- within Corporate/Commercial Law topic(s)

- with Finance and Tax Executives

- in United States

- with readers working within the Retail & Leisure industries

On April 29, 2015, the Securities and Exchange Commission (SEC)

voted 3-2 to propose new rules requiring companies to disclose the

relationship between executive compensation "actually

paid" and the company's "financial performance."

The proposed rules implement Section 14(i) of the Securities

Exchange Act of 1934, as added by Section 953(a) of the Dodd-Frank

Wall Street Reform and Consumer Protection Act. These disclosures

would be required to be included in proxy or information statements

in which executive compensation disclosure is currently required

pursuant to Item 402 of Regulation S-K.

The pay-versus-performance rules are one of four governance and

executive compensation-related provisions applicable to public

companies under the Dodd-Frank Act that remain to be adopted by the

SEC. Three of the four (pay-versus-performance, hedging policy and

pay ratio) have now been proposed, leaving only the clawbacks

rulemaking to be proposed. While not as controversial as the pay

ratio rulemaking, pay-versus-performance nonetheless will bring

with it challenges for companies subject to the new disclosure

requirements, not to mention contribute to the ever-expanding

length of proxy statements.

The two key questions in the pay-versus-performance disclosure

mandate are what is compensation "actually paid" and what

is "performance." The SEC took the approach in the

proposal that compensation "actually paid" is the total

compensation that companies report in the summary compensation

table with adjustments for pension benefits and equity awards,

while "performance" must be measured by total shareholder

return (TSR). In addition to disclosing information about the

company's compensation and TSR, certain companies subject to

the new requirements also will be required to provide disclosure of

their peer companies' TSR.

Companies Subject to the New Disclosure

Requirements

The proposed rules would apply to all reporting companies except

for foreign private issuers (which are not generally subject to the

proxy rules), registered investment companies and emerging growth

companies (which were exempted from the statutory requirement by

Section 102(a)(2) of the JOBS Act). Smaller reporting companies

would be subject to the new requirements, but would receive certain

accommodations under the proposal.

Covered Executives

The proposed rules would require disclosure about the company's

named executive officers (NEOs) for each covered fiscal year.

Information for the principal executive officer (PEO) would be

presented separately, while an average would be provided for the

remaining NEOs. If multiple PEOs serve during a covered fiscal

year, the reported data would be an aggregation of those

individuals' compensation. Any other former executives who are

included in the summary compensation table as NEOs would be

included in the average reported for the remaining NEOs. In

discussing the proposal, the SEC noted its belief that requiring

average compensation for the non-PEO NEOs would make the

information more comparable year-to-year in light of the likely

variability in the composition and number of non-PEO NEOs over the

years for which disclosure is required.

Summary of New Disclosures

The proposed rules would add new paragraph (v) to Item 402 of

Regulation S-K, which would require the following tabular

disclosure for each of the company's last five completed fiscal

years (or three years in the case of smaller reporting companies)

in any proxy or information statement in which disclosure under

Item 402 is required:

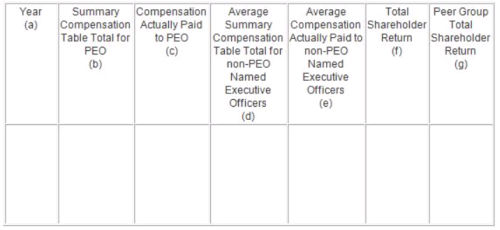

PAY VERSUS PERFORMANCE

As reflected above, the required table must disclose the following for each covered fiscal year:

-

the PEO's total compensation, as reported in the summary compensation table in the proxy statement (presented on an aggregate basis if there was more than one PEO during the year);

-

the compensation "actually paid" to the PEO (the summary compensation table total compensation as adjusted for pension benefits and equity awards) (presented on an aggregate basis if there was more than one PEO during the year);

-

the average total compensation for the non-PEO NEOs (including any former executive officers required to be included in the summary compensation table);

-

the average compensation "actually paid" to non-PEO NEOs (including any former executive officers required to be included in the summary compensation table);

-

the company's cumulative TSR, using the definition of TSR included in Item 201(e) of Regulation S-K, which sets forth an existing requirement for a stock performance graph; and

-

the TSR of the companies identified in the peer group identified by the company in its stock performance graph or in its compensation discussion and analysis (CD&A).

Companies also would be required (using

the information provided in the table) to provide 1) a clear

description of the relationship between executive compensation

actually paid to the company's PEO and other NEOs and the

cumulative TSR of the company for the period covered in the table

and 2) a comparison of the company's TSR and the TSR of the

company's peer group.

In addition to being allowed to present three rather than five

years of information, smaller reporting companies also would not be

required to provide disclosure about peer group TSR because they

are not required to disclose an Item 201(e) performance graph or

CD&A.

Companies would be required to tag the disclosure in eXtensible

Business Reporting Language, or XBRL, which represents the first

time information in proxy or information statements would be

required to be tagged. This requirement would be phased in for

smaller reporting companies, so that they would not be required to

comply with the tagging requirement until the third annual filing

in which the pay-versus-performance disclosure is provided.

Calculating Executive Compensation "Actually

Paid"

The SEC stated that it recognizes companies currently follow

different concepts for "realized" and

"realizable" pay and that companies have not broadly

accepted one conceptual approach over another. To provide

comparability across issuers, the SEC's proposed rule sets

forth a calculation for amounts "actually paid."

Executive compensation "actually paid" would be

calculated using the total compensation amount that companies

report in the summary compensation table already required in the

proxy statement as a starting point, with adjustments relating to

pension benefits and equity awards. Companies would be required to

disclose the adjustments to the compensation as reported in the

summary compensation table.

Under the proposal:

-

Pension amounts would be adjusted by deducting the change in pension value reflected in the summary compensation table and adding back the actuarially determined service cost for services rendered by the executive during the applicable year. Smaller reporting companies would not be required to make adjustments in pension amounts because they are subject to scaled compensation disclosure requirements that do not include disclosure of pension plans.

-

Equity awards would be considered actually paid on the date of vesting and at fair value on that date, rather than fair value on the grant date as required in the summary compensation table. A company would be required to disclose the vesting date valuation assumptions if they are materially different from those disclosed in its financial statements as of the grant date.

Measure of Financial Performance

While Section 14(i) of the Exchange Act

does not specify how a company's financial performance is to be

measured, it requires financial performance to take into account

any change in the value of the shares of stock and dividends of the

company and any distributions of the company. To meet this

statutory requirement, the SEC has proposed to use TSR, as defined

in Item 201(e) of Regulation S-K, which is calculated by dividing

(i) the sum of (A) the cumulative amount of dividends for the

measurement period, assuming dividend reinvestment, and (B) the

difference between the registrant's share price at the end and

the beginning of the measurement period; by (ii) the share price at

the beginning of the measurement period. Issuers, other than

smaller reporting companies, must present comparative TSR

information for the same peer group used for purposes of Item

201(e) of Regulation S-K, or, a peer group used in the CD&A for

purposes of disclosing the issuer's compensation benchmarking

practices. For many companies, TSR is not the way financial

performance is generally measured. While the proposal would require

use of TSR, companies may supplement the required disclosure under

the proposed rule with other measures that they feel are better

suited to the company, so long as such measures are clearly

identified, not misleading, and not presented with greater

prominence than the required disclosure.

Subject to Say-on-Pay Vote

Because the proposed new disclosures would be provided under Item

402, the disclosures would be subject to the say-on-pay advisory

vote required under Rule 14a-21(a). In proposing the new disclosure

requirements, the SEC noted its belief that both the

pay-versus-performance and pay ratio provisions under the

Dodd-Frank Act were intended to provide shareholders with

information to help assess a company's executive compensation

when exercising their rights to cast say-on-pay votes, and that the

new pay-versus-performance disclosures will provide shareholders a

new metric for assessing a company's executive compensation

relative to its financial performance.

Phase-In of New Disclosure Requirements

The proposed rules would be phased in for all companies subject to

the new disclosure requirements. Companies other than smaller

reporting companies would be required to provide information on the

prior three years the first time the new disclosure is provided,

with an additional year of information provided in each of the two

subsequent annual proxy or information statements. Smaller

reporting companies would initially provide the information for two

years, with the third year to be added in their next annual proxy

or information statement. The timing of adoption of the final rules

will determine when the disclosure is first required, which could

be as early as the 2016 proxy season.

Comment Period

Comments on the rule proposal should be received by the SEC on or

before July 6, 2015. The proposing release includes 54 specific

requests for comment, as well as a general request for comment. In

addition to requesting comment on the various specific details of

the rule proposal, the SEC more generally requests comment on

whether the proposed rule strikes the appropriate balance between

prescribing rules to meet the statutory requirements of Section

14(i) while also allowing issuers sufficient flexibility to provide

the most useful information to shareholders, and whether the SEC

should permit a principles-based approach to the disclosures.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.