- within Insolvency/Bankruptcy/Re-Structuring, Coronavirus (COVID-19) and Cannabis & Hemp topic(s)

Previously published by May 2012 issue of the ABI Committee News

By definition, a preferential transfer is any "transfer" to or for the benefit of the creditor during the 90-day period counting backwards from the bankruptcy filing date. A "transfer" is anything of value, tangible or not, that the bankrupt customer gave any creditor or gave up for the benefit of a creditor for any reason.

According to § 547 of the Bankruptcy Code, after filing for bankruptcy the debtor may recover transfers occurring in the 90 days prior to the filing, provided that the transfers meet certain criteria. Conversely, the creditor has several defenses to defend against preference claims in order to retain transfers previously received. One such defense frequently employed by creditors has been the industry ordinary-course defense, which often involves reference to public sources of industry information in order to establish that the transfers were ordinary based on observed payment practices in the relevant industry. However, depending on the information available, data obtained directly from the creditor or debtor relating to historical accounts payable transactions, accounts receivable transactions and other indications of payment practices may provide an alternative or complement to defining industry ordinary course for payment practices.

Ordinary in the Industry: Objective Test

Comparisons to industry standards are often used to establish a reasonable basis for ordinary course. As stated by Credit Research Foundation, when establishing the industry ordinary-course defense, "although the industry standard does not require a creditor to establish the existence of a uniform set of business terms, it does require evidence of a prevailing practice among similarly situated members of the industry facing the same or similar problems."1

Many factors may impact the court's ruling on whether the alleged preferential transfers occurred within industry "ordinary course." In Smith Road Furniture, the court made a special point that "the more established the trade relationship between the parties, the more that a creditor will be permitted to deviate from the industry standard and still qualify for the ordinary-course-of-business exception. However, it is the creditor's burden to establish the industry payment standard."2

Sources of Data Utilized to Define Industry Ordinary Course

When defining industry ordinary course, the creditor will often refer to sources of public information pertaining to payment days, days sales outstanding (DSO)3 and days payable outstanding (DPO).4 Such sources of information may include Capital IQ, the Risk Management Association, Dunn & Bradstreet reports, and information from the Credit Research Foundation.

Limitations of Common Industry Publications

While the common industry sources for payment and credit information mentioned can be helpful, they can also pose certain limitations. Certain sources have been provided information anonymously and the information may or may not have been audited or verified for accuracy or consistency. Further, these sources of information do not provide information in a format that is searchable, sortable, or otherwise well suited for analysis beyond the quartile metrics stated in the publication. For example, these sources of information will not allow an analysis of distribution of industry conduct; rather, they will frequently only provide a 25th percentile, median (50th percentile) and 75th percentile. The remaining distribution on either side of these percentiles can still be considered ordinary in an industry but can be difficult to assess without significant additional information.

Most public sources of information are also only published on a periodic basis, which can limit the degree of analysis that can be performed in industries or economic circumstances that are fluctuating over a shorter period. As such, while these sources provide an indication of industry standards, if more detailed information is available from the creditor or debtor, it should be reviewed and analyzed to assist in further understanding ordinary conduct in an industry.

Using Company Data to Establish Industry Ordinary Course

Given the limitations that are sometimes observed with industry data, it is often relevant to consider records from the creditor and debtor detailing receivables and payables transactions and balances specific to their customer and supplier or vendor base. Such information can be utilized as an additional proxy for ordinary course with respect to payment behavior between suppliers and customers in the industry. Similar to an analysis giving primary consideration to public sources of information, an analysis of industry ordinary course based on company data will often require consideration of key metrics relating to payment practices.

Use of Creditor Data

The analysis of the creditor's data will often start with an identification of the customers most relevant for defining the appropriate industry. For example, if the creditor is a supplier of electronic components, it may supply such products to both the automotive and aerospace industries. It may be necessary to identify those customers within the creditor's accounts receivable and payment receipt information that are most similar to the debtor.

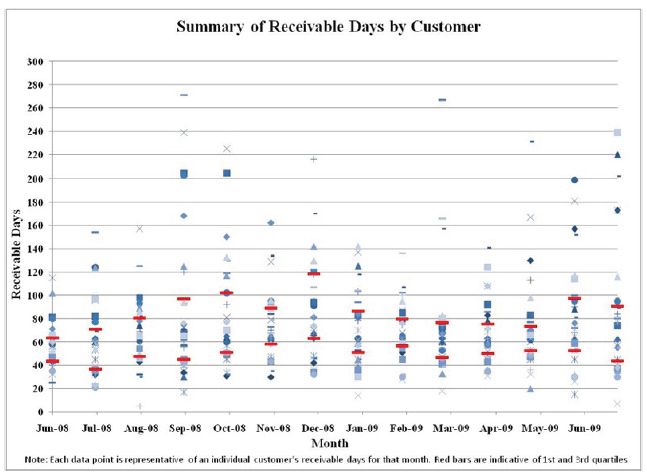

Once the relevant customer data is identified, it is then necessary to analyze the data based on several common payment metrics such as DSO or payment days (giving consideration to any fluctuation in payment terms offered to individual customers).5 For example, if information is obtained from the creditor detailing the monthly aging of accounts receivable for each customer in total, such data may be utilized to calculate average DSO. Alternatively, if information is available regarding individual invoices outstanding for each month, actual DSO may be calculated for each invoice. Further, if information is available regarding when payments were made on individual invoices, such data can be utilized to calculate actual payment days for these invoices.

As indicated in the charts below, this analysis provides the opportunity to evaluate several factors that may not be transparent in the use of common industry publications. This approach facilitates an investigation of how overall payment trends may have changed over time for the industry, how the distribution of payment practices (how flat or tall the bell curve is) has changed over time and whether any industry subgroup appears to have unique payment practices that should be further investigated. In general, this approach, if available, can provide for a more precise analysis and one more capable of identifying an "industry" of companies that were similarly situated to the creditor and debtor at the time of the transfers.

Similar to the analyses that may be performed based on creditor data, it is also often relevant to consider historical payables and payment information specific to the debtor and its relationship with its suppliers.

How the Courts Are Considering Industry Ordinary Course

The dynamics of preference litigation began to shift after the decoupling of the objective and subjective tests under the amended § 547(c)(2). There seemingly has been a tide of defendants willing to assert the industry ordinary-course defense without submitting to initial settlement pressures, which is likely the function of two things. First, the decoupling of the objective and subjective tests has made it less expensive for defendants because, for example, experts hired to assess ordinary course only need to focus on one prong of the test rather than two. Second, now being able to consider solely the objective test, courts are in a better position to review the objective facts (rather than subjective), making it easier to determine whether there are questions of fact. As a consequence, this gave defendants a higher degree of confidence that their ordinary course defense would be adjudicated in their favor.

An interesting case in this regard is In re American Camshaft Specialties Inc.6 In this case, the chapter 7 trustee brought a preference action seeking to recover preferential payments in the amount of $3.1 million made by the debtor to the supplier for steel bar stock. The supplier asserted both the objective and subjective ordinary-course defense under § 547(c)(2)(A) and (B) and a new-value defense. The supplier moved for summary judgment on those defenses. The court granted the motion based on the ordinary-course defenses, making it unnecessary for the court to rule on the new-value defense. In addressing specifically the industry ordinary-course defense, the court applied the Sixth Circuit standard under which "courts analyze whether the particular transaction in question comports with the standard conduct of business within the industry."7 The Sixth Circuit has also held that "ordinary business terms" means that the transaction was not so unusual to render it an aberration in the relevant industry.8 The court noted that both experts went to the same sources for the same industry for comparison data.9 After consideration of the comparison data and applying that data to the facts, the court concluded there were no genuine issues of material fact regarding whether the challenged payments were made according to ordinary business terms.10 The court granted summary judgment in favor of the defendant on the industry ordinary-course defense.11 The takeaway is that when the industry ordinary-course defense can be thoroughly investigated early in the case, the odds of a court being able to grant full or partial summary judgment for the defendant should increase.

Conclusion

Comparisons to industry standards are often used to establish a reasonable basis for ordinary course. Establishing the industry ordinary-course defense requires evidence of a "prevailing practice among similarly situated members of the industry facing the same or similar problems."12 However, due to the limitations of certain publicly available sources of information, it is often relevant to consider records from the creditor and debtor detailing receivables and payables transactions and balances. Such information can be utilized as an additional proxy for industry ordinary course.

Footnotes

1. Scott Blakeley and Terry Callahan, "In Defense of a Preference," The Credit Research Foundation, 2004.

2. Scott Blakeley and Terry Callahan, "In Defense of a Preference," The Credit Research Foundation, 2004; In re Smith Road Furniture Inc., 304 B.R. 793 (Bankr. S.D. Ohio 2003).

3. This metric is often referred to as accounts receivable days outstanding (ARDO). These metrics are not appropriate as direct comparison to payment days on individual invoices. Such metrics only measure the company's receivables in aggregate and do not provide payment days specific to individual invoices, which are often in dispute in the preference action. However, these metrics may be utilized as a reasonable proxy for industry ordinary course.

4. This metric is often referred to as accounts payable days outstanding (APDO).

5. This metric is typically calculated based on the time from the invoice date to payment date.

6. 444 B.R. 347 (E.D. Mich. Bankr. 2011)

7. Id. at 363

8. Id.

9. Id. at 365.

10. Id. at 366.

11. Id.

12. Scott Blakeley and Terry Callahan, "In Defense of a Preference," The Credit Research Foundation, 2004.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.