- with Inhouse Counsel

- in Asia

- in Asia

- in Asia

- with readers working within the Healthcare industries

The uptake of AI use cases in the financial services sector has been faster than regulators had initially envisaged. In financial services, AI is being used to: optimise internal processes; transform customer relationships; target marketing and offer services; assist in credit assessments; automate trading systems; detect patterns and make future value predictions; support know-your-customer (KYC) and due diligence processes; monitor risks, regulatory compliance and employees; shed light on dark data for underwriting and collection purposes; report data to regulators; and more. Some firms are also already investing in quantum computing projects, in anticipation of quantum viability.

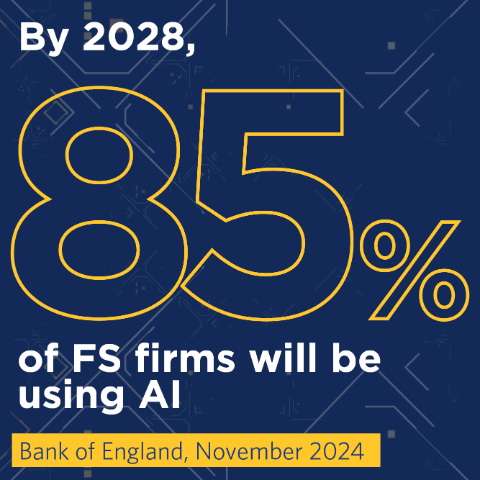

In November 2024, the Bank of England reported that more than 75% of financial services firms were using AI systems. Over 50% of all financial services AI use cases have some degree of automated decision-making: around 24% are semi-autonomous (designed to involve human oversight for critical or ambiguous decisions) and as of November 2024, only 2% were fully autonomous.

Research from Russell Reynolds suggested that in the first half of 2025 around 91% had taken steps towards implementing generative AI in their workflow.

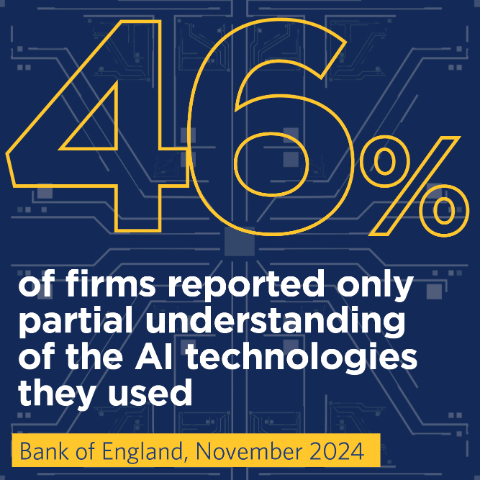

Against this background of increasing take-up, a third of financial services use cases are third-party implementations – this poses challenges in terms of transparency, governance and control, in addition to a degree of concentration risk at the level of cloud, model and data providers. More concerningly, only 34% of firms using AI felt they had a complete understanding of the technologies they used; 46% reported only partial understanding. Nonetheless, 40% of firms are using AI to optimise their own internal processes.

Regulatory approaches

The regulators, often with strong encouragement from

governments, are taking steps to ensure firms are empowered to

embrace automation and capitalise on the many opportunities it

creates. The vision is that AI will help to enhance growth, market

integrity and consumer outcomes.1 Most regulators seek

to foster the development of these systems through the provision of

testing environments for AI that simulate conditions close to the

real world, as well as other forms of private/public collaboration.

Unsurprisingly, however, the regulators also expect firms to ensure

appropriate management of the risks that the use of this technology

may introduce or amplify.

Markets remain complex, nuanced and deeply human. The value of skilled, well-trained analysts – those who understand market behaviour, context and intent – is not diminished by technology. If anything, it's amplified.

Dominic Holland

FCA Director of Market Oversight, November 2025

While a few jurisdictions have sought to adopt technology-specific legislation and rules, many jurisdictions and regulators (for example, the UK and Hong Kong) aim to take a technology neutral or agnostic stance, welcoming the use of 'good technology' to support and enhance decision-making but only as long as firms maintain robust governance, oversight and testing and comply with existing regulatory requirements. The result is that existing regulatory requirements – many of which were originally developed in a more analogue context – now apply in an increasingly digitalised operating environment. That said, regulators are also beginning to develop guidance and best practices on the basis of their growing experience of the range of AI use cases being deployed by the firms they regulate.

Nonetheless, as Dominic Holland, Director of Market Oversight at the UK Financial Conduct Authority (FCA), recently said, AI cannot replace human judgement. Interestingly, he noted that regulations are written with individuals in mind and stressed that the regulators' experience is in interrogating, issuing directions to, and taking action against individuals, including individuals within a body corporate.

Some regulators, like the Hong Kong Monetary Authority (HKMA), require firms to allow customers to opt out or request human intervention in customer facing applications using GenAI, and the Hong Kong Securities and Futures Commission (SFC) imposes stricter requirements on high-risk activities like the provision of investment recommendations, investment advice and investment research using GenAI models.

The Republic of Korea and Vietnam are progressing detailed and comprehensive requirements specifically governing the use of AI rather than focusing on financial services specifically; Indonesia, Thailand and the Philippines are also considering a comprehensive legislative approach, and the UK too is contemplating possible cross-sector legislation. The Australian government has, for now at least, rejected a proposal for stand-alone legislation.

On the other hand, having finalised AI-specific legislation, the EU is now delaying implementation of requirements for 'high risk' applications until harmonised standards and support tools are in place and is considering targeted measures to simplify the EU AI Act to help foster growth and innovation. In common with approaches elsewhere, EU AI regulation stresses the need for appropriate human oversight measures in addition to adequate risk assessment and mitigation systems, quality of datasets, transparency, monitorability, security and robustness.

Fundamentally, AI will continue to be a focus for regulatory, supervisory and use case development through 2026 and beyond.

Footnote

1 The HKMA, for example, notes potential uses such as the identification of vulnerable customers, and those who may need more information or clarifications to better understand product features, risks, and terms and conditions, and the issuance of fraud alerts to customers engaging in transactions with potentially higher risks: See HKMA Circular on customer protection in respect of the use of Generative Artificial Intelligence, 19 August 2024 (HKMA GenAI Circular).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.