In December 2017, the CBOE Futures Exchange (CFE) and the Chicago Mercantile Exchange (CME) introduced bitcoin futures contracts. The opportunity to trade bitcoin futures on two established exchanges was viewed as increasing bitcoin's credibility and has facilitated additional venues for trading in the cryptocurrency, sometimes referred to more generally as virtual currencies or digital assets. Futures trading allowed investors to take leveraged economic positions in bitcoin which previously traded only on a decentralized and unregulated spot market. This article reviews some of the key features of the bitcoin futures contracts and provides an overview of trading activity during the first year of their existence.

I. Bitcoin

Bitcoin, considered a commodity by the U.S. Commodity Futures Trading Commission (CFTC),1 is a decentralized virtual currency, also referred to as a cryptocurency, based on blockchain technology.2 Bitcoin, launched in 2009, surged in popularity during 2017, when its market capitalization increased from approximately $15 billion at the beginning of the year to $326 billion at its peak in December 2017.

Absent any market distortions, the price of bitcoin is determined by supply and demand.3 Supply is affected by "new" bitcoins that are created through a transaction verification process, also known as mining,4 and the sale of bitcoins already in circulation. Demand is affected by factors including expectations about bitcoin's potential, which is uncertain, and the pool of buyers. Bitcoin's potential is tied to prospects about its wider acceptance, such as its use as a means of payment or storage of value, as well as expectations about relevant legal and regulatory developments. The possibility of a competing cryptocurrency that may overtake bitcoin in popularity also affects demand. Bitcoin's price thus remains volatile, similar to the prices of other cryptocurrencies.

Bitcoin trades on many spot markets which are markets generally accessible to the public. In these markets, digital assets like bitcoin and other cryptocurrencies are traded for almost immediate delivery. CoinMarketCap.com, a widely-referenced site for prices of various cryptocurrency assets, contains a list of spot exchanges including information on trading volume and exchange rates for cryptocurrency pairs. Although transaction fees vary by exchange, they are usually set as a percentage of the value of the transaction. Participants who open an account with an exchange may fund their account either with conventional (fiat) currency or other cryptocurrencies, and upon verification, are allowed to start trading on that exchange. As with other markets, one key consideration is liquidity.5 All else being equal, participants tend to select exchanges with higher liquidity and lower fees.

II. Bitcoin Futures: CFE and CME Contracts

A futures contract is a standardized exchange-traded derivative contract to buy or sell real or financial assets at a set price, on a specified future date, in a predefined quality and quantity. Futures contracts can complement the trading of assets in the spot markets and provide certain benefits like leverage (which magnifies returns),6 enhanced liquidity, improved diversification, and a means of selling an asset "short" (i.e., selling an asset that is not owned by the seller). Selling short allows market participants who believe that the price of an asset is too high to bet against it, putting downward pressure on the price.

CFE launched trading in bitcoin futures contracts on December 10, 2017 under the ticker XBT. CME followed soon after on December 18, 2017 by offering its own bitcoin futures contracts under the ticker BTC. Both exchanges have offered contracts with several expiration dates, generally shorter than six months. One of the characteristics of bitcoin futures contracts is that they are cash-settled and therefore do not involve the exchange of actual bitcoin. Anyone who has an account with a registered futures broker can therefore gain an economic exposure to bitcoin.

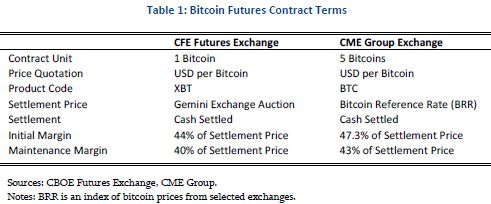

The exchange determines the contract details such as size, trading limits, settlement conventions, and margin requirements. Table 1 summarizes some of the main features of the bitcoin futures contracts traded on CFE and CME.7 Aside from the contract unit size and determination of the settlement price, the contracts on both exchanges are similar in many ways, including sizeable initial and maintenance margin requirements (implying an approximate two-plus times leverage).8

The margins are set substantially higher than most other exchange-traded futures contracts, likely due to high bitcoin volatility. Higher margins make bitcoin futures more expensive to trade than other futures because they provide less leverage. Maintenance margins of other futures are generally lower at typically 3-12 percent of the notional value of the contract (implying an approximate ten to thirty-plus times leverage).9

As depicted in Figure 1 below, the CME has captured a gradually increasing share of trading in futures contracts, from 17 percent in December 2017 to 56 percent in December 2018.10 The volume of traded contracts, depicted in the bottom chart of Figure 1, varied substantially over time with a maximum volume of more than 85 thousand contracts during the week of July 23, 2018 and an average volume of approximately 41 thousand contracts.11

The figure shows the number of futures contracts traded on the two exchanges. As shown in Table 1, CFE has a "smaller" size futures contract unit that references one bitcoin, whereas CME has a "larger" size futures contract unit that references five bitcoins. Figure 1 may indicate a gradual increasing preference among investors for large size of bitcoin futures contracts during the last year.

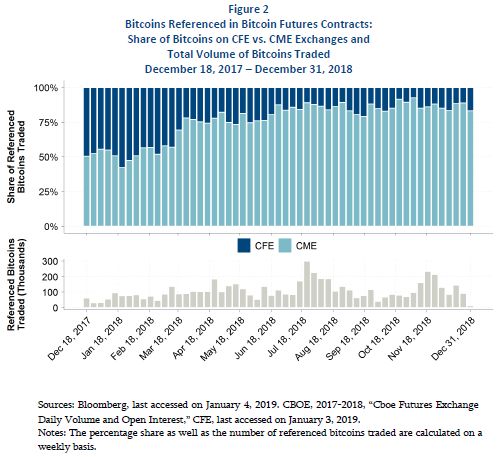

Figure 2 below depicts the share of bitcoins referenced by traded futures contracts on CFE and CME, adjusting for differences in contract unit size. The share traded on CME started at 51 percent in December 2017 and increased to 87 percent in December 2018.12 The weekly volume of bitcoins referenced in futures contracts, depicted in the bottom chart of Figure 2, also varied substantially over time. The average weekly volume was approximately for 110 thousand bitcoins and weekly volume peaked at 298 thousand bitcoins during the week of July 23, 2018.13 The average weekly volume over the period corresponded to approximately $797 million in dollar terms (number of referenced bitcoins times dollar value per bitcoin), with substantial variance in the value, partially due to bitcoin price fluctuations during 2018.14

The two exchanges also differ in the determination of the bitcoin reference price they use for settlement purposes. CFE's bitcoin reference price for final settlement is sourced from a single bitcoin spot exchange Gemini.15 CME's bitcoin reference price for final settlement relies on the "Bitcoin Reference Rate" (BRR), which is an index constructed from relevant transactions of multiple constituent spot exchanges.16 Although the two reference prices are determined at different times of day (CFE Gemini's auction is at 4 p.m. Eastern time whereas CME BRR is based on trading between 3 p.m. and 4 p.m. London time), historically the two prices have been closely correlated, with a daily correlation of 99.8 percent over the period between February 9, 2018 and December 31, 2018. Given the similarities in contract attributes between the CFE and CME bitcoin futures, the contract size (5 bitcoins on CME vs. 1 bitcoin on CFE) may be one of the key factors that contributes to the relatively larger volumes observed on CME.

III. Bitcoin Spot vs. Futures Activity

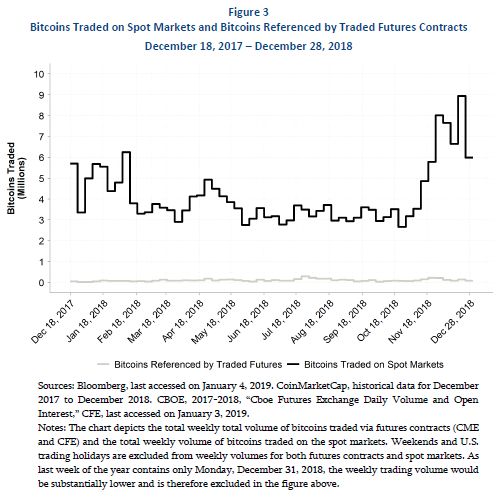

Even though trading activity in bitcoin futures has been increasing, its share is small relative to spot markets.17 Figure 3 depicts the number of bitcoins traded on the spot markets, as aggregated by CoinMarketCap.com, as well as the number of bitcoins traded in all exchange-traded futures contracts.

The volume of bitcoins traded on the spot markets is substantially greater than the volume of bitcoins traded in the bitcoin futures contracts. As shown in Figure 4, bitcoins referenced by traded futures as a share of bitcoins traded on spot markets has been volatile throughout 2018. The share increased in the first half of the year, peaking in late July 2018, and subsequently declined to a level comparable to the share in December 2017.18

The share of bitcoins traded through the futures markets as a percentage of bitcoins traded on spot markets may further increase if the U.S. Securities and Exchange Commission (SEC) allows the listing of bitcoin exchange-traded funds (ETFs). Bitcoin ETFs, if approved, would likely include bitcoin futures in their holdings.19 The SEC has so far either disapproved or delayed its decision on any proposed bitcoin ETFs,20 but is expected to decide on the SolidX bitcoin ETF, which proposes holding actual bitcoin instead of bitcoin futures, later this year.

IV. Regulation

The CFTC regulates derivative exchange operators, which include CFE and CME, and as a consequence bitcoin futures contracts traded on the two exchanges are under the purview of the CFTC.21 The two exchanges completed a relatively quick and hands-off CFTC self-certification process prior to launching their respective bitcoin futures contracts.22

Separately, cryptocurrencies, like bitcoin, trade in the U.S. under the purview of multiple other agencies. For example, state banking regulators oversee cryptocurrency spot exchanges through state money transfer laws. The U.S. Department of the Treasury's Financial Crimes Enforcement Network (FinCEN) monitors bitcoin and other cryptocurrency transfers for anti-money laundering purposes. In addition, the U.S. Internal Revenue Service (IRS) considers virtual currencies as property and, as a result, profitable bitcoin trades are subject to capital gains taxes.23 Finally, the SEC has been closely monitoring the emerging initial coin offerings (ICOs) which are primarily funded by cryptocurrencies including bitcoin.24

The CFTC has perhaps been one of the first regulators in issuing active guidance to investors regarding cryptocurrencies such as bitcoin. The CFTC initially declared bitcoin a commodity in 2014.25 A few years later, in October 2017, the CFTC published a primer discussing several types of risks related to bitcoin and other cryptocurrencies26 and warned that periods of high volatility with inadequate trading volume might create adverse market conditions, leading to harmful effects such as customer orders being filled at undesirable prices.27

V. Conclusion

This article summarizes the key features of bitcoin futures contracts traded on CFE and CME and presents information on trading activity on both exchanges over the initial year of their existence. Each of the two exchanges captured approximately half of the bitcoin futures contracts traded leading into December 2018 – a year after their original launch – with an increasing trend of CME's relative share during the year. CME's trading share of referenced bitcoins may be driven by the larger contract size. Relative volume of bitcoin futures as a percentage of the bitcoin spot markets was volatile, peaking in late July 2018, when bitcoin spot trading volume was relatively flat.

Relative volume decreased in the last few months of 2018, when bitcoin spot trading almost tripled, returning to the initial levels seen around the launch period in December 2017. CME and CFE bitcoin futures markets are young and the regulatory landscape surrounding bitcoin is still developing. These markets may thus inform and develop precedents for other cryptocurrency derivative markets and are worth following.

Footnotes

1. In addition, on March 6, 2018, Judge Jack B. Weinstein of the U.S. District Court for the Eastern District of New York ruled that virtual currencies are commodities under the Commodity Exchange Act and therefore subject to the CFTC's anti-fraud and anti-manipulation enforcement authority. Commodity Futures Trading Commission v. McDonnell, No. 1:18-cv-00361-JBW-RLM.

2. Blockchain is a distributed digital ledger which is composed of blocks of ledger entries created and "chained" together by cryptography to provide a complete and verifiable transactional history without the necessity to rely on a trusted "third" party.

3. For discussion of supply and demand considerations of bitcoin price formation, see Ciaian, Pavel, Miroslava Rajcaniova, and d'Artis Kancs (2016) "The economics of BitCoin price formation," Applied Economics, 48:19, p. 1799-1815, DOI: 10.1080/00036846.2015.1109038.

4. The bitcoin transaction verification process is based on a predetermined algorithm, with its ultimate stock of bitcoin limited to 21 million units.

5. Liquidity captures the degree to which an asset or a financial instrument can be quickly bought or sold in the market without affecting its price.

6. See p. 10 of CME Group's Trader's Guide to Futures: "Leverage on futures contracts is created through the use of performance bonds, often referred to as margin. This is an amount of money deposited by both the buyer and seller of a futures contract [...] to ensure their performance of the contract terms. The performance bond may represent only a fraction of the total value of the contract, often 3 to 12%, making futures a highly leveraged trading vehicle. Therefore, futures contracts represent a larger contract value that can be controlled with a relatively small amount of capital. This provides the trader with greater flexibility and capital efficiency." Accessed on February 6, 2019, https://www.cmegroup.com/education/files/a-traders-guide-to-futures.pdf.

7. Additional details on the CME contract design can be found in Moran, Nicole, Yesim Richardson, and Robert Letson, "Bitcoin Futures: A Closer Look At CME's Contract Design," Law360, December 19, 2017.

8. Initial margin is a collateral that needs to be deposited with the exchange prior to opening a position, whereas maintenance margin is a collateral that needs to be maintained with the exchange to keep the position open. The maintenance margin is generally lower than the initial margin. On CME, the initial margin requirement for all speculative products is set at 110 percent of the maintenance margin requirement (see web site: https://www.cmegroup.com/clearing/risk-management/performance-bonds-margins.html, accessed on December 20, 2018.) The purpose of the margin requirements is to reduce counterparty risk. Bitcoins' maintenance margin corresponds to 43 percent of contract's value (see https://www.cmegroup.com/education/bitcoin/cme-bitcoin-futures-frequently-asked-questions.html, accessed on December 20, 2018).

9. See CME Group discussion of the margins: "Futures margin generally represents a smaller percentage of the notional value of the contract, typically 3-12% per futures contract [...]." Accessed on December 20, 2018, https://www.cmegroup.com/education/courses/introduction-to-futures/margin-know-what-is-needed.html.

10. Considering only days after December 18, 2017, when CFE as well as CME traded the bitcoin futures. The percentages for the month are calculated based on monthly volumes when the trading of bitcoin futures was possible on both exchanges.

11. The average volume calculation considers data starting on December 18, 2017 and excludes the last week of the year 2018, which contains only Monday, December 31, 2018.

12. Same as endnote 10.

13. Same as endnote 11.

14. The weekly trading volume in dollars is an aggregation of the daily volumes of each of the contracts multiplied by the corresponding daily close price.

15. CFE does not use Gemini Continuous Trading to determine the daily settlement bitcoin futures price, as such price could possibly be easier to manipulate, but instead relies on Gemini Auction at 4 p.m. Eastern time for BTC-USD pair on the final settlement date. Because the auction focuses market participants into a particular moment, such auctions generally result in better price discovery.

16. CME uses the BRR index which is determined between 3 p.m. and 4 p.m. London time. The potential for manipulation of the reference rates is discussed in Wagener Brown-Hruska, Sharon, Jordan Milev, and Trevor Wagener, "Crypto Market Surveillance Has Arrived," Law360, May 25, 2018.

17. As discussed above, bitcoin futures are cash-settled and therefore do not involve the exchange of actual bitcoin. Trading on the bitcoin spot markets, however, has some potential benefits that may not be captured by the bitcoin futures market. For instance, futures contracts may not enjoy the benefits of any potential bitcoin "fork." A fork is a type of split among bitcoin network nodes, where some of the nodes may adopt an updated protocol for processing bitcoin transactions and the remaining nodes stay within the existing protocol. The result of a fork is a bifurcation of the original blockchain and associated bitcoins. Because any bifurcation starts with the original blockchain ledger, every investor that is indicated on the ledger as holding bitcoins at the time when the cryptocurrency undergoes the "forking" process keeps those units and also becomes an owner of equivalent units of the new currency that arose as a result of the fork. For example, the bitcoin blockchain experienced such a "fork" on August 1, 2017, where a separate version of bitcoin was created under the new label "bitcoin cash" (BCH). The BCH ledger went on to record transactions separate from those of the original bitcoin ledger. Because the BCH ledger started with the original bitcoin ledger, investors who owned bitcoins on the "fork date" appeared on the new BCH ledger as owners of the same amount of the new currency. To the extent that such new cryptocurrency has a positive value, the "fork" may generate benefit to a bitcoin holder, but not to an individual holding bitcoin futures. Such individual does not hold actual bitcoins and their interest is therefore not part of the bitcoin ledger.

18. Note the potential tax benefits of trading futures, which are taxed using the 60/40 rule, where 60 percent of gains are taxed at the long-term rate and 40 percent of gains are taxed at the short-term rate. Gains from spot trades of assets held less than a year are taxed at a higher short-term rate. Thus, trading futures may provide tax benefits compared to trading on the spot market. For details, see Section 1256 of Title 26 of the U.S. Code.

19. For example, see the proposal of ProShares Trust which outlines investment strategy as follows: "The Fund generally seeks to have 30% of the value of its portfolio invested in bitcoin futures contracts and 70% of the value of its portfolio invested in money market instruments. The Fund does not invest directly in bitcoin." Accessed on October 2, 2018, https://www.sec.gov/Archives/edgar/data/1174610/000119312517373736/d506454d485apos.htm.

20. For review of recent developments in Bitcoin ETFs, see Asjylyn Loder, "Bitcoin ETFs Keep Trying, Despite Regulators' Rejections," Wall Street Journal, September 23, 2018, accessed on October 2, 2018, https://www.wsj.com/articles/bitcoin-etfs-keep-trying-despite-regulators-rejections-1537754701.

21. CFTC's mission is to foster open, transparent, and competitive markets and protect market users and their funds from fraud, manipulation, and abusive practices related to the Commodity Exchange Act (CEA).

22. In 2017, CFE and CME self-certified the new bitcoin futures contracts with the CFTC. Self-certification is one of the paths for an exchange to attest that a new product complies with the CEA and CFTC regulations, including that the new contract is not readily susceptible to manipulation. The CFTC self-certification process provides a quicker path to allow trading of new derivative contracts, allowing exchanges to self-certify new products on twenty-four hour notice prior to trading with the goal to foster innovation in financial markets. See CFTC Backgrounder on Self-Certified Contracts for Bitcoin Products, accessed on August 6, 2018, https://www.cftc.gov/sites/default/files/idc/groups/public/@customerprotection/documents/file/backgrounder_virtualcurrency01.pdf. For discussion of the trade-offs of CFTC's self-certification process, see Rubin, Gabriel T., "Rise of Bitcoin Futures Prompts Regulator to Revisit Hands-Off Approach," Wall Street Journal, January 31, 2018, accessed on January 23, 2019, https://www.wsj.com/articles/rise-of-bitcoin-futures-prompts-regulator-to-revisit-hands-off-approach-1517394600.

23. See IRS's Notice 2014-21, accessed on September 9, 2018, https://www.irs.gov/pub/irs-drop/n-14-21.pdf.

24. See CFTC Backgrounder on Self-Certified Contracts for Bitcoin Products, accessed on August 6, 2018, https://www.cftc.gov/sites/default/files/idc/groups/public/@customerprotection/documents/file/backgrounder_virtualcurrency01.pdf.

25. Testimony of Chairman Timothy Massad before the U.S. Senate Committee, December 10, 2014, accessed on October 2, 2018, https://www.cftc.gov/PressRoom/SpeechesTestimony/opamassad-6.

26. Even though some of the risks, such as losing one's private keys from the bitcoins, can be avoided by trading bitcoin futures, systemic security issues affecting the underlying asset remain.

27. LabCFTC, "A CFTC Primer on Virtual Currencies," accessed on August 2, 2018, https://www.cftc.gov/sites/default/files/idc/groups/public/documents/file/labcftc_primercurrencies100417.pdf.

The authors would like to thank Eli Offenkrantz, Kevin Pan, and Raghav Saraogi for their assistance with this article.

The opinions expressed are those of the author(s) and do not necessarily reflect the views of the The Brattle Group, its clients, or any of its or their respective affiliates. This article is for general information purposes and is not intended to be and should not be taken as legal advice.