- with readers working within the Pharmaceuticals & BioTech industries

- within Insolvency/Bankruptcy/Re-Structuring, Consumer Protection and Law Department Performance topic(s)

Allocation of merger control execution risk in transaction documents is front of mind for merging parties. The stakes are high where regulatory outcomes are unknown or hard to predict. But the emergence of a more permissive merger control environment may prompt a change in both the balance and nature of deal protections.

Caution in the face of unpredictability

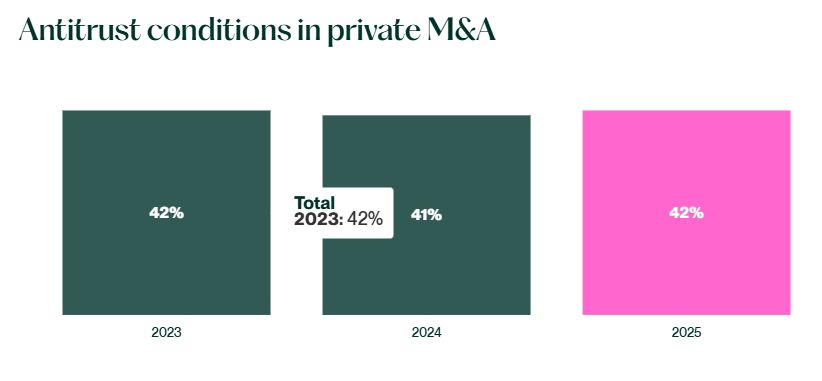

According to our research on global private M&A deals, the proportion of transactions that were subject to antitrust approvals conditions remained relatively steady last year, at 42%.

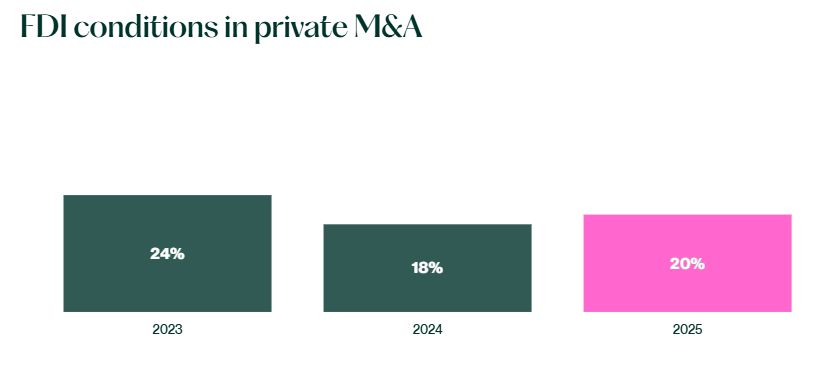

For deals conditional on FDI approvals, it was a similar picture. The figure increased slightly to 20% of our deals.

Unsurprisingly, the proportion rises for big-ticket deals. These are generally more likely to trigger regulatory filings (especially given the continued proliferation of merger control and FDI regimes). Of our transactions valued at USD1 billion or more, three quarters were subject to antitrust conditions and a third included FDI conditions.

Going forward, we could see merger control outcomes become more predictable as a more permissive approach to enforcement beds down in key jurisdictions (see Fewer roadblocks for M&A: Politics play into lighter touch merger control enforcement).

However, with the potential for regulatory reviews to be influenced by turbulent geopolitics and shifting domestic priorities, it is likely that merging parties will continue to approach antitrust and FDI risk allocation with caution.

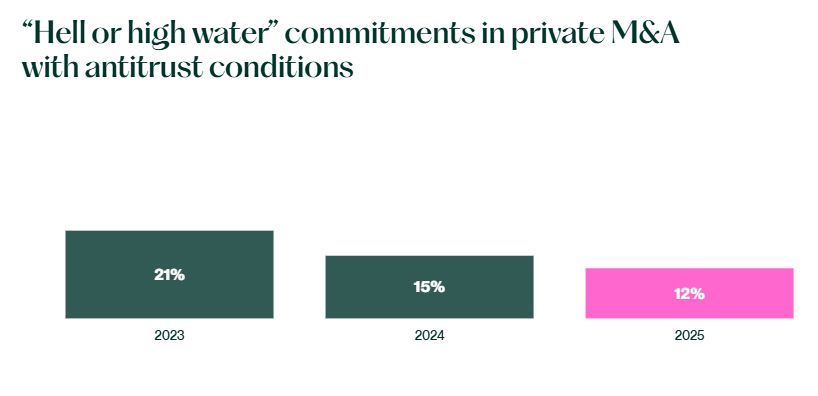

Hell or high water commitments dwindle

"Hell or high water" (HOHW) commitments compel the buyer to do everything in its power to secure merger control clearance (e.g., by accepting remedies in any form).

Instances of HOHW commitments continued to decline in 2025, down to 12% of our deals containing an antitrust condition.

With the nature of merger remedies often being difficult to predict, particularly where they might comprise behavioral commitments, buyers are likely to push back on HOHW commitments that could force them to make unforeseen and far-reaching concessions. They will be even more resistant to HOHW clauses where a full divestment fire sale might be required.

Instead, we could see antitrust conditions with a more limited obligation, e.g., requiring the buyer to only accept remedies subject to a material effect qualifier, or provided that no divestment of its existing group or portfolio is required. These were included in 16% of our deals with an antitrust condition last year. This figure may rise in next year's report.

For transactions conditional on FDI approvals, HOHW commitments only appeared in 12%, down from 17% in 2024. This reflects the unpredictability of FDI review outcomes, where deals may be blocked or remedies imposed without discussion with the buyer.

Reverse break fees in favor (for now)

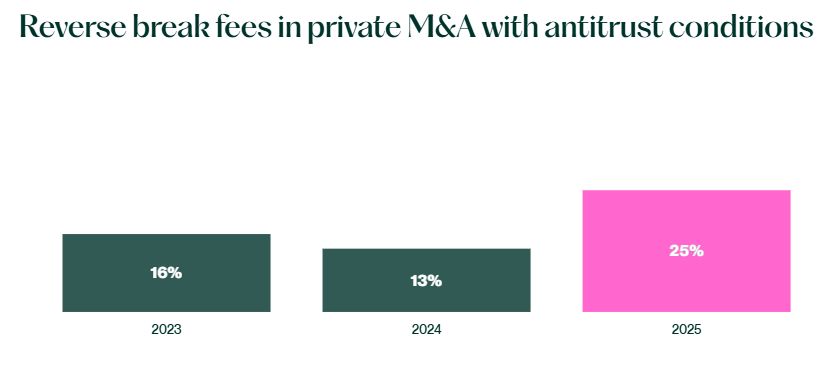

As HOHW commitments decreased, instances of reverse break fees shot up.

In 2025, they appeared in a quarter of our deals that were conditional on antitrust approval, nearly double the 2024 tally. It was a similar story in our deals with FDI conditions.

The average fee was 8% of enterprise value (6% for FDI). This is relatively high but is broadly in line with the wider market last year.

The reverse break fee agreed on Prosus' acquisition of Just Eat was 8 to 10% (the deal is now closed after the European Commission issued a conditional clearance). Google reportedly agreed to a similarly high fee in relation to its planned purchase of cloud security platform, Wiz.

Whether this trend continues is something to watch over the coming months.

As merger control enforcement becomes less aggressive, a shift in the use of reverse break fees may become apparent. Conversely, as FDI review outcomes remain politicized, reverse break fees may continue to provide a useful deal protection compromise.

Key takeaways

Early assessment of regulatory risk is crucial

At the outset, analyze the likelihood of antitrust, FDI, or FSR intervention. Be aware of authorities' current enforcement priorities and the possibility for political or geopolitical influences. This assessment will frame negotiations on risk mitigation and allocation and will feed into the overall regulatory strategy.

Consider provision for below-threshold reviews

Authorities are increasingly obtaining and using powers to scrutinize transactions that do not meet filing thresholds (see Driving uncertainty: Below threshold M&A is not safe from merger control review). This possibility is greater in some jurisdictions, and for deals in certain sectors, such as digital, life sciences, or other strategic industries. Where there is call-in risk, ensure any conditions and other deal terms cover this eventuality.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.