- within Litigation and Mediation & Arbitration topic(s)

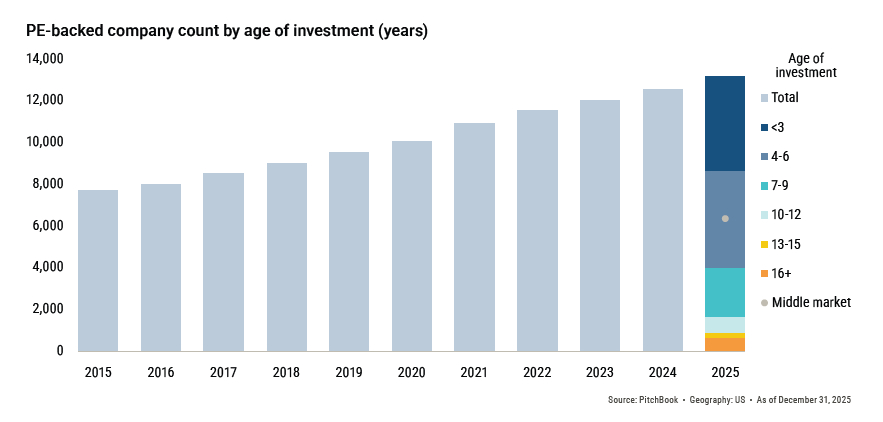

In the private equity sector, the middle-market exit environment is telling a pretty clear story right now. According to Pitchbook data:

- Half of sponsor-backed companies brought to market over the past few years didn't transact (largely driven by valuation disconnects).

- More than 6,000 PE-backed middle market companies remain unsold, with median hold periods stretching to 6.4 years.

- Corporate exits are down ~30% year-over-year, removing a key price-setting buyer from processes.

Not every deal is struggling, as it appears that deals involving high-quality assets are getting done. But in other cases, private equity sponsors are navigating heightened complexity because everything else is either getting repriced, restructured, or held longer than planned.

Factors that will drive success in middle-market private equity exits

In this environment, we're seeing increased focus on pre-sale readiness, clean and defensible revenue, data integrity, and operational clarity to bridge the gap between buyer expectations and seller value.

What's changed is the level of scrutiny. Buyers are underwriting to what they can validate, not what's in the CIM. That's putting pressure on PE teams to address areas that didn't always determine outcomes before, such as revenue quality, consistency of data across systems, and the ability to tie performance to a clear, repeatable operating model.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.