- within Real Estate and Construction topic(s)

As the market continues to evolve with the dynamics of sustainable finance legislation, managers are often facing challenges in how to best navigate competing investor demand and sentiment on environmental, social, and governance (ESG) preferences. More specifically, changing investor demand is requiring managers to look closely at whether "anti-ESG" preferences can be reconciled with the requirements in the EU Sustainable Finance Disclosure Regulation (SFDR), especially those in Article 8.

Article 8 applies to a fund "which promotes, among other characteristics, environmental or social characteristics, or a combination of those characteristics, provided that the companies in which the investments are made follow good governance practices". On its face, this requirement is at odds with those of investors, especially some US public authorities, for whom the promotion of ESG characteristics and practices should not be given any priority or, indeed, should be actively avoided.

However, an investor may say that it will invest in a fund whose investment mandate does not allow the fund manager to give non-pecuniary (i.e. ESG) factors priority over pecuniary (i.e. investment returns) ones. In this case, the fund could be one that promotes, among other characteristics, environmental or social characteristics, albeit one that prioritises a financial return. Such a fund could therefore reconcile some "anti-ESG" positions with Article 8. This is different to the case where an investor says that it will only invest in a fund whose investment mandate does not allow the fund manager to consider non-pecuniary factors at all. Clearly, such a fund would not be one that promotes, among other characteristics and practices, environmental or social characteristics and, therefore, would be contrary to Article 8. Another (less controversial) approach that we are seeing is managers focusing capital raising in key jurisdictions and geographies where investors welcome, if not actively seek, funds that promote ESG characteristics, and managers accepting that approaching "anti-ESG" investors in other jurisdictions and geographies will not be possible or worthwhile. Managers have also attempted to admit "anti-ESG" investors in Article 8 funds by granting them excuse rights; however, this approach has seen only limited success.

Ultimately, a manager will have to understand what a potential investor is really looking for, and in this regard, it is necessary to consider the current investor ESG landscape and the solutions in light of that landscape. Although the case study below focuses on some examples seen in the US, we would note that this dichotomy is not limited to the US investor universe, and we see similar situations arising in other geographies.

What Is the Investor ESG Landscape?

Several US states have adopted specific ESG positions. Approximately 20 states have adopted "anti-ESG" positions and approximately 15 states have adopted "pro-ESG" positions. These positions vary significantly by state and pose a range of practical issues for managers. Examples include:

On the "anti-ESG" side

- The prohibition of the investment of state money in companies/funds that boycott oil and gas

- Restricting investments of public funds to those based only on pecuniary factors (which is then defined as one that does not include the consideration of ESG and/or the promotion of social, political, or ideological interests)

On the "pro-ESG" side

- No investments of public funds in fossil fuels or firearms

- Statements explicitly allowing for the consideration of ESG factors in investing public funds

Whilst some investors get comfortable that they can effectively be disenfranchised from any "tainted" investments they would otherwise participate in — by tailored provisions that cater for excuse rights, redemption, divestment, or another exit route — we see other cases where investors push back if the fund itself can still invest in that asset.

What Are the Practical Solutions?

From our experience, side letter negotiations are one of the principal ways that investor polarisation is handled. The table below sets out some examples of what we've been seeing, based on recent experiences across our offices. In considering whether to address these items through a side letter, proper disclosure is critical in offering documents to notify prospective investors that these types of arrangement may be made through a side letter, and the potential impact it may have on the fund and the other investors.

|

Negotiation point |

What it means |

Comment |

|

Refinements to ESG elements of the manager's investment strategy |

Bespoke provisions given to a particular investor of how the investment strategy will be implemented, to accommodate that investor's preferences and perspective. |

A manager will be constrained by what they can commit to and represent, which is essentially to affirm the investment strategy they have articulated in their wider materials. |

|

Excuse rights |

Where an investor has an irreconcilable restraint, it can be treated as excused from any portfolio investment that derives a significant portion of its revenue from the "prohibited" investment — so, for example, were the fund to invest in, say, oil and gas or solar wind and energy — then a particular investor would not have to participate. |

That investor is treated as excused from any portfolio investment that derives a significant portion of its revenue from generation of a particular investment. This is often a preferred approach as it does not affect the SFDR disclosure obligations and is commercially viable where the excused investor(s) represent a relatively small proportion of the fund's equity commitments. |

|

Side pockets and redemption rights |

These effectively allow an investor to not be invested in a particular category of assets. |

Although the outcome is similar to that for excuse rights, introducing redemption rights in these circumstances can be commercially suboptimal from the manager's perspective. |

What Other Solutions and Issues Are There?

Other approaches to bespoke side letter provisions include the manager reconfiguring its marketing strategy. This would involve filtering the investor universe to include or exclude certain investors and by using parallel or sub-funds to accommodate pro-ESG investors and anti-ESG investors. For example, a European-focused Article 8 sleeve (that promotes environmental and/or social objectives) and a US-focused Article 6 sleeve (that does not). Another strategy change we have seen is a manager choosing to reduce ESG ambitions so that the fund in question classifies and discloses under Article 6 of the SFDR instead of Article 8 — although this may not be ideal as it limits capital from those who are more persuaded by an ESG agenda.

ESG reporting is also an area where some investors have significant additional requirements that affect a manager's compliance procedures and costs. On the cost side, we would typically expect this to be dealt with by way of either reimbursement as a fund cost or an incremental cost to the specific investor seeking bespoke reporting, so that the manager is not out of pocket.

Is the Future Brighter?

A key plank of the argument for "anti-ESG" investors is that by favoring ESG factors, managers are neglecting their fiduciary duties to maximise profits/returns. Of course, this could be rebutted by taking into consideration the data indicating that ESG factors can boost returns (for example, in the case of real estate assets, landlords taking into account ESG factors in the buildings they let are attracting more tenants than others who are not) to show that sustainable performance and positive impact are part of that value. On this basis, the argument is that the opposite is the case: ESG factors are included alongside (and as part of) other economic factors that form part of an investment decision.

In meeting their fiduciary duties, a manager has to assess all material risks and factors that they deem financially material to their business — credit, liquidity, and sustainability, in equal measure. This would allow a manager to argue that financial and ESG factors are one and the same.

The ability to advocate the "one and the same" argument outlined above will of course depend on the specifics in question and nature of an investor's requirements. As ESG reporting evolves, it may be more likely that a link can be forged to help reconcile "anti-ESG" positions with the Article 8 requirements.

Will the Data Show the Way?

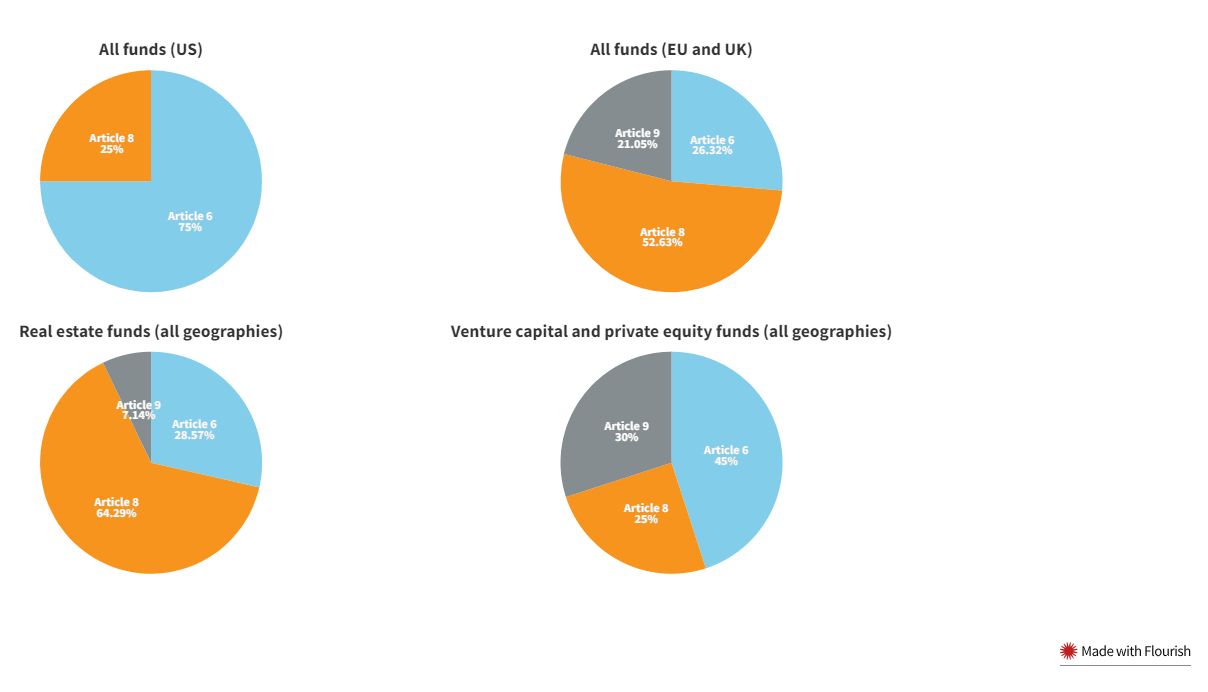

Analysis of Goodwin's Terms Database for Private Investment Funds indicates that funds disclosing under Article 6 of the SFDR are much more common for US fund managers (75%) compared to funds sponsored by UK and EU managers (26% Article 6, and the majority of 53% disclosing under Article 8). The percentages also vary by asset class and other factors. Based on data from 91 funds (across all geographies) that closed in the past 18 months, we have seen far fewer real estate strategies disclosing under Article 9 (7%) compared to private equity and venture capital funds (30%), and a significant majority (64%) of real estate funds disclosing under Article 8.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]