- within Criminal Law and Intellectual Property topic(s)

In private equity (PE), firms often follow a highly

leveraged business model, and cash is more than a by-product of

operations; it is a

strategic asset. Unlocked cash can be used for reducing

debt, returning capital to shareholders, and reinvesting in the

business

for growth, yet despite its pivotal role in value creation,

working capital—a source of potential short-term free cash

flow—usually remains only an afterthought.

Sponsors tend to prioritize revenue growth and margin expansion while ignoring cash trapped in day-to-day operations.

SUCH DISREGARD IS COSTLY.

Working capital represents one of the most immediate and most accessible sources of liquidity in a portfolio company. At PE firms focused on maximizing returns, working capital optimization should therefore not be only a secondary concern. Working capital optimization is a critical lever for value creation—and is especially relevant in today's environment of global trade disruption and slowing economic growth, both of which have served to add pressure on portfolio company finances—on top of current higher interest rates.

PE firms are more versed than most in working capital, but we still regularly see missed opportunities and gaps in execution.

This series of articles shows why PE firms and theirportfolio companies should make working capital management a priority and offers ways to improve that management both quickly and sustainably. By learning the strategic value of working capital, deploying technology, using artificial intelligence, applying data-driven decision-making, and implementing best-in-class operational practices, sponsors can unlock substantial trapped capital, accelerate liquidity, and increase returns. Working capital directly influences both internal rate of return (IRR) and fund performance. And every dollar of free cash flow can have a direct—and positive—impact on investment returns, financial performance, value creation, and exit readiness.

This series of articles shows why PE firms and their portfolio companies should make working capital management a priority and offers ways to improve that management both quickly and sustainably.

ROLE OF WORKING CAPITAL IN PRIVATE EQUITY VALUE CREATION

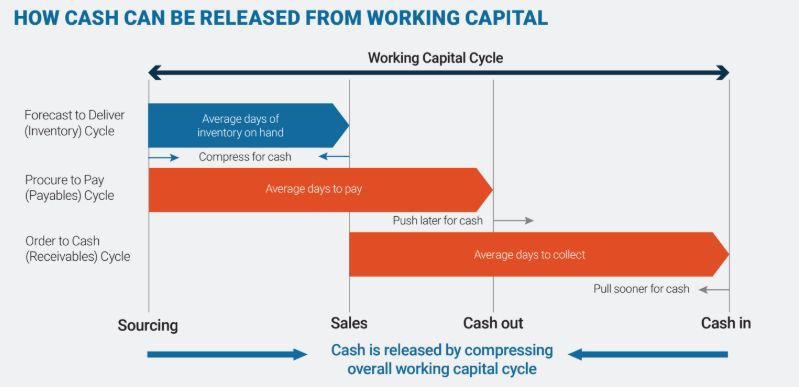

Every company needs working capital because working capital is the fuel that powers daily operations: It gives credit to customers, stores up the inventory necessary for operations, and pays suppliers on time.

Working capital is the cash tied up in daily operations. Technically speaking, working capital is defined as current assets (such as receivables and inventory) minus current liabilities (such as payables). In practical terms, it is cash that should be moving through the business but that often sits idle due to inefficiencies in collections, payments, operations, and inventory management. Like any fuelworking capital should be used as efficiently as possible and in the same way because it is better—other things being equal—to drive a fuel-efficient car than a gas guzzler.

Despite its impact on liquidity and returns, however, working capital typically receives less attention from sponsors and portfolio companies than revenue growth, EBITDA expansion, and capital expenditures. And because it moves continuously through the balance sheet, working capital often gets mismanaged or even overlooked.

Cash might be hiding in hard-to-see places, such as work that has been completed but not yet billed or slow-moving and obsolete inventory in the warehouse. Left unoptimized, excess working capital erodes returns, delays shareholder distributions, and weakens financial flexibility.

Reframing working capital as a recoverable asset rather than a fixed constraint changes the equation positively. Every inefficiency in receivables, payables, or inventory represents an opportunity to unlock liquidity. By tightening customer terms, improving collections, adhering to a tight billing schedule, reducing excess inventory, eliminating rework and waste, and optimizing supplier payment strategies, businesses can get cash—without additional financing. And the funds can be reallocated to invest in portfolio company growth initiatives and acquisitions, to return capital to investors, or to reduce costly debt.

WHY CASH MATTERS MORE THAN EVER IN PRIVATE EQUITY

Unlocking working capital accelerates cash generation and allows

for early distributions to investors and enhancements of IRRs. Even

a partial distribution ahead of schedule provides funds with the

flexibility to redeploy capital into new opportunities, compounding

returns

over time. During the sale of a portfolio company, working capital

often gets heavily discounted. Sellers and buyers routinely rely on

working capital historical trends and benchmarks, meaning that

working capital generally does not get fully reflected in the

purchase price. In effect, unoptimized working capital represents

value left on the table. But sophisticated sponsors know that every

dollar

of working capital removed from the business ahead of a transaction

profits the seller.

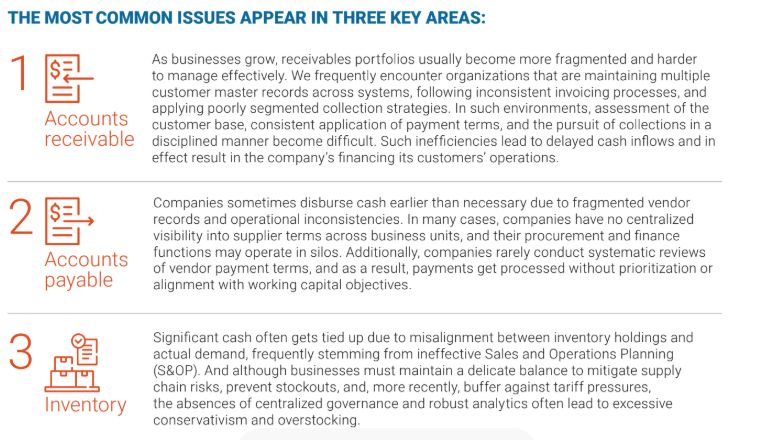

For buyers, part of the challenge lies in underwriting. Although buyers typically assess high-level metrics—such as days sales outstanding, days payable outstanding, and days inventory outstanding—those aggregated indicators often mask underlying opportunities. However, when data rooms include detailed transactional and operational data, the identification of actionable opportunities even during due diligence becomes possible. For example, analysis of invoice-level payment histories, stock-keeping-unit (SKU) level inventory turnover, and invoice-level receivables aging analysis can reveal structural cash traps and support a credible post-close value creation thesis.

Beyond improving exit economics, disciplined working capital

management creates opportunities for reinvestment throughout the

holding period. For instance, in a high-interest-rate environment,

in which raising additional capital is more expensive, self-funding

growth through released working capital is a compelling strategy

because there is no cheaper capital than the money you

already

have. Freed-up cash can be deployed toward expansion, digital

transformation, new product development, or bolt- on

acquisitions—all without increasing leverage.

Even in well-managed organizations, operational complexity often outpaces control—especially in fast-growing or global businesses. Complexity can cause blind spots where cash becomes trapped.

THE BOTTOM LINE

Optimizing working capital from Day One generates cash—and cash creates options.

For instance, cash enables sponsors and portfolio company

leaders to determine whether to reinvest in expansion or return

capital

to stakeholders. And the earlier that working capital optimization

begins, the greater the benefits will be, yet too many firms fail

to extract trapped cash, leaving value on the table.

Working capital should not be only an afterthought.

Sponsors that identify, unlock, and deploy trapped cash early can position their portfolio companies for stronger returns, higher valuations, and greater resilience in uncertain markets.

The impact of that freed-up liquidity is immediate, but its strategic value extends further—whether through early distributions to investors, self-funded growth initiatives, or a fortified financial position that enhances flexibility.

Moreover, embedding disciplined working capital practices into

the business increases process efficiencies so that by the time of

sale,

the business benefits from a leaner balance sheet, more-efficient

operations, and well-documented financial discipline—all of

which make the business more attractive to buyers and support a

stronger valuation.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]