrified homes spaces.

Lastly, the growth in adoption of EVs by individual consumers and vehicle fleets yielded significant M&A activity in 2022, with a key trend being the acquisition of charging suppliers. EV charging solutions providers — such as EV Connect,19 InCharge Energy20 and SemaConnect21 — were all acquired by strategic players. The latter was the most notable as SemaConnect was acquired by one of its main competitors, Blink. Overall, it demonstrates the growing consolidation in a highly fragmented market that's reaching maturity as the adoption of EVs' increases.

Outlook for 2023

We begin 2023 with a strong sense of optimism, as increased corporate commitment to decarbonization, accelerated carbon reduction goals from local, state, and federal governments and the passage of the IRA providing over $370 billion in incentives over a 10-year term all support the prospect of strong M&A activity. Only hindsight will tell, but 2023 may be described as the year when optimism transitions to practical application. While market participants begin to understand and take advantage of these favorable conditions, they must also confront and adapt to the challenges associated with supply chain issues, demand imbalances, a higher cost of capital, and human resource constraints.

Some of the key themes for the year ahead include:

The IRA: Moving from Euphoria to Reality

We anticipate that it will take 4 to 6 months for guidance to be issued on specific aspects of the IRA. Developers and asset owners will require time to assess the relative value to their investments and to implement financing plans that take advantage of these incentives. Importantly, additional time will be needed for newly qualified tax equity markets to price and receive investor interest. With patience, we anticipate strong M&A activity in traditional renewable assets, platforms and emerging technologies trending toward the second half of 2023 and into 2024 as greater clarity and increased value creation are established.

Supply Challenges

Ongoing supply shortages relating to solar modules, transformers, and other critical components across various technologies continue to slow and delay project construction. Supply-chain issues, Uyghur Forced Labor Prevention Act ("UFPLA") restrictions, and resource scarcity will continue to hinder growth in the near term for the sector. We also anticipate additional supply constraints relating to tax-equity dollars and human capital. With the eligibility expansion under the IRA of the ITC and PTC and the potential for increased tax equity investments per project, the demand for tax-credit investors will most certainly outstrip the current supply. We anticipate this short supply of tax-equity funding to create challenges for many developers, especially for middle-market players and developers in emerging subsectors. While potentially challenging to source, higher tax-equity eligibility will increase returns and potentially attract new participants over time.

Another factor plaguing the renewable-energy sector is the demand for trained professionals who can quickly move into critical positions inside new or expanding renewable platforms. Be it technicians, engineers, contractors or financiers, scaling such businesses will continue to be challenged by labor shortages.

Market Expansion

With the support of the IRA and other federal and state incentives, we anticipate accelerated growth in waste-to-energy, RNG, standalone battery storage, clean hydrogen and carbon sequestration. While the bulk of M&A and capital-market activity will continue around traditional solar and wind assets, a significant amount of capital is moving into promising technologies that offer federal tax incentives, scale, different revenue profiles and strong long-term financial returns. For example, several infrastructure funds and private equity investors have recently become comfortable with the technology, discrete nature and waste issues relating to the anaerobic digestion of food and dairy waste into energy. This "comfort" greenlights investment dollars through an investment thesis containing scale, certainty, and attractive returns.

With the ability to take advantage of the ITC, standalone battery storage, already exhibiting strong growth, is poised to reach a significantly higher scale as our needs for electrical storage continue to grow. While still in the earlier stages of commercial application, both clean hydrogen and carbon-capture projects are attracting new investors. With more projects coming online in 2023, investors will be quick to fill this space and take on the risk and potential rewards of these promising technologies.

Although 2022 was a volatile year across the United States in both M&A and capital-markets activity, renewable energy fared well because of the growing interest in the energy transition, the IRA accelerating the deployment of capital and the continued attractive investment opportunities that fit an ESG investment profile. While 2023 may bring increased cost of capital as the Federal Reserve stays proactive against inflationary factors, we anticipate the renewable energy sector to benefit from the aforementioned tailwinds, leading to a robust year for transactions.

How FTI Consulting's Power, Renewables & Energy Transition Team Can Help

FTI Consulting's Power, Renewables & Energy Transition professionals have functional expertise across the life cycle of renewable energy participants. Our seasoned team provides tailored services for strategic and financial investors, creditors and corporates and has deep experience with renewable energy platforms, projects and portfolios.

Through our wholly owned investment banking subsidiary, FTI Capital Advisors, we provide tactical strategic advice, buy- and sell-side advisory and capital-raising services. Our seasoned investment bankers have significant transactional experience in developing solutions and executing assignments in the U.S. capital markets for a wide variety of clients. As an independent investment bank, we are free of conflicts, enabling us to provide clients with unbiased and uncompromising advice and execution capabilities, besides being uniquely supported by a broad team of industry experts servicing consulting clients across the renewables value chain.

FTI Consulting team members have developed and apply best practices in strategic market entry, transaction advisory, due diligence, and operational transformation. We assist leading strategic and financial investors across all stages of the transaction life cycle, including strategy, diligence, and the pre-sign, sign-to-close, and post-close phases of merger integration and carve-out transactions. Our team customizes the scope of our engagement models to provide solutions tailored to our clients' needs, from full-scale transaction execution to specific PMO or functional-subject-matter expertise, always working in partnership with leadership and key stakeholders.

M&A Strategy

- Strategic Alternatives

- Cap. Structure Alternatives

- Market Cap. Alternatives

- Value Enhancement

- Tax Optimization

Due Diligence

- Financial

- Tax

- Commercial

- Operational

- Technical

Transaction Execution

- Negotiation & Structuring

- Execution Advisory

- Market to Investors

- Deal Close Support

Transition Planning

- Integration Strategies

- Synergy

- Day 1 Readiness Planning

- Integration Management Office

Target Identification

- Buy-Side Services

- Prospect Identification

- Strategic Fit Analysis

- Valuation Advisory

Divestiture & Carve-out

- Buy-and-Sell-Side Carve-outs

- Carve-out Due Diligence

- TSA Development

- Capital Raise Services

- Exit Strategy

- Valuation Ranges

Merger Integration

- Due Diligence

- Integration Plan Development and Execution

- Synergy Assessment and Tracking

- Post-Close Support and Busines Transformation

Footnotes

1: The White House. Declaration of Emergency and Authorization for Temporary Extensions of Time and Duty-Free Importation of Solar Cells and Modules from Southeast Asia. June 6, 2022. Link

2: The White House. Inflation Reduction Act Guidebook. Link

3: RWE. RWE agrees to acquire Con Edison Clean Energy Businesses, Inc. Link

4: Macquarie. Macquarie Asset Management's Green Investment Group Acquires Treaty Oak Clean Energy. December 2022. Link

5: Encap Investments. Encap Investments Sells Jupiter Power To Blackrock. Link

6: Business Wire. Generate Capital Provides Pine Gate Renewables with $500 Million. June 2022. Link

7: Silicon Ranch. Silicon Ranch Raises $775 Million in Equity Funding. January 2022. Link

8: FTI Consulting, Inc. Due Diligence Considerations for Investing in the Energy Transition. Link

9: BP. bp North America agrees to purchase EDF Energy Services. September 2022. Link

10: TotalEnergies. Total Energies to Acquire SunPower's Commercial & Industrial Solar Business. February, 2022. Link

11: TotalEnergies. United-States: Total Energies Wins Maritime Lease to Develop a 3 GW+ Offshore Wind Farm. February, 2022. Link

12: Equinor. Equinor acquires energy storage developer in the US. July, 2022. Link

13: Lanzatech. Lanzatech NZ, Inc., a market-leading innovator in carbon capture & transformation, to go public through business combination with AMCI Acquisition Corp. II. March, 2022. Link

14: Renewable Energy World. Intersect Power raises $750m to develop renewable energy portfolio. June, 2022. Link

15: Monolith. Monolith raises more than $300 million in latest funding round. July, 2022. Link

16: NRG Energy. NRG Energy, Inc. to Acquire Vivint Smart Home, Inc. December, 2022. Link

17: EnergySage. EnergySage Acquired by Schneider Electric to Accelerate a Shared Global Vision of Electrifying the Future. February, 2022. Link

18: Spruce Power. XL Fleet Completes Transformational Acquisition of Spruce Power. September, 2022. Link

19: EV Connect. EV Connect Acquired by Schneider Electric to Accelerate EV Revolution. June, 2022. Link

20: ABB. ABB acquires controlling interest in InCharge Energy, strengthening its EV charging solutions in the U.S. January, 2022. Link

21: Blink Charging. Blink Charging Announces Closing of the Acquisition of EV Charging Leader SemaConnect. June, 2022. Link

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.